Beyond the Grave: The Fiscal Ghost How the Law Handles Tax Liability After a Taxpayer’s Demise

It is a foundational tenet of modern jurisprudence that death terminates an individual’s legal personality. In the eyes of the revenue authorities, however, a taxpayer’s financial shadow lingers long after their passing.

For surviving family members, navigating the immediate aftermath of a loss is a deeply emotional process. Yet, the machinery of fiscal administration waits for no one. Under the framework of Section 159 of the Income Tax Act, 1961, death does not discharge a citizen’s tax obligations. Instead, it systematically transfers the mechanical burden of tax compliance and debt settlement straight to their legal representatives.

For tax professionals and estate executors, managing this transition requires balancing meticulous compliance with a clear understanding of the statutory boundaries designed to protect heirs from personal financial liability.

The Statutory Mantle: Who Steps into the Taxpayer’s Shoes?

When a taxpayer passes away, the law requires a live entity to step into their place to settle accounts with the state. Section 159 formally designates the “legal representative” (LR) as deemed assessees. This means that for all intents and purposes of assessment, the representative is treated as if they were the taxpayer themselves.

If the deceased leaves behind a legally validated will, this responsibility falls squarely on the named executor. However, in intestate cases—where an individual dies without a will—the administrative burden shifts to the natural legal heirs.

To prevent chaotic disputes among surviving family members, a strict order of priority governs this responsibility:

1. The Surviving Spouse (Widow or Widower)

2. Children of the deceased

3. The Mother

4. Other legal beneficiaries or dependents

The legal representative’s duties are comprehensive. They are responsible for responding to pending assessment notices, correcting past filing discrepancies, and clearing any unpaid income tax, interest, or penalties that accumulated during the taxpayer’s lifetime.

The Asset Wall: Understanding the Limit of Liability

One of the most frequent points of anxiety for grieving families is the fear of inheriting overwhelming debt. A common misconception is that if a deceased relative owed millions in back-taxes, the children or spouse must liquidate their own personal savings to balance the ledger.

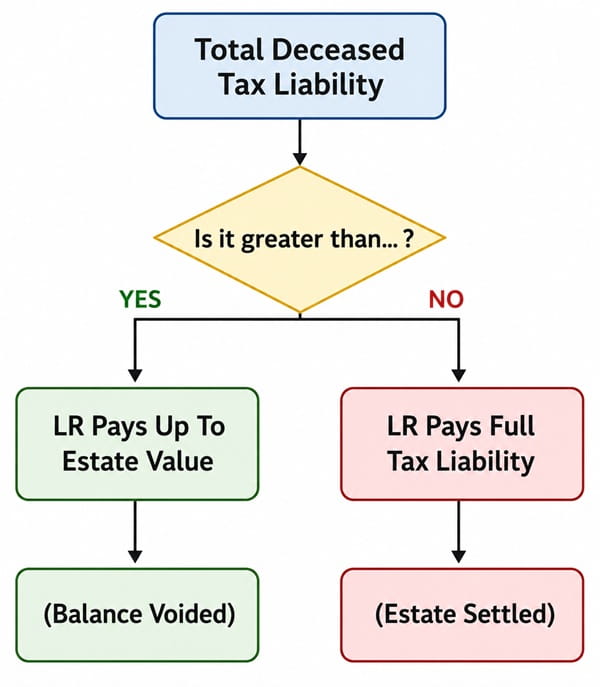

Fortunately, Section 159 establishes an ironclad protective barrier: The financial liability of a legal representative is strictly capped at the value of the estate they inherit.

The estate encompasses any asset of value left behind by the deceased, including:

- Liquid Capital: Bank savings accounts, fixed deposits, and accrued cash reserves.

- Financial Instruments: Shares, mutual fund units, debentures, and alternative investments.

- Immovable Property: Residential homes, commercial spaces, and agricultural land.

- Tangible Assets: Vehicles, jewelry, precious metals, and high-value collectibles.

If the calculated tax liability exceeds the total market valuation of these combined assets, the legal representative is not personally liable to pay the remaining deficit. The Income Tax Department cannot seize the personal assets, property, or salary of the heir to bridge the gap.

However, an important caveat exists for executors: distributing the physical or financial assets of the estate to heirs before formally discharging the tax debt can breach this protection, making the representative personally liable up to the value of the distributed property.

The Compliance Roadmap: A Four-Step Execution Workflow

Fulfilling the final obligations of a deceased taxpayer requires a disciplined, step-by-step approach to avoid processing delays or late fees:

Step 1: Information and Discovery

The legal representative must compile all financial records spanning the current financial year up to the exact date of death. This includes securing Form 26AS, Annual Information Statements (AIS), bank statements, salary slips, and sale deeds for capital gains calculations.

Step 2: Formal Portal Registration

An individual cannot simply log into the deceased’s e-filing account and submit a return. The representative must log into their own personal income tax portal account and submit a formal request to register as a “Legal Heir.” This application requires uploading the deceased’s death certificate, PAN card, the representative’s PAN card, and a legal heir certificate or probate of the will.

Step 3: Drafting and Filing the Final Return

Once approved by the portal authorities, the representative can file the final Income Tax Return (ITR) on behalf of the deceased. Crucially, the return covers only the period from April 1st of that financial year up to the exact date of death. The return status must be explicitly marked as “Deceased” within the e-filing system.

Step 4: Asset Liquidation and Settlement

With the final tax liability determined, the legal representative must use the liquid assets within the estate to pay the balance due. Only legitimate deductions, exemptions, and tax credits that the taxpayer was entitled to during their lifetime may be claimed. Once paid, all receipts, file acknowledgments, and asset valuation reports should be safely archived for future audit readiness.

CRITICAL COMPLIANCE INSIGHT

Income earned UP TO the date of death -> Filed via Deceased Individual’s ITR.

Income earned AFTER the date of death -> Filed via “Estate of the Deceased” ITR.

Pitfalls in Post-Mortem Tax Planning

Even seasoned tax professionals occasionally stumble when navigating post-mortem compliance. The most frequent error involves the misallocation of post-death income.

If a taxpayer passes away on October 1st, any interest earned on their fixed deposits or rent collected from their commercial properties up to October 1st goes onto their final personal return. However, any interest or rent generated from October 2nd onward belongs to the estate or the beneficiaries who inherited the asset. Clubbing post-death income into the deceased’s final return is a technical error that can trigger automated defect notices.

Furthermore, ignoring deadlines invites standard penalties. The Income Tax Department does not pause the accrual of interest under Sections 234A, 234B, or 234C due to a taxpayer’s demise. Delays in registering as a legal heir or failing to file before the annual statutory deadline will result in late fees and mounting interest charges that chip away at the value of the inheritance.

Final Thoughts

Closing a late taxpayer’s financial ledger is a sober but necessary administrative duty. By understanding the mechanics of Section 159, legal representatives can approach the process with confidence—safeguarding the integrity of the deceased’s estate while ensuring they remain firmly on the right side of the law.

Adv SAIJESH

Author Bio