An investment outside India can be done by an Indian party or an individual or (single or in association with another resident individual or with an ‘Indian Party’). All resident individuals, including minors, are allowed to freely remit up to USD 250,000 per financial year.

An Indian Party can make overseas direct investment in any bonafide activity. However, Real estate and banking business are the prohibited sectors for overseas direct investment. But, Indian banks operating in India can set up JVs/WOSs abroad provided they obtain clearance under the Banking Regulation Act, 1949, from the Department of Banking Regulation (DBR) and RBI.

Note: *When more than one such company, body or entity makes investment in the foreign JV/WOS, such combination will also form an “Indian Party”.

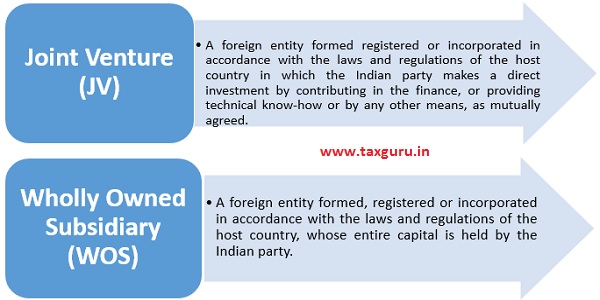

Forms of Entity that An Indian party can form for Overseas Direct Investment :-

Modes of Direct Investment :-

Modes of Direct Investment :-

♦ In both the cases, an Indian Party should approach an Authorized Dealer Category – I Bank (hereafter, referred as “AD bank”) with an application in Form ODI Part-I along with the prescribed enclosures / documents.

♦ The AD bank should report the relevant Form ODI in the online OID application and obtain UIN while executing the remittance and intimate to the Remitter which shall be used by him in all the future communication made with RBI.

| Automatic Route | Approval Route |

|

No prior approval from the RBI required if an Indian Party make ODI in equity shares and compulsorily convertible preference shares subject to certain conditions and restrictions explained as follows: 1. The WOS should be engaged in bonafide business activity. 2. The total financial commitment of the Indian Party in all WOS should not exceed 400 % of the net worth of the Indian Party as on the date of last audited balance sheet. However, any financial commitment exceeding USD $ 1 billion in a financial year would require prior approval of the Reserve Bank. 3. The Indian party should not be on the Reserve Bank of India’s Exporters’ caution list / list of defaulters. 4. An Indian Party may extend a loan or a guarantee to or on behalf of the JV/WOS abroad only if there is already existing equity participation by way of direct investment in such overseas entity. If there is no equity holding of Indian Party, then Loan and Guarantee can be granted by way of RBI Approval. 5. The valuation of shares of the company outside India shall be made by a Chartered Accountant or a Certified Public Accountant. However, if the amount is more than USD 5 million, the valuation of the shares shall be made by a Category I Merchant Banker registered in/outside India. 6. The Indian Party routes all the transactions relating to the investment in a JV/WOS through only one branch of an Authorised Dealer(AD) to be designated by the Indian Party.

|

If the conditions not fulfilled under Automatic Route then the Indian Party shall seek prior approval of the RBI before making investment. RBI before approval shall take into account the following factors:- 1. Prima facie viability of the JV/WOS outside India; 2. Contribution to external trade and other benefits which will accrue to India through such investment; 3. Financial position and business track record of the Indian Party and the foreign entity; 4. Expertise and experience of the Indian Party in the same or related line of activity of the JV or WOS outside India.

|

Sources of Funds :-

Financial Commitment Without Equity Contribution

- An Indian party may, with prior approval of RBI, undertake financial commitment without equity contribution in JV / WOS provided it is as per the business requirement of the Indian party and also as per the legal requirement of the host country.

- “Financial commitment” as defined in regulation 2 (f) of FOREIGN EXCHANGE MANAGEMENT (TRANSFER OR ISSUE OF ANY FOREIGN SECURITY) REGULATIONS, 2004 means the amount of direct investment by way of contribution to equity, loan and 100 per cent of the amount of guarantees and 50 per cent of the performance guarantees issued by an Indian party to or on behalf of its overseas Joint Venture Company or Wholly Owned Subsidiary

- Proposals from the Indian party for undertaking financial commitment without equity contribution in JV / WOS may be considered by the Reserve Bank under the approval route based on the business requirement of the Indian Party and legal requirement of the host country in which JV/WOS is located.

- Regulation 6 (4) of FOREIGN EXCHANGE MANAGEMENT (TRANSFER OR ISSUE OF ANY FOREIGN SECURITY) REGULATIONS, 2004 specifically mention the approval requirement as under:

“With prior approval of the Reserve Bank, an Indian party may undertake financial commitment without equity contribution in JV / WOS provided it is as per the business requirement of the Indian party and also as per the legal requirement of the host country.”

- Accordingly, an Indian party need to approach RBI through its AD bank to get the approval for subscribing the shares without consideration.

Transfer By Way of Sale of Shares of JV/ WOS Outside India: –

An Indian Party may transfer by way of sale to another Indian Party or to a resident outside India, any share or security held by it in a JV/ WOS outside India subject to following conditions:

- The sale does not result in any write-off of the investment made;

- In case shares of overseas JV/ WOS are listed, sale is to be effected through stock exchanges;

- In case shares of overseas JV/ WOS are not listed and shares are disinvested by a private arrangement – share price should not be less than the value derived by CA/ CPA;

- An Indian Party should not have any outstanding dues from the overseas JV/ WOS;

- The overseas JV/ WOS has been in operation for at least one full year and the APR together with audited accounts for that year has been submitted to Reserve Bank;

- An Indian Party is not under any investigation by CBI/ DoE/ SEBI/ IRDA or any other regulatory authority in India.

