Section 44AD versus Section 44AB: What to choose ?

As per recent amendments in Finance Act, 2020 where one of major amendment was made in Section 44AB by inserting a proviso to clause (a), which reads as follows:-

Audit of accounts of certain persons carrying on business or profession.

44AB. Every person,—

(a) carrying on business shall, if his total sales, turnover or gross receipts, as the case may be, in business exceed or exceeds one crore rupees in any previous year

Provided that in the case of a person whose—

(a) aggregate of all amounts received including amount received for sales, turnover or gross receipts during the previous year, in cash, does not exceed five per cent of the said amount; and

(b) aggregate of all payments made including amount incurred for expenditure, in cash, during the previous year does not exceed five per cent of the said payment,

this clause shall have effect as if for the words “one crore rupees”, the words “five crore rupees” had been substituted;

The above amendment is interpreted as follows:-

1. Applicability:-

To Individual, HUF, AOP/ BOI, Partnership firm, Company (Private/ Public) or LLP Carrying Business and not Profession

2. This amendment becomes effective from Assessment Year: 2020-2021.

3. Revised Threshold Limit : Rs. 5 Crores instead of Rs. 1 crore

4. Revised Threshold Limit is subject to following conditions:-

a) The aggregate amount of receipts (including Revenue receipts and Capital receipts of any nature) in cash during the previous financial does not exceed 5% of such receipts.

AND

b) The aggregate amount of payments (including Revenue Payments and Capital Payments of any nature) in cash during the previous financial does not exceed 5% of such payments.

5. The conditions mentioned in points 4 needs to be fulfilled cumulatively.

The above amendments has created different Turnover slabs for Decision making between section 44AB or Section 44AD because section 44AD has an overriding effect over clause (a) of section 44AB.

The Turnover slabs are follows :-

| Turnover | Cash Receipts and Cash Payments | Profit => 8% / 6% | Is Tax Audit Applicable? |

| Less Than 1 Crore | Not Applicable | Not Applicable | No |

| More than 1 Crore but upto 2 Crores | Upto 5% | Not Applicable | No |

| More than 1 Crore but upto 2 Crores | More than 5% | Not Applicable | Yes |

| More than 2 Crores but upto 5 Crores | Upto 5% | Not Applicable | No |

| More than 2 Crores but upto 5 Crores | More than 5% | Not Applicable | Yes |

| More than 5 Crores | Not Applicable | Not Applicable | Yes |

Now the question arises,

As per Act, the threshold limit is either 1 Crore or 5 Crores then why I have created the one more slab of More than 1 Crore but upto 2 Crores ?

Answer:-

This is because Section 44 AD comes into play at this slab which has following conditions:-

1. Applicability :- Individual, HUF or Partnership Firm but excludes LLP.

2. Carrying on business other than plying , hiring or leasing of Carriage Goods

3. Specifically not applicable to person carrying on the business of Commission.

4. Turnover Threshold is Upto Rs. 2 Crore

5. Deemed Profit is 8% / 6% or more of Gross Receipts/ Turnover

6. As per sub-section (4) and (5) of Section 44AD,

a) Assessee should maintain assessibility under Section 44AD for 5 Consecutive Assessment Years.

b) If the condition a) above is not satisfied then Assessee cannot avail benefit under section 44AD for nxt 5 consecutive assessment years. Also, the assessee has to maintain books of Accounts under section 44 AB and if the profit exceeds basic exemption limit then assessee has to get the accounts audited also irrespective of Turnover of Rs 1Crore or Rs 5 Crore

c) Also, apart from above if the assessee declares profit less than deemed profit under section 44AD or in case of loss then also Assessee needs to maintain books of accounts.

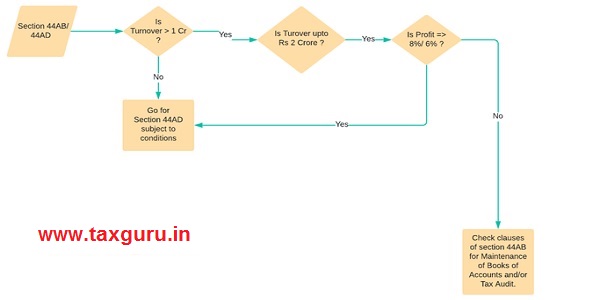

Hence to decide whether to opt for Section 44AD or Section 44AB following flow chart may help.