How to pay your taxes

Pay Direct taxes to the Government through the following two options

1. Online at NSDL e-Gov portal – mandatory for following categories

a. Corporate assesses.

b. All assesses (other than company) to whom provisions of section 44AB of the Income Tax Act, 1961 are applicable.

2. Offline – payment in physical mode at designated bank branches.

E-Tax payment online

1. Visit website http://www.tin.nsdl.com (Services/ e-payment : Pay Taxes Online)

1. The option of is also available at home page of TIN website

Select the relevant tax challan for payment

Provided details of the taxpayer and taxes being paid in the electronic challan

Tax payer is required to enter the relevant / mandatory detail as per the challan selected, such as

1. Accounting Head codes (major and minor)

2. Nature of payment

3. Select the payment option – through net-banking or debit card of select banks

4. Enter PAN/TAN

5. Assessment year

6. Address and other contact

Verify and confirm the details entered

Verify and confirm the details entered

On submission of data as per the selected challan form, Tax payer will be redirected to confirmation screen. The full name of taxpayer as per PAN/TAN master will be displayed on the confirmation screen. The name will be partially masked for information security reasons

Submit the details

On clicking the option “Submit to the Bank”, the taxpayer will be directed to the bank as per the payment option selected i.e. net-banking or Debit card.

Login to the net-banking portal of selected bank

The taxpayer has to login to the net-banking site by providing the login credentials.In

Enter the amount of tax to be paid under the various tax heads

Verify the amounts entered and confirm

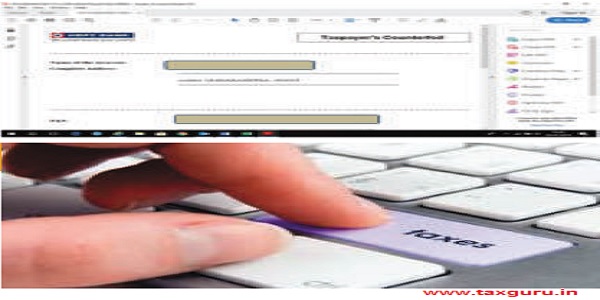

Download the tax counterfoil

On successful payment a taxpayer’s counterfoil will be generated and displayed.

Challan Identification Number (CIN) on the counterfoil is a proof of payment being made

Do’s

1. Mandatory details required to be filled in challan

{a} PAN/TAN

{b} Name and Address (In case of a physical challan)

{c} Assessment Year

{d} Major Head, Minor Head

{e} Type of payment

2. Use challan type 281 for deposit of TDS/TCS payments.

{a} Quote the correct TAN, name & address of the deductor on each challan

{b} Verify your TAN details from Income Tax Department web-site (www.incometaxindia.gov.in) prior to depositing TDS/TCS.

{c} Use seperate challan to deposit tax deducted under each section and indicate the correct nature of payment code in the relevant column in the challan.

{d} Use seperate challans to deposit tax deducted for different types of deductees.

3. For Non TDS/TCS payments use challan types 280/282283/285/286/287 as applicable.

{a} Quote the correct PAN, name and adderss on each challan used for depositing the tax.

4. Mention/verify the correct Financial Year and Assessment Year in the challan before tax payment.

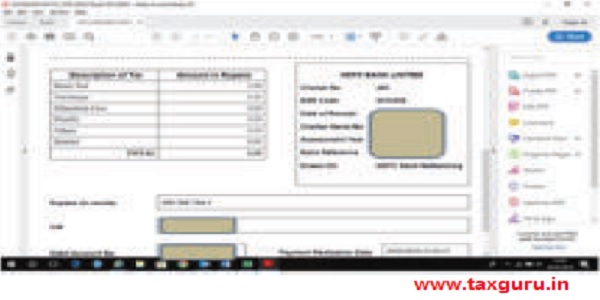

5. Payment confirmation: Ensure that the Challan Identification Number (CIN) has been provided on the counterfoil issued after successful payment of tax. Challan Identification Number (CIN) comprises of the following

{a} Seven digit BSR code of the bank branch where tax is deposited

{b} Date of Deposit (DD/MM/YY) of tax

{c} Serial Number of Challan

6. Verify the tax payment information submitted to the bank.

{a} Details available on the TIN website www.tin-nsdl.com under the link “Challan Status Inquiry”

{b} In case the details are not available then you may contact the bank branch where the tax has been deposited.

7. In case the counterfoil issued by the bank has been misplaced, kindly contact the respective bank/branch for details regarding the same

Don’ts

1. Do not use incorrect type of challan for payment of taxes.

2. Do not make mistake in quoting PAN/TAN.

3. Do not give PAN in place of TAN or vice versa.

4. Do not use a single challan to deposit tax deducted for corporate and non-corporate deductees.

5. Do not use same challan for depositing various types of tax like advance tax, self-assessment tax etc.

6. Do not make mistake in the F.Y.and A.Y. to be indicated in the challan.

7. If you have multiple TANs for the same division filling TDS statements, do not use different TANs in different challans. Use one TAN consistently and surrender the others