Introduction:

The article deals with Additional Tier-1 Bonds, popularly known as ‘AT-1 Bonds’ and the recent restructuring plan proposed by the Reserve Bank of India for Yes Bank which has also resulted in writing off the AT-1 Bonds in totality, while using its powers conferred by the virtue of section 45 of the Banking Regulation Act, 1949. The draft restructuring plan is still pending for approval. The Reserve Bank of India by way of the restructuring plan is trying to bring Yes Bank back on its feet from the financial woes that it has been under since last year. The article also deals with the extent of implication of the AT-1 Bonds being written off completely on the companies/individuals who have invested in the bonds.The set of investors have also approached the Hon’ble Bombay High Court against the draft scheme as proposed by the Reserve Bank of India for Yes Bank. It would be interesting to see how Indian courts would address this issue considering the large quantum of investor’s money which today stands unresolved.

What are AT-1 Bonds?[1]

AT-1 bonds or the Additional Tier Bonds are unsecured, perpetual and non-convertible bonds issued by banks in order to secure an external capital base to be used in times of a financial emergency without being subjected to insolvency and distress measures.The AT-1 bonds carry a high interest rate which plays out an alluring factor for the investors. The issuance of AT-1 Bonds was first formulated after the 2008 financial crisis that saw the infamous fall of a banking behemoth ‘The Lehman Brothers’ in United States of America. The world economy witnessed an unavoidable slump due to the liquidity crunch that all the banks in the world faced at that time. Therefore, in the wake of such distress, the central bank of India i.e. The Reserve Bank of India formulated a plan in compliance with the BASEL-III Norms to make the financial institutions maintain a certain level of liquidity and be prepared for any financial risk or any unwelcoming situation such as the 2008 financial crisis. The Banks in India started issuing AT-1 Bonds which are perpetual bonds with no fixed maturity date and which carried high interest that is higher than the interest provided with the Fixed Deposits. However, in addition to the higher interest that it promises, it also carries higher risk than other bonds which are available in the market. The bonds also carry a call option with them that allows the banks to have an option of redeeming it after 5 or 10 years depending upon the financial situation of the bank, however, the banks are not compulsorily mandated to exercise such call option, it is the banks discretion whether to redeem the AT-1’s or not . The majority of investments since the inception of AT-1 bonds have been made by big corporates, mutual fund entities and high net worth individuals (HNI’s) etc.

Key take-aways from the AT-1 Bonds[2]:

The AT-1 Bonds ensue with it very interesting aspects, which on the face of it would probably appear to be inconsequential however, it will have lasting consequences if avoided in the first place. It is significant to note that the AT-1 bonds are very different from the usual plain vanilla bonds available in the market. Even though there is a call option available with the bonds, the banks can redeem it anytime if the Common Equity Tier Ratio (CET) which is also known as CET falls below 5.5%. Also, the AT-1 bonds involve coupon payments, which can also be bailed out in case the banks are not in compliance with the BASEL-III Norms. It should also be noted that if the CET falls below 8%, it then triggers a slip in interest payouts and if it further falls below 6.125%, it triggers the cut out in the payment of the principal amount, which is also known as the ‘Principal Loss Absorption Feature’. Further, the AT-1 bonds are written off in conformity with the extant regulations issued the Reserve Bank of India based on the BASEL Framework which for the record entails absolute right to the Reserve Bank of India to write off the bonds. Further, if the Reserve Bank of India feels that any bank is under a financial crunch, it can waive off the liability of the banks to redeem the AT-1 bonds and completely write it off as it did in the restructuring scheme/plan of Yes Bank.[3]

How is Bond Market regulated in India?

There are primarily two regulators in India, which looks after the bond market i.e. The Reserve Bank of India and The Securities and Exchange Board of India (SEBI) respectively. To understand it in a more simpler sense, let me put it this way, The Reserve Bank of India is more of a facilitating authority wherein the SEBI works as a regulatory mechanism for the all the bonds traded in the market. However, if we come to corporate bond markets, there plenty of organisations regularizing the bond markets in India, like Clearing Corporation of India, Stock Exchanges etc which according to an erstwhile RBI Governor hurt the bond market and deters the flow of investments.

