Articles by this Author

Income Tax

Income Tax

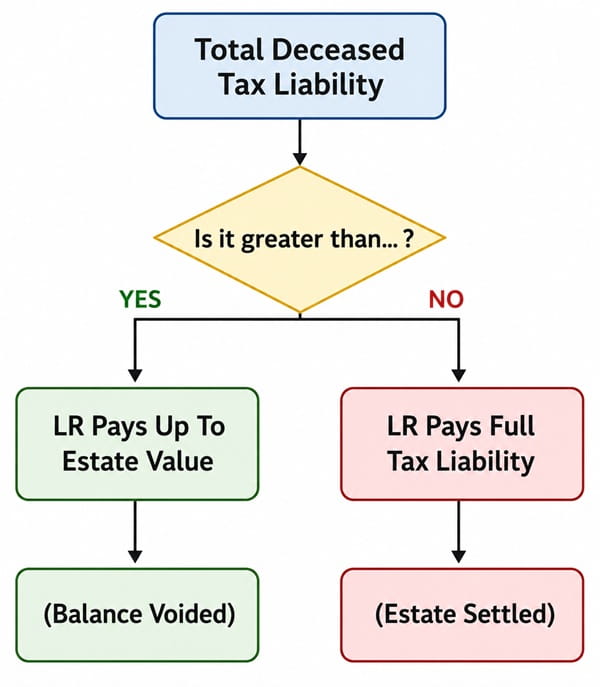

Section 159 Income Tax Rules on Legal Representative’s Liability After Taxpayer’s Death

Goods and Services Tax

Goods and Services Tax

India’s E-Way Bill System Change Effective From August 1, 2026

Income Tax

Income Tax

India’s Direct Tax Revolution: New Sections New Tax Slabs

Income Tax

Income Tax

ITR Filing Under New Tax Regime (FY 2025-26): A Complete Guide

Income Tax

Income Tax

Decoding Exempt Incomes Under Income Tax Act, 2025: From Section 10 to 11

Goods and Services Tax

Goods and Services Tax