Case Law Details

Mangadu Natarajan Balasundharam Vs ITO (ITAT Chennai)

The Income Tax Appellate Tribunal (ITAT), Chennai allowed the appeal of the assessee and deleted the penalty levied under Section 271(1)(c) of the Income-tax Act for Assessment Year 2016-17.

The assessee, an individual, originally filed the return of income on 14 October 2016, declaring taxable income of Rs. 10,82,190. Subsequently, the Assessing Officer (AO) received information from the DDIT (Investigation) that the assessee had not disclosed income arising from the sale of plots jointly owned with two other persons. Based on this information, the AO initiated reassessment proceedings by issuing a notice under Section 148A(b), passed an order under Section 148A(d), and thereafter issued a notice under Section 148.

In response to the notice under Section 148, the assessee filed a fresh return on 27 April 2023, declaring total income of Rs. 93,19,140, which included Long-Term Capital Gains (LTCG) of Rs. 82,36,957 arising from the sale of the plots. The AO completed the reassessment under Section 147 by accepting the income disclosed in the return filed pursuant to Section 148 without making any further additions or disallowances.

Despite accepting the reassessed income, the AO initiated penalty proceedings under Section 271(1)(c) on the ground that the assessee had concealed income by not offering the LTCG in the original return filed under Section 139(1). Holding that the assessee had failed to provide a satisfactory explanation for the omission, the AO imposed a penalty of Rs. 16,96,813, being 100% of the tax attributable to the concealed income. The Commissioner of Income Tax (Appeals) upheld the penalty after rejecting the assessee’s explanation that he was unaware the capital gains were taxable in his individual hands.

Before the Tribunal, the assessee contended that although the LTCG had not been disclosed in the original return, it was voluntarily included in the return filed in response to the notice under Section 148. It was argued that the AO had accepted the revised return in its entirety without making any additions, and therefore there was no concealment of income. The assessee relied on the decision of the Madhya Pradesh High Court in CIT v. Suresh Chandra Mittal, which held that where a revised return is accepted and the explanation is found to be bona fide, penalty under Section 271(1)(c) is not justified. The assessee also pointed out that the Supreme Court had dismissed the Special Leave Petition against that decision.

The Revenue argued that the facts were distinguishable because the assessee disclosed the LTCG only after reassessment proceedings had been initiated and would not have offered the income otherwise. Accordingly, it submitted that the penalty for concealment had been rightly imposed.

After examining the record, the Tribunal observed that the reassessment was initiated because the LTCG had not been offered in the original return. However, the assessee disclosed the entire LTCG in the return filed under Section 148, and the AO accepted the returned income without making any additions or disallowances.

The Tribunal analysed Section 271(1)(c) and Explanation 1, noting that penalty is attracted where an assessee conceals income or furnishes inaccurate particulars, and where the explanation offered is either false or not substantiated. It observed that concealment generally involves an active attempt to hide income from assessment.

The Tribunal rejected the Revenue’s argument that the omission in the original return alone established concealment. It held that once the AO completed the reassessment by accepting the income disclosed in the return filed under Section 148 without making any further additions, the levy of penalty was not sustainable. The Tribunal also noted that the assessment order itself recorded that the assessee had disclosed gains from transactions which were not even part of the investigation report, reflecting the assessee’s bona fide intention.

According to the Tribunal, the test for concealment cannot be based merely on comparing the original return with the return filed under Section 148 when the reassessment has been completed entirely on the basis of the latter. It reiterated that disclosure of higher income in a revised or reassessment return does not automatically amount to concealment, particularly where the returned income is accepted without modification.

Holding that the conditions for levy of penalty under Section 271(1)(c) were not satisfied, the Tribunal set aside the penalty and allowed the assessee’s appeal.

FULL TEXT OF THE ORDER OF ITAT CHENNAI

This appeal by the assessee is against the order of the Commissioner of Income Tax (Appeals)/National Faceless Appeal Centre (NFAC), Delhi, (in short “CIT(A)”) passed u/s. 250 of the Income Tax Act, 1961 (in short “the Act”) dated 28.07.2025 for Assessment Year (AY) 2016-17.

2. The assessee is an individual and filed the return of income for AY 2016-17 on 14.10.2016 declaring taxable income of Rs.10,82,190/-. The A.O received information from DDIT(Investigation) that the assessee has not offered the income from sale of plots co-owned by him along with two others.