Then, why should one go with the AT-1 Bonds in the first place?

The AT-1 bonds also known as COCO (Contingent Convertible Bonds) in Europe carries a very high interest and is perpetual in nature, which acts as an alluring factor for such bonds. These bonds are primarily for people who are not looking for regular income or secured funding rather for corporates who want to invest big and probably not looking for short-term liquidity or early redemption. The call option available with the Bonds gives an option to the issuerto redeem it within a span of 5 years or 10 years but the issuer is under no obligation to exercise such call options.

Does investment made through AT-1 bonds secure any right?

Normally, there are two routes to acquire AT-1 Bonds, one is Initial Private Placement and second one is the routine market purchase of already traded AT-1 Bonds. It may also not out of place to question that since, there is a considerable amount of investment made through the purchase of AT-1 Bonds, will it not secure any right against the investment made by the bond holders? Since, when you buy a bond of a company, essentially you are lending money to the company and that is the reason why raising money through bonds is considered to be a debt financing. Now, can we say that bondholders are equivalent to creditors of the banks since; they have lent money to the bank by purchasing bonds i.e. AT-1 Bonds from the bank. Before going any further, we need to analyze the definition of creditor. The definition of creditor can be found under section 2(10) of the Insolvency and Bankruptcy Code, 2016, it states that “creditor” means any person to whom a debt is owed and includes a financial creditor, an operational creditor, a secured creditor, an unsecured creditor and a decree-holder”.

Now, considering the definition of creditor, one would wonder that, the bondholders shall be considered under the definition of creditors and the RBI while writing them off entirely qua the restructuring plan of YES Bank has forged out an intelligible differentia between the bondholders and other creditors of the bank. However, it may also be not out of place to mention that the Reserve Bank of India has defined powers under section 45 of the Banking Regulation Act, 1949 which empowers it to take such adverse measures. It is pertinent to note that, the Reserve Bank of India, has proposed the restructuring plan/scheme by virtue of powers guaranteed under section 45 of the Banking Regulation Act, 1949.

AT-1 Bonds in other countries:

AT-1 Bonds in other countries are also known as COCO Bonds (Contigent Convertible Bonds) especially in Europe. The Banks in the world started with the issuance of additional tier-1 bonds or the perpetual bonds only after the massive financial crisis that the world banking sector witnessed in the year 2008. The COCO Bonds can be assailed as a savior package for situations such as the financial crisis of 2008. It was proposed to be issued by various other central banks of other countries in order to safeguard the banks and put the banks in a situation so as to absorb any losses in case of a financial breakdown. The COCO bonds have been primarily present in the market since the year 2014. As the data suggests that banks such as Societe Generale, Credit Suisse, Deutsche Bank, Royal Bank of Scotland has issued such bonds to the tune of $101 Billion from April, 2013 to early 2016. However, there were many speculations doing the rounds regarding the capacity of banks in different countries being able to service the AT-1 Bonds or the COCO Bonds. Even in the Middle-East countries, the AT-1 Bonds have been meted out with plenty of investments, for instance, Al Hilal Bank, being from one of richest states in the world i.e. Abu Dhabi received a good response after floating Additional Tier Bonds. However, few banks in Europe tried to convert the debt based bonds i.e. COCO Bonds as they are popularly known as in Europe into equity however, it was not met with feasible outcomes in the market. The diabolical aspect attached to such bonds makes it highly risky at one hand but also an interested area of investment for entities which are looking for higher returns on their investment. The issuer of such bonds, in a scenario of financial meltdown, may write down, write-off or convert such bonds to equity. [4]

With respect to the other banks in the world deciding upon writing off the perpetual bonds or the AT-1 Bonds, there are few instances which could be certainly highlighted here. Last year, Bank of Jinzhou[5] decided to skip the interest payment to its international bondholders after reporting losses in 2019. Also, in February, 2019, Banco Santander SA of Spain failed to redeem the issued bonds as expected. The Arste Bank of Austria[6] very recently also failed to stand up to their coupon payments for their COCO Bonds, however, in 2016, it was able to pay an 8.875% coupon which was more than 2.5 times of what the bank was paying on the new issues.[7]

Does power of restructuring conferred to RBI under section 45 of the Banking Regulation Act, 1949 calls for an intervention considering the quantum of investments made by varuious corporate entities and HNI’S?

