Case Law Details

Vrinda Ispat Pvt. Ltd Vs ITO (ITAT Kolkata)

The assessee filed appeals against the orders of the National Faceless Appeal Centre for AYs 2013-14 to 2017-18. Appeals in ITA Nos. 6, 8 and 10/KOL/2025 were dismissed as withdrawn on the assessee’s request. In ITA No. 7/KOL/2025, the assessee challenged the reassessment proceedings initiated under Section 147 on the ground of limitation. The ITAT found that the notice issued under Section 148A(b) dated 30.06.2021, the notice under Section 148, and the assessment order dated 26.05.2023 were barred by limitation in view of the Supreme Court decision in PCIT v. Rajeev Bansal. The notice under Section 148 and the consequential assessment were quashed. In ITA No. 9/KOL/2025, the Tribunal held that for AY 2016-17, where reopening was initiated after three years, approval under Section 151 was required from the Principal Chief Commissioner of Income Tax. As the approval dated 14.07.2022 had been granted by the Principal Commissioner of Income Tax, it was held invalid. Consequently, the notice under Section 148 and the assessment order dated 25.05.2023 were also quashed. The remaining appeals were partly allowed by the ITAT Kolkata.

FULL TEXT OF THE ORDER OF ITAT KOLKATA

These are appeals preferred by the assessee against the orders of the National Faceless Appeal Centre, Delhi (hereinafter referred to as the “Ld. CIT(A)”] dated 03.12.2024 & 22.11.2024 for the AYs2013-14 to 2017-18.

ITA Nos. 6,8 &10/KOL/2025

2. At the outset, Ld. Counsel for the assessee requested to withdraw these appeals bearing ITA Nos. 6,8 & 10/KOL/2025, to which Ld. DR did not oppose. We ,therefore, dismiss these appeals as withdrawn.

3. These appeals of the assessee are dismissed as withdrawn.

ITA No. 7/KOL/2025

4. The only issue pressed at the time of hearing is that the reassessment proceedings-initiated u/s 147 of the Act being barred by limitation, in view of the decision of Hon’ble Supreme Court in case of PCIT Vs. Rajeev Bansal (2024) 469 ITR 46 (SC), which is raised by the assessee in ground nos. 2,3 and 4.

4.1. We have heard the rival submission and perused the materials available on record, we find merit in the contention of the assessee that the notice u/s 148 of the Income-tax Act, 1961 (the Act) as well as the consequent assessment framed by the ld. AO in this case are barred by limitation. We have examined the show cause notice issued u/s 148A(b) of the Act dated 30.06.2021, by the ld. AO. Therefore, there is no surviving time left for issuance of notice under TOLA and assessment was framed vide order dated 26.05.2023, which are barred by limitation in view of the decision of Hon’ble Supreme Court in case of Rajeev Bansal (supra). Consequently, the notice as well as the assessment framed are quashed.

4.2. The appeal of the assessee is allowed.

ITA No. 9/KOL/2025

5. The only issue pressed at the time of hearing by the Counsel of the assessee is contained in ground no.6, which is extracted below:-

“Without prejudice to ground no.5 above, Ld. CIT (A) was wholly unjustified in dismissing the validity of the notice u/s 151(1) by the specified authority and in view of the facts and in the circumstances, it may be held accordingly.”

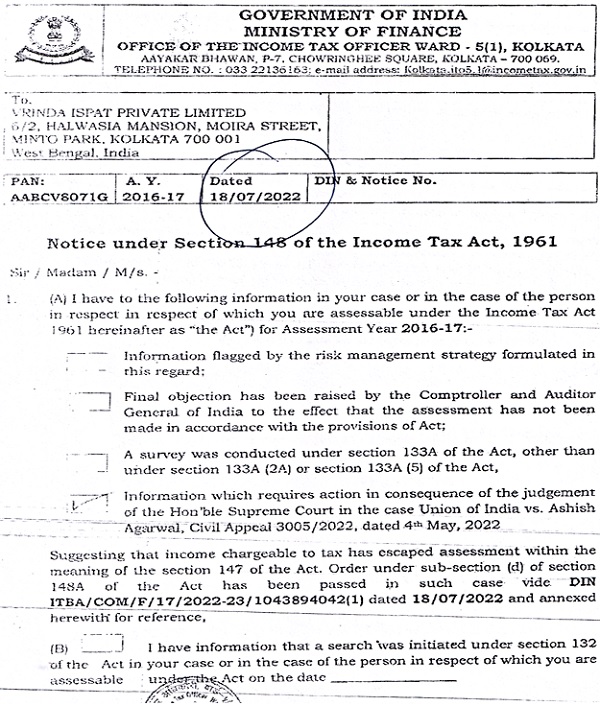

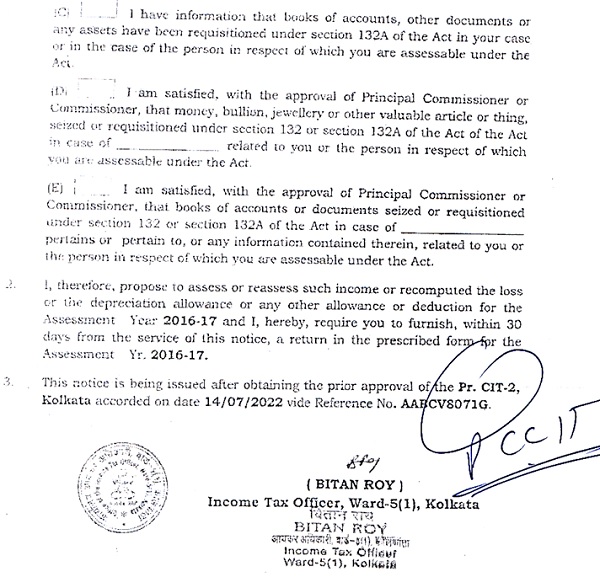

5.1. After hearing the rival contentions and perusing the materials available on record, we find that the assessee has raised a legal issue challenging the validity of approval granted by the ld. PCIT-2, Kolkata on 14.07.2022, for issuance of notice u/s 148 of the Act. For the sake of ready reference, the said approval granted is extracted below:-

–

5.1.1. Since, the year involved is A.Y. 2016-17, and the reopening is made after a period of three years then the approval has to be granted by the Principal Chief Commissioner of Income Tax and not Principal Commissioner of Income Tax. Therefore, the approval granted is invalid and hereby quashed. Consequently the notice issued u/s 148 of the Act as well as the assessment framed vide order dated 25.05.2023, are also invalid and are hereby quashed.

5.2. The appeal of the assessee is allowed.

6. In the result, the appeals of the assessee are partly allowed.

Order pronounced on 25.06.2026.

Author Bio