The hardest thing in the world to understand is the income tax. [Albert Einstein]

This article aims at highlighting the importance of ‘reasons to believe’ phrase on invocation of provisions of section 148/147 Income Tax Act, 1961.

Background- To understand the phrase ‘reasons to believe’ it is fair to discuss provisions of section 147 of Income Tax Act, 1961. For ready reference relevant extracts of provisions of section 147 of the Income Tax Act, 1961 is reproduced below:

“147. Income escaping assessment.

If the [Assessing] Officer,[has reason to believe] that any income chargeable to tax has escaped assessment for any assessment year, he may, subject to the provisions of sections 148 to 153, assess or reassess such income and also any other income chargeable to tax which has escaped assessment and which comes to his notice subsequently in the course of the proceedings under this section, or recompute the loss or the depreciation allowance or any other allowance, as the case may be, for the assessment year concerned (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year) :

Provided that where an assessment under sub-section (3) of section 143 or this section has been made for the relevant assessment year, no action shall be taken under this section after the expiry of four years from the end of the relevant assessment year, unless any income chargeable to tax has escaped assessment for such assessment year by reason of the failure on the part of the assessee to make a return under section 139 or in response to a notice issued under sub-section (1) of section 142 or section 148 or to disclose fully and truly all material facts necessary for his assessment for that assessment year.

From the above cited provision, it is manifested that the assessing officer must have reasons to believe to satisfy the criteria of section 147 of the Income Tax Act, 1961 to issue notice under section 148 of the Income Tax Act, 1961.

Meaning of “reasons to believe”:

Phrase “reasons to believe” is not explained in the Income Tax Act, 1961. “reasons” refer to the cause like a document, statement, third party, confirmation etc. and “belief” refers to conclusion. Some examples of reasons to believe:

a. Fresh evidence coming to the possession of authorities which indicate that the assessee has understated income or claimed excessive or wrong deductions, expenses, allowances etc. like third party statements, findings in other cases etc.

b. Later decision of supreme court/ High court against the assessee.

c. Retrospective amendment in law.

For the same many litigators have knocked the doors of tribunal and court to understand the essential ingredient of section 147 of the Income Tax Act, 1961 and also challenged the validity of notice issued under section 148 of the Income Tax Act, 1961. Some of the examples enumerated below:

a. Mere gossip, rumour or suspicion can amount to ‘reasons to suspect’ but they are not sufficient to form a ‘reason to believe’.

b. Report of departmental valuation officer. It is merely an estimation. It can not be said to be “Reasons to belief”. [ACIT vs Dhariya Construction (2011) (SC)]

c. Assessee filed return , which was processed u/s 143(1). Later on, a survey u/s 133A was conducted. Based on the survey report, AO initiated reassessment proceedings u/s 147.

Held, neither the survey report nor any other material material indicated that any income chargeable to tax had escaped assessment, reopening was invalid. [Hemant Traders vs ITO(2015) (Bom)].

d. Reopening cannot be done on a mere change of opinion of the A.O. [ CIT vs Kelvinator of India (2010) (SC)].

e. In the case of ACIT vs Rajesh Jhaveri and others (2006)(SC) It was held that for change of opinion formed earlier in assessment. Initiation u/s 143(1)(a) is not an assessment and hence, no opinion was formed. Hence, if initiation u/s 143(1)(a) is issued and thereafter notice u/s 148 is issued, assessee cannot argue that there is change of opinion.

f. Reopening based on the audit objection of the Income Tax department’s audit party (whether on facts or on law) is generally not a reason to believe. [CIT Vs. Lukas TVS Ltd., [2001] 249 ITR 306 (SC)]

g. Reasons to believe shall only be of AO. AO cannot borrow the opinion of any other person. Like if the superior authority of AO asks to reopen an assessment, the same is not valid. It is only AO who has to form an opinion. In the case of PCIT-6 vs Meenakshi Overseas (P.) Ltd Honorable Delhi High court heldsince there was no independent application of mind by Assessing Officer to tangible material and, conclusions of Assessing Officer were reproduction of conclusion in investigation report, reasons failed to demonstrate link between tangible material and formation of reason to believe that income had escaped assessment and, consequently, reassessment was unjustified.(2017) 395 ITR 677)

h. Reasons to believe shall be a prima-facie opinion of AO that income escaped assessment. It is not required to be a conclusive opinion that income escaped assessment.