The Reserve Bank of India by way of section 45 of the Banking Regulation Act, 1949 has powers to suspend the operations of a bank and to propose a scheme of arrangement for the banks. It is stated in section 45(3) (d) that ‘in the interest of the banking system of the country as a whole, it is necessary so to do, the Reserve Bank may prepare a scheme-

(i) For the reconstruction of the banking company, or

(ii) For the amalgamation of the banking company with any other banking instituion (in this section referred to as “the transferee bank”)

Further, the section 45(f) states that ‘the reduction of interest or rights which the members, depositors and other creditors have in or against the banking company before its reconstruction or amalgamation to such extent as the Reserve Bank considers necessary in public interest or in the interest of members, depositors and other creditors or for the maintenance of the business of the banking company;

While, section 45(h) of the Banking Regulation Act, 1949 states that ‘the allotment to the members of the banking company for shares held by the them therein before its reconstruction or amalgamation [whether their interest in such shares has been reduced under clause (f) or not], of shares in the banking company on its reconstruction or, as the case may be, in the transferee bank and where any members claim payment in cash and not allotment of shares, or where it is not possible to allot shares to any members, the payment in cash to those members in full satisfaction of their claim-

(i) in respect of their interest in shares in the banking company before its reconstruction or amalgamation; or

(ii) where such interest has been reduced under clause (f) in respect of their interest in shares as so reduced;……….

Now, if read the aforementioned section with the definition of creditor as defined under section 2(10) of the Insolvency and Bankruptcy Code, 2016, the AT-1 Bondholders falls within the purview of creditors and hence, there could be reduction in the interest/rights of the creditors and not complete extinguishment. But at the same point one would argue that the AT-1 Bonds are basically issued with a caveat that if the banks has any liquidity crunch, it may use extinguishment of these bonds in order keep the liquidity pressure at bay.

It becomes pertinent to mention that very recently, AT-1 Bond holders moved before Hon’ble High Court of Bombay by way of a writ petition wherein they have challenged the intelligible differentia perpetuated at behest of the plan/scheme proposed by the Reserve Bank of India. They have also argued that since with more savior package pumped into YES Bank, the bank will be in a much better condition to carry the commitments tethered with AT-1 Bonds and hence, they have argued to not extinguish it completely rather to be allowed to continue with the bank further. The said writ petition is pending adjudication and the outcome will provide certainty to the manner in which the bondholders would be treated alongside other creditors and promoters.

It is also to be noted that according to a RBI Circular in 2015, the instruments that fall under Tier-1 Capital such as the AT-1 Bonds would be considered just above equity but lower than other creditors while assimilating the claims if then bank goes into financial trouble.

