TDS/TCS ON PURCHASE/SALE OF GOODS

Finance Act, 2020 had inserted a Sub-Section (1H) in Section 206C of Income Tax Act, 1961 requiring every person to collect TCS on sale of goods from buyer w.e.f. 01-10-2020. These provisions were subject to following conditions:

1. The total sales, gross receipts or turnover from the business must exceed Rupees Ten Crore during the immediately preceding financial year in which the sale of goods is carried out.

2. Tax has to be collected only from the buyers to whom sale of more than Rs. 50 Lakhs is made during the year whether in a single bill or all the bills taken together.

3. Tax has to be collected on the amount which exceeds Rs. 50 lakhs.

4. TCS is to be collected at the time of receipt of amount from buyer.

5. TCS shall not be applicable in the following cases:

a) The buyer is Central/State Government, an embassy, a High Commission, legation, commission, consulate and the trade representation of a foreign State or a local authority or a person importing goods into India.

b) The buyer is liable to deduct TDS under any other provision of the Act and has deducted such amount on the goods purchased by him from the seller;

c) The goods mentioned below are not required to be considered for the above said provision:

-

- Alcoholic Liquor for human consumption

- Tendu leaves

- Timber obtained under a forest lease

- Timber obtained by any mode other than under a forest lease

- Any other forest produce not being timber or tendu leaves

- Scrap, Minerals, being coal or lignite or iron ore

- Motor vehicle

- Foreign remittance through Liberalised Remittance Scheme

- Selling of overseas tour package

- Where the goods are exported out of India.

6. TCS is required to be collected at the rate of 0.1% of the amount in excess of Rs. 50 Lakhs.

7. If the buyer does not provide PAN or Adhar Number, then the rate shall be 1 %.

8. TCS is required to be collected @ 5% if buyer has not filed the returns of income for both of the two previous years immediately prior to the previous year in which tax is required to be collected, and the aggregate of tax deducted at source and tax collected at source in his case is rupees fifty thousand or more in each of these two previous years:

9. The person needs to check the applicability on year on year as well as specific to each buyer basis on PAN India not GSTIN Basis.

Now, Finance Act 2021 has inserted a new section 194Q in Income Tax Act, 1961 which requires a person to deduct tax from payments made against purchase of goods.

These provisions are subject to following conditions:

1. These Provisions are effective from 01-07-2021

2. The total sales, gross receipts or turnover of the person from the business must exceed Rupees Ten Crore during the immediately preceding financial year in which the purchase of goods is carried out;

3. Tax has to be deducted only from the sellers from whom purchase of more than Rs. 50 Lakhs is made during the year whether in a single bill or all the bills taken together.

4. Tax has to be deducted on the amount which exceeds Rs. 50 lakhs.

5. The provisions of this section shall not apply to a transaction on which—

(a) tax is deductible under any other provisions of the Act; and

(b) tax is collectible under the provisions of section 206C other than a transaction to which sub-section (1H) of section 206C applies. These transactions are:

-

- Alcoholic Liquor for human consumption

- Tendu leaves

- Timber obtained under a forest lease

- Timber obtained by any mode other than under a forest lease

- Any other forest produce not being timber or tendu leaves

- Scrap, Minerals, being coal or lignite or iron ore

- Motor vehicle

- Foreign remittance through Liberalised Remittance Scheme

- Selling of overseas tour package

6. TDS is required to be deducted @ 0.1% of the amount in excess of Rs. 50 Lakhs.

7. In following two situations, TDS is required to be deducted @ 5%.

- If the seller does not provide PAN or Adhar Number, or

- If Seller has not filed the returns of income for both of the two previous years immediately prior to the previous year in which tax is required to be deducted, and the aggregate of tax deducted at source and tax collected at source in his case is rupees fifty thousand or more in each of these two previous years:

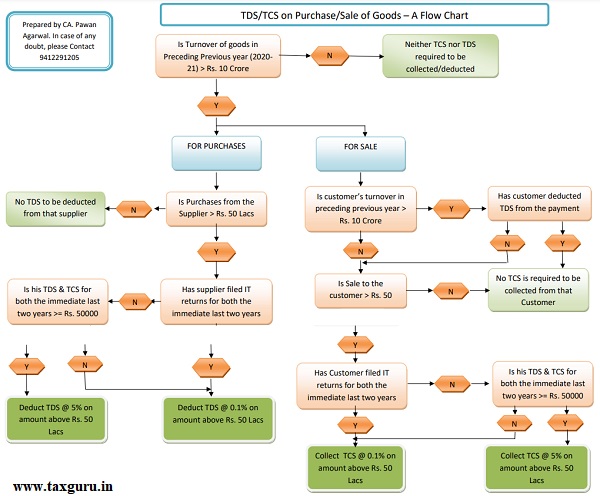

The law of two sections cumulatively can be summarized as under:

1. If the turnover of the person in preceding previous year is less than Rs. 10 Crore, he is neither required to deduct TDS nor required to collect TCS.

2. If the turnover of person is more than Rs. 10 Crore then

A. For Purchases made by Person

a. he has to deduct TDS @ 0.1% from that supplier from whom he is purchasing goods worth more than Rs. 50 Lacs in a previous year. The tax is required to be deducted only on the amount in excess of Rs. 50 lacs.

b. If however, supplier has not filed the returns of income for both of the two previous years immediately prior to the previous year in which tax is required to be deducted, and the aggregate of tax deducted at source and tax collected at source in his case is rupees fifty thousand or more in each of these two previous years, the rate of deduction shall be 5%.

b. For Sales made by Person

a. He has to obtain details of turnover of all his customers.

b. Wherever, turnover of customer is 10 crore or less, the person is required to collect TCS @ 0.1% from his customer at the time of receipt of payment in excess of Rs. 50 Lacs.

c. Wherever turnover of customer is greater than Rs. 10 crore, he has to see whether his customer has deducted TDS from the payment. If TDS is deducted by customer, the person is not required to collect TCS. If, customer has not deducted TDS, he has to collect TCS @0.1%.

d. In all the aforesaid cases, where person has to collect tax, he is required to collect tax @ 1% if his customer has not furnished his PAN.

e. In all the aforesaid cases, where person has to collect tax, he is required to collect tax @ 5% if his customer has not filed the returns of income for both of the two previous years immediately prior to the previous year in which tax is required to be collected, and the aggregate of tax deducted at source and tax collected at source in his case is rupees fifty thousand or more in each of these two previous years.

It may be noted that these provisions are applicable only on sale/purchase of GOODS.

The provisions have also been summarized in a form of Flow Chart for easy understanding. The flow Chart is also attached herewith.

Client is deducting TCS on Sale bills instead of Receipts. the amount of sale is less than the amount received due to which tcs deducted by the party is less than the tcs to be collected. What we have to do in that case.

If buyer deducted TDS on our sales then is it required to collect TCS?

No, you are not required to collect TCS if buyer has deducted TDS

So much complications. this is not good for business

VERY WELL EXPLAINED ARTICLE CONGRATS CA PAWAN AGARWAL JI.

Sad that govt keeps on complicating life for SMEs…..first gst with its countless forms and rules, and now this. So much burden on SMEs.

Nicely explained the provisions.

Well explained Sir.

The applicability conditions: Is the TO limit exceeding 10Cr or Gross receipt? Like TO is 9Cr and GST @ 18% 1.62Cr total 10.62Cr.