The A.O therefore issued a notice u/s. 148A(b) of the Act and passed an order u/s. 148A(d) of the Act. The A.O reopened the assessment by issue of notice u/s. 148 of the Act. The assessee in response to the notice issued u/s. 148 of the Act filed the return of income on 27.04.2023 offering an income of Rs.93,19,140/- after including the Long Term Capital Gain (LTCG) on sale of plots to the tune of Rs.82,36,957/-. The A.O completed the assessment u/s. 147 of the Act accepting the income offered by the assessee in the return filed in response to notice u/s. 148 of the Act. Subsequently, the A.O initiated penalty proceedings u/s. 271(1)(c) of the Act for concealment of income towards LTCG not offered by the assessee in the original return of income filed u/s. 139(1) of the Act. The A.O held that the assessee failed to furnish proper explanation to substantiate the bonafide reason for not offering the LTCG and therefore the A.O levied penalty of Rs. 16,96,813/- being 100% of tax. Aggrieved, the assessee filed further appeal before the CIT(A). The CIT(A) confirmed the penalty rejecting the plea of the assessee he was not aware that the income on sale of land should be offered to tax in his individual hands. The assessee is in appeal before the Tribunal against the order of the CIT(A).

3. The Ld. Authorized Representative (AR) of the assessee submitted that the assessee though did not offer the LTCG while filing the original return of income has included the same while filing the return in response to notice u/s. 148 of the Act. The Ld. AR further submitted that the A.O has accepted the income as per the return filed in response to notice u/s. 148 of the Act without making any additions. The Ld. AR accordingly submitted that there is no concealment of income by the assessee since the return filed in response to notice u/s. 148 of the Act replaces return filed originally by the assessee. The Ld. AR in this regard placed reliance on the decision of the Hon’ble Madhya Pradesh High Court in the case of CIT vs. Suresh Chandra Mittal [2002] 123 Taxman 1052 (MP), where it has been held that:

“5. We find ourselves in agreement with the view taken by the Tribunal. It is well-settled that under section 271(1)(e), the initial burden lies on the revenue to establish that the assessee had concealed the income or had furnished inaccurate particulars of such income. The harden shifts to the assessor only if he fails is offer any explanation for the undisclosed income or offers an explanation which is found to be false by the assessing authority. However, the proviso to Explanation / provides for shifting of this burden again where the explanation offered by the assessee is found to be bona fide

6. In the present case, though it is true that the assessee had not surrendered at all and that he had done so on the persistent queries made by the Assessing Officer, but once the revised assessment was regularised by the revenue and once the assessing authority had failed to take any objection in the manner, the declaration of income made by the assessee in his revised returns and his explanation that he had done so to buy peace with the department and to come out of vexed litigation could be treated as bona fide in the facts and circumstances of the case. Therefore, the Tribunal was justified in cancelling the penalty levied by the Assessing Officer and affirmed by the Commissioner (Appeals) in the facts and circumstances of the case. This reference is, accordingly, answered in the affirmative holding that the Tribunal was justified in doing so.”

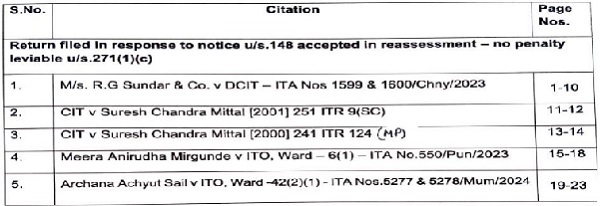

4. The Ld. AR also brought to our attention that the SLP filed against the above decision of the Hon’ble High court is dismissed by the Hon’ble Supreme Court [(2001) 119 Taxman 433 (SC)]. The Ld. AR also placed reliance on the following judicial precedence –

5. The Ld. Departmental Representative (DR), on the other hand, submitted that the decision relied on is factually distinguishable since the assessee voluntarily offered the income to buy peace in the said case. The ld. DR further submitted that in the present case the assessee offered the LTCG only in response to the notice issued u/s. 148 of the Act but for which the LTCG would not have been offered by the assessee. The Ld. DR accordingly argued that the levy of penalty for concealment of income is correctly levied in the assessee’s case.