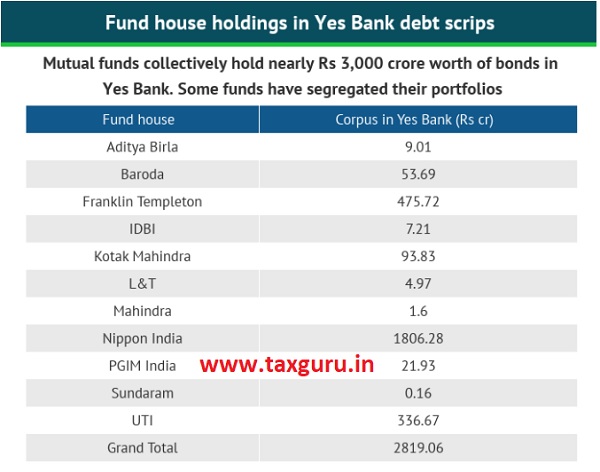

With respect to the YES Bank situation, it cannot be ignored that there are huge investments made by various investors mostly mutual fund entities and HNI’S having exposure of around Rs.2,819 crores. The Bank of Baroda Mutual Fund- Baroda Treasury Advantage Fund and Baroda Credit Risk Fund have investments worth of Rs.53.49 crores; UTI Mutual Bonds has investments of around Rs.50 crores and most strikingly, Indiabulls Housing Finance have investments of Rs.662 crores. It may not out of place to mention that Indiabulls Housing Finance is already in a great financial trouble right now and a write off around Rs.662 crores will further worsen the already precarious situation. Apart from the abovementioned investors, the senior citizen investors who were misguided by the Fund Managers into buying such bonds would also have to borne the heat. It is significant to note there are around 11 fund which hold a nearly Rs.3,000 crore according to a news report published in the moneycontrol.

Since, the parameters of the restructuring has already been defined under section 45 of the Banking Regulation Act, 1949, it would be interesting to see the manner the Hon’ble High Court of Bombay will deal with the issue considering the stake of investors involved in AT-1 Bonds.

Conclusion:

It can be said that the underlying idea to introduce AT-1’s or CoCo’s is to help the banks to absorb losses in case of a financial trouble and to also comply with the BASEL-III Norms. However, if the situation of bondholders of Yes Bank is to be discussed, it can be said that the holders have been kept in the dark whilst pitching them such bonds. Also, the intelligible differentia as derived by the Reserve Bank of India in their draft scheme between the AT-1 Bondholders and the Promoters/Creditors perpetuates cynicism in the bond market. The total exposure of the AT-1’s held with Yes Bank stands at around Rs.2800 Crores. Since, this is a first for Indian investors wherein their value of investment in high risk bonds has been completely depleted, it will be interesting to see what the courts decide more specifically, the Hon’ble Bombay High Court. It will also be an eye opener for the investors and will definitely have a consequential impact on the Indian Bonds market.

Notes:-

[1] https://www.thehindubusinessline.com/opinion/columns/slate/all-you-wanted-to-know-about-at-1-bonds/article31024984.ece#

[2]https://economictimes.indiatimes.com/markets/bonds/perpetual-bonds-draw-attention-from-regulators/articleshow/68677540.cms?from=mdr

[3] https://www.financialexpress.com/market/cafeinvest/additional-tier-i-bonds-perpetual-bonds-the-case-of-yes-bank/1893437/

[4] https://www.euromoney.com/article/b12kqjlwvsz26k/at1-capitalcoco-bonds-what-you-should-know

[5] https://www.wsj.com/articles/ailing-chinese-bank-stops-paying-coupons-on-coco-bonds-11567424965

[6] https://www.washingtonpost.com/business/a-coco-bond-at-3375percent-the-markets-still-crazy/2020/01/23/7a9435ae-3db6-11ea-afe2-090eb37b60b1_story.html

[7]https://in.reuters.com/article/us-europe-banks-bankcapital/banks-gear-up-for-high-risk-debt-sales-in-once-in-a-lifetime-market-idINKBN1W317Q

[8] https://www.moneycontrol.com/news/business/personal-finance/explained-the-impact-of-at1-bonds-in-debt-mfs-on-investors-5014921.html

(Authors are practicing as advocates in New Delhi)

(Authors are practicing as advocates in New Delhi)

(The views expressed in this Article are based on personal understanding and interpretation of the Authors.)

Whether yes bankat1 bonds are allowable under income tax vat 1961

Whether yes bank bond s at1allowable under income tax vat 1961

Thanks for elaborate explanation of the AT1 bonds. Many small investors / retired persons had put hard earned money in those bonds of Yes banks.

How RBI can bring them on toad by such strange order.

This can not only result in some agitation but even some seal investor may subside by loosing big investment.

Pain put in by both the Authors deserves loud applause. Very informative and unique as well.