i. The reasons to believe must have rational connection with or relevant bearing on the formation of belief i.e. there must be a live link between material coming the notice of the Assessing Officer and the formation of belief regarding escapement of income. If the aforesaid requirement are not met, the Assessee is entitled to challenge the very act of re-opening of Assessment and assuming jurisdiction on the part of the Assessing Officer.[ITO v. Lakhmani Merwal Das [1976] 103 ITR 437]

j. Reasons to believe must be concrete not a mechanical one. Hon’ble Delhi High Court in the case of Pr. CIT vs., SNG Developers Ltd., [2018] 404 ITR 312 (Del.) in which it was held that “Held, dismissing the appeal, that the reasons recorded by the Assessing Officer for reopening the assessment under section 147, issuing a notice under section 148 did not meet the statutory conditions. As already held by the Appellate Tribunal, there was a repetition of at least five accommodation entries and the total amount constituting the so-called accommodation entries would therefore not work out to Rs.95,65,510. It was unacceptable that the Assessing Officer persisted with his “belief” that the amount had escaped assessment not only at the stage of rejecting the assessee’s objections but also in the reassessment proceedings, where he proceeded to add the entire amount to the income of the assessee. Therefore there was non-application of mind on the part of the Assessing Officer. The Appellate Tribunal was justified in confirming the order of the Commissioner (Appeals) and holding that the reopening of the assessment was bad in law.”

From the above discussion, we can conclude that before believing on “reasons to believe” provided by the Assessing Officer, we must examine the facts of the case on an isolated basis and based on that challenge the beliefs formed by the Assessing Officer.

Few noticeable points on “reasons to believe”:

a. Reasons must be dated. Date specified in reasons to believe must be before the date of issue of notice under section 148 of the Income Tax Act.

b. Approval of appropriate authorities must be obtained on reasons to believe.

c. Reasons must be recorded in writing.

d. It must be written that “I have reasons to believe” It cannot be replaced by any other phrase.

e. Reasons must be of a jurisdictional Assessing officer.

f. It must be based on evidence.

There can be many other different ways to challenge the validity of reasons to believe by staying within the boundaries of law.

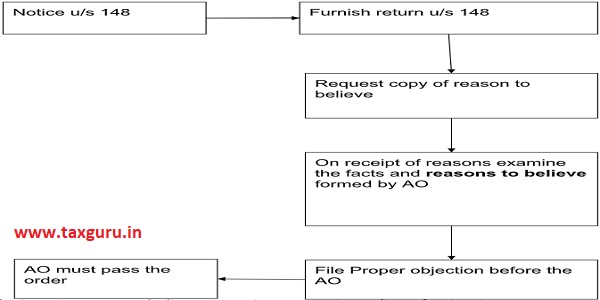

Procedure for obtaining the reason to believe:

Income Tax Act does not specify the procedure for obtaining the reasons to believe. However, Apex court of India laid down the procedures in GKN Driveshafts (India) Ltd. v. Income-tax Officer (2002) 125 TAXMAN 963 held that “we clarify that when a notice under section 148 of the Income Tax Act is issued, the proper course of action for the noticee is to file return and if he so desires, to seek reasons for issuing notices. The Assessing Officer is bound to furnish reasons within a reasonable time. On receipt of reasons, the noticee is entitled to file objections to issuance of notice and the Assessing Officer is bound to dispose of the same by passing a speaking order. In the instant case, as the reasons have been disclosed in these proceedings, the Assessing Officer has to dispose of the objections, if filed, by passing a speaking order, before proceeding with the assessment in respect of the above said five assessment years”.

Above judgement gives the AO a precise direction that he must provide a copy of “reasons to believe” within reasonable time and on receipt of reasons, noticee can file the objections for reopening and AO must pass a speaking order before proceedings. If AO has not provided the copy of reasons to believe, noticee can challenge the Validity of notice u/s 148 of the Income Tax Act, 1961. However, The reasons recorded under section 132 of the Income Tax Act, 1961 shall not be disclosed as any person or any authority or the Appellate Tribunal (Search and Seizure). The reasons recorded in case of search can be obtained by filing Writ before Honorable High Court.

Conclusion: Reasons to believe is an important ingredient for issuing notice under section 148 and invocation of section 147 of Income tax Act, 1961. Challenging the reasons to believe can be based on both facts/law and procedural lapses also. We may conclude that before believing on reasons to believe we must examine the facts of the case and “reasons to believe” formed by AO to give proper direction to the case of appellant.

Disclaimer: The views expressed herein above are solely the author’s personal views/opinion. This is an informational article and should not be considered as a legal opinion. The possibility of any errors and omissions in the article cannot be ruled out.

Author Bio