Tax Audit Report (Form 3CD- Applicability of Clause 30C & Clause 44 deferred till March 31, 2021

Central Board of Direct Taxes (CBDT) has issued Circular No. 10/2020 dated April 24, 2020 by which the CBDT has deferred the applicability of certain Clause of Form 3CD (Tax Audit Report) till March 31, 2021.

Order under Section 119 of the Income-tax Act, 1961

“Section 44AB of the Income-tax Act, 1961 (‘the Act’) read with rule 6G of the Income-tax Rules, 1962 (‘the Rules’) requires specified persons to furnish the Tax Audit Report along with the prescribed particulars in Form No. 3CD. The existing Form No. 3CD was amended vide notification no. GSR 666(E) dated 20th July, 2018 with effect from 20th August, 2018. However, the reporting under clause 30C and clause 44 of the Tax Audit Report was kept in abeyance till 31st March, 2019 vide Circular No. 6/2018 dated 17.08.2018, which was subsequently extended to 31 .03.2020 vide Circular No. 9/2019.

Several representations were received by the Board with regards to difficulty in implementation of reporting requirements under clause 30C and clause 44 of the Form No. 3CD of the Income-tax Rules, 1962 in yiew of the Global Pandemic due to COVID-19 virus and requested for deferring the applicability of the above provisions.

The matter has been examined and in view of the prevailing situation due to COVID- 19 pandemic across the country, it has been decided by the Board that the reporting under clause 30C and clause 44 of the Tax Audit Report shall be kept in abeyance till 31 st March, 2021.”

Brief introduction of Clause 30C and Clause 44 of the Form 3CD which is deferred till March 31, 2021 as mentioned below:

A) Clause 30C:

30C. (a) Whether the assessee has entered into an impermissible avoidance arrangement, as referred to in section 96, during the previous year? (Yes/No.)

(b) If yes, please specify:-

(i) Nature of impermissible avoidance arrangement:

(ii) Amount (in Rs.) of tax benefit in the previous year arising, in aggregate, to all the parties to the arrangement:

The definition of ‘impermissible avoidance arrangement’ U/s 96 of Income-tax Act is as mentioned below:

(1) An impermissible avoidance arrangement means an arrangement, the main purpose of which is to obtain a tax benefit, and it-

(a) creates rights, or obligations, which are not ordinarily created between persons dealing at arm’s length;

(b) results, directly or indirectly, in the misuse, or abuse, of the provisions of this Act;

(c) lacks commercial substance or is deemed to lack commercial substance under section 97, in whole or in part; or

(d) is entered into, or carried out, by means, or in a manner, which are not ordinarily employed for bona fide purposes.

(2) An arrangement shall be presumed, unless it is proved to the contrary by the assessee, to have been entered into, or carried out, for the main purpose of obtaining a tax benefit, if the main purpose of a step in, or a part of, the arrangement is to obtain a tax benefit, notwithstanding the fact that the main purpose of the whole arrangement is not to obtain a tax benefit.

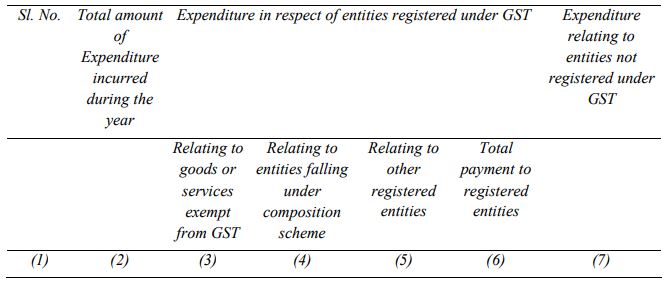

B) Clause 44:

Break-up of total expenditure of entities registered or not registered under the GST:

Please reach out to us at +919711132615 or write us: mishradevesh12@gmail.com for any further query.

Please reach out to us at +919711132615 or write us: mishradevesh12@gmail.com for any further query.

In this crucial time, we request all of you to stay back at your home and keep yourself and your family safe from COVID-19.

Author Bio