6. We have heard the parties, and perused the material available on record. The A.O reopened the assessment for the reason that the assessee has not offered the income arising from sale of a plot of land during the year under consideration. The assessee filed return in response to notice u/s.148 of the Act wherein the assessee has included the LTCG arising from the sale of land. The AO while completing the assessment u/s.148 accepted the income returned by the assessee without making any other additions/disallowances. The AO subsequently levied penalty u/s.271(1)(c) stating that there is a concealment of income towards LTCG not declared by the assessee in the original return of income filed u/s.271(1)(c). The AO while doing so held that the assessee cannot take shelter under Explanation-1 to Section 271(1)(c). Therefore, before proceeding further we will first look at the relevant provisions –

“271. (1) If the Assessing Officer or the Commissioner (Appeals) or the Principal Commissioner or Commissioner in the course of any proceedings under this Act, is satisfied that any person—

(a) & (b)***

(c) has concealed the particulars of his income or furnished inaccurate particulars of such income, or

(d)******

he may direct that such person shall pay by way of penalty,—

Explanation 1.—Where in respect of any facts material to the computation of the total income of any person under this Act,—

(A) such person fails to offer an explanation or offers an explanation which is found by the Assessing Officer or the Commissioner (Appeals) or the Principal Commissioner or Commissioner to be false, or

(B) such person offers an explanation which he is not able to substantiate and fails to prove that such explanation is bona fide and that all the facts relating to the same and material to the computation of his total income have been disclosed by him,

then, the amount added or disallowed in computing the total income of such person as a result thereof shall, for the purposes of clause (c) of this sub-section, be deemed to represent the income in respect of which particulars have been concealed.”

7. Section 271(1)(c) of the Act is attracted where, in the course of any proceedings under the Act, the AO or the first appellate authority is satisfied that: (a) any person has concealed the particulars of his income; or (b) has furnished inaccurate particulars of such income. The expressions ‘has concealed’ and ‘has furnished inaccurate particulars’ have not been defined either in the section or elsewhere in the Act. However, notwithstanding differences in the two circumstances, they lead to the same effect, viz., keeping off a certain portion of income. Explanation 1 automatically comes into operation when, in respect of any facts material to the computation of total income of any person, there is failure to offer an explanation or an explanation is offered which is found to be false by the AO or the first appellate authority, or an explanation is offered which is not substantiated. In such a case, the amount added or disallowed in computing the total income is deemed to represent the income in respect of which particulars have been concealed. The term “concealment” in general parlance represents an active, direct attempt to hide any particular income from being assessed to tax. The Explanation-1 conveys the similar meaning where it states that the income would be treated as concealed when the explanation offered by the assessee with regard to any amount added or disallowed is not substantiating the bonafide intention and that the facts and materials to the computation have been disclosed by him. Now the question before us is whether the additional income of LTCG offered by the assessee in response to notice u/s.148 would amount to concealment of income. The argument of the revenue is that but for the initiation of reassessment the assessee would not have offered the LTCG to tax and therefore there is concealment. In our considered view, the said contention cannot be accepted for the reason that the AO has completed the assessment based on the return filed by the assessee in response to notice u/s.148 where the assessee has offered the LTCG and that the AO has accepted the income returned in the said return. It is relevant to mention here that the AO in assessment order has recorded a specific finding that the assessee has offered the gain from transactions which were not even part of the investigation report and the said finding according to the Ld. AR reflects the bonafide intention of the assessee. Further, Explanation-1 specifically provides that the explanation offered by the assessee with regard to amount added or disallowed is not well substantiated then it would amount to concealment. In the present case, it is an admitted fact that the AO while completing the assessment considering the return filed in response to notice u/s.148 where the assessee has included the LTCG and that the AO has accepted the income returned by the assessee without making any additions or disallowances. Therefore, there is merit in the submission that when the income returned in response to notice u/s.148 is accepted then levying penalty u/s.271(1)(c) for concealment is not tenable. It is a settled legal position that the disclosure of higher income in the revised return by the assessee does not automatically result in concealment, more so when the AO has completed the assessee based on such revised return without making any additions or disallowances. In other words, the test of concealment in our considered view cannot be based on comparing the income in the original return filed u/s.139(1) and the return filed in response to notice u/s.148 since the AO has completed the assessment based the income returned u/s.148 without making any additions. In view of these discussions and considering the judicial precedence in this regard, we hold that the AO is not correct in levying penalty u/s.271(1)(c) of the Act in the present case after having completed the assessment accepting the income returned u/s.148 of the Act.

8. In the result, the appeal of the assessee is allowed.

Order pronounced on 09th day of April, 2026 at Chennai.

Author Bio