Further, An Indian Party may disinvest, without prior approval of the Reserve Bank, in any of the under noted cases where the amount repatriated after disinvestment is less than the original amount invested:

*The Indian Party shall ensure that the sale proceeds of shares/securities shall be repatriated within 90 days from the date of sale of shares/securities and the documentary evidence to this effect shall be submitted to the RBI through the designated AD bank.

Restrictions on Forming Step Down Subsidiary (SDS) Company :-

- There are no restrictions on entities having JVs/WOSs abroad setting up second generation operating companies (step-down subsidiaries) within the overall limits applicable for investments under the Automatic Route. However, companies wishing to set up step-down operating subsidiaries to undertake financial sector activities will have to comply with the additional requirements for direct investment in the financial services sector.

- The provisions of Notification No. FEMA 120/RB-2004 dated July 7, 2004, as amended from time to time, dealing with transfer and issue of any foreign security to Residents do not permit an IP to set up Indian subsidiary(ies) through its foreign WOS or JV nor do the provisions permit an IP to acquire a WOS or invest in JV that already has direct/indirect investment in India under the automatic route.

However, in such cases, IPs can approach the Reserve Bank for prior approval through their Authorized Dealer Banks which will be considered on a case to case basis, depending on the merits of the case.

Reporting Compliances And Obligations of Indian party Making ODI :-

*Delayed submission/ non-submission of APRs entails penal measures, as prescribed under FEMA 1999, against the defaulting Indian Party.

| One Time

|

• The Indian Company intending to make a direct investment under the automatic route is required to submit form ODI with the designated bank, duly supported by the documents listed therein. |

| Recurring | • Submit Annual Performance Report of overseas entity to the Reserve Bank of India through AD Bank.

• Submit annual return on foreign liabilities and foreign assets. • Report the details of the decisions taken by a JV/WOS regarding diversification of its activities /setting up of step down subsidiaries/alteration in its share holding pattern within 30 days of such alteration. |

| Event Wise

|

• Receive share certificates or any other documentary evidence of investment in the foreign JV / WOS as an evidence of investment and submit the same to the designated AD within 6 months.

• Repatriate to India all dues viz. dividends, royalty, technical fees, etc within 60 days of falling due. • In case of disinvestment, sale proceeds of shares/securities shall be repatriated to India immediately on receipt thereof and in any case not later than 90 days from the date of sale of the shares /securities and documentary evidence to this effect shall be submitted to the Reserve Bank through the designated AD. |

Investment in foreign securities Other than by way of Direct Investment:-

By Way Of – Gift/ Inheritance/ ESOP

- As per regulation 22 of Foreign Exchange Management (Transfer Or Issue Of Any Foreign Security) Regulations, 2004, General permission has been granted to person resident in India who is an individual:-

- to acquire foreign securities as a gift from any person resident outside India; or to acquire shares by way of inheritance from a person whether resident in or outside India; a person resident in India being an individual who is an employee/ director of Indian office/branch of a foreign entity/ subsidiary of foreign entity in India/ Indian company in which foreign entity has direct/ indirect equity holding, may accept shares offered by such foreign entity provided that:

♦ the shares under ESOP scheme are offered by the issuing company globally on uniform basis; and

♦ an annual return is submitted by the Indian company to RBI through AD Bank giving details of remittance/ beneficiary etc.

- by way of bonus/rights shares on the foreign securities already held by them. (Regulation 4)

- to acquire shares under Cashless Employees Stock Option Scheme issued by a company outside India, provided it does not involve any remittance from India

| *Meaning of PRI (Person Resident in India): –

A person residing in India for more than 182 days during the course of preceding financial year. However, it does not include a person who has come to or stays in India, in either case, otherwise than : (a) He has come for or taking employment in India (b) For carrying on business or vocation in India (c) For any other purpose, in such circumstances as would indicate his intention to stay in India for an uncertain period. |

*Meaning of PROI (Person Residing Outside India): –

Person Residing Outside India means a person who is not covered as per Defination of PRI (Person Resident in India). |

Compliance Requirements When Shares Acquired Without Consideration: –

- The Indian Party Should Report the details of the acquisition of securities by way of gift/ inheritance within 30 days of such acquisition.

- In case of ESOP issued to an employee of Indian branch/ subsidiary, the reporting shall be made in form as annexed below as an Annexure A.

Annex – A

ESOP Reporting

Statement of shares allotted to Indian employees / directors under ESOP

Schemes for the year ended March ______________

(to be submitted on the letterhead of the company through their AD bank)

We, M/s………………….., (Indian company) hereby declare that :

a) M/s ……………. (foreign company) has issued ………… shares to our employees under ESOP Scheme during the year as under

(i) No. of shares allotted :

(ii) Number of employees/directors who accepted shares :

(iii) Amount remitted :

b) effective holding of the foreign company M/s ………… in the Indian company, as on March 31, ______, is not less than 51% and

c) the information furnished above is true and correct to the best of our knowledge and belief.

Signature of the Authorised Official :

Name :

Designation :

Date :

To,

The Chief General Manager

Reserve Bank of India

Foreign Exchange Department,

Overseas Investment Division,

Central Office,

Amar Bldg., 3rd Floor,

Sir. P.M. Road,

Fort,

Mumbai 400 001.

About the Author

Author is Divya Goel, ACS working as Assistant Manager- Company Secretary with Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India.