Summary: Home loan interest can be a financial challenge, but with careful planning, it can become a tax-saving tool. For self-occupied properties, under Section 24(b), taxpayers can claim a maximum deduction of ₹2 lakh per annum on home loan interest, and any unclaimed interest is added to the Cost of Acquisition (COA) to reduce future capital gains tax. For rented-out properties, there is no cap on interest deductions, allowing the entire interest to be deducted from rental income. Losses, up to ₹4.5 lakh annually, can be carried forward for up to 8 years to offset future rental income. For example, on a ₹2 crore property with a ₹1.2 crore loan and ₹10 lakh annual interest, self-occupied owners can claim ₹2 lakh and add ₹8 lakh to their COA, while landlords can reduce their taxable rental income by the full ₹10 lakh. Over time, these strategies reduce tax liabilities, increase wealth through capital gains tax reduction, and provide a cushion for future rental income taxes. By understanding and utilizing these provisions, taxpayers can significantly improve their tax outcomes and financial stability.

Introduction

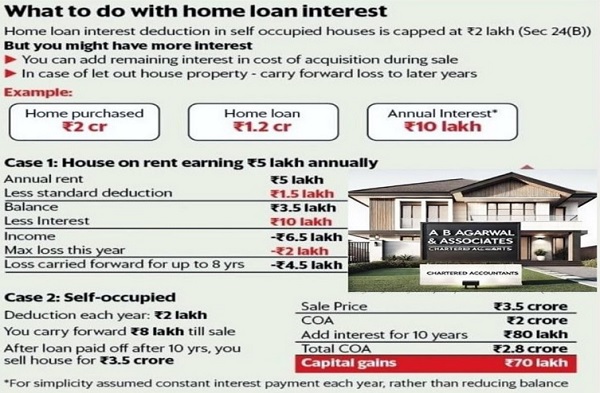

Buying a home is a dream for many, but the associated home loan interest can be a financial burden. However, with strategic planning, you can turn this burden into a tax-saving opportunity. Below is a detailed, tabular breakdown of how to maximize tax benefits on home loan interest, whether your property is self-occupied or rented out.

Tax Benefits on Home Loan Interest: A Comparative Analysis

| Aspect | Self-Occupied Property | Rented-Out Property |

| Section Applicable | Section 24(b) | Section 24(b) |

| Maximum Deduction | ₹2 lakh per annum (on interest) | No upper limit (entire interest can be deducted from rental income) |

| Example Scenario | – Home Purchase Price: ₹2 crore

– Home Loan: ₹1.2 crore – Annual Interest: ₹10 lakh |

– Annual Rent: ₹5 lakh

– Standard Deduction: ₹1.5 lakh – Annual Interest: ₹10 lakh |

| Tax Calculation | – Deduction Claimed: ₹2 lakh

– Remaining Interest: ₹8 lakh (add to COA) |

– Net Rent After Deduction: ₹3.5 lakh

– Interest Deduction: ₹10 lakh – Loss: ₹6.5 lakh |

| Carry Forward Benefit | – Unclaimed Interest: ₹8 lakh/year

– Added to COA over 10 years: ₹80 lakh |

– Loss Carried Forward: ₹4.5 lakh (for up to 8 yrs) |

| Long-Term Strategy | – Total COA after 10 years: ₹2.8 crore

– Sale Price: ₹3.5 crore – Capital Gains: ₹70 lakh |

– Set off ₹4.5 lakh loss against future rental income |

| Key Takeaway | Add unclaimed interest to COA to reduce capital gains tax. | Carry forward losses to offset future rental income. |

The Wow Factor: Turning Unclaimed Interest into a Tax Advantage

| Strategy | Self-Occupied Property | Rented-Out Property |

| Tax Benefit | – Reduces capital gains tax by increasing COA.

– Long-term wealth creation. |

– Reduces taxable rental income.

– Provides a cushion against future tax liabilities. |

| Example | – COA increases by ₹80 lakh over 10 years.

– Capital gains tax reduces significantly. |

– ₹4.5 lakh loss carried forward for 8 years.

– Future rental income is tax-free up to this amount. |

Conclusion

| Key Message | Self-Occupied Property | Rented-Out Property |

| Final Takeaway | Add unclaimed interest to COA to reduce capital gains tax. | Carry forward losses to offset future rental income. |

*****

For a deeper insight you may reach out to me at cacs.abhishekagarwal@gmail.com, also you can follow me on linkedin.com/in/abhishek-agarwal-b51358164

Disclaimer: The above content has been prepared for general information purposes only. This is not intended to constitute a recommendation, offer or advice. It does not constitute a solicitation to any class of persons. I do not warrant that the content is accurate or complete and disclaim any and all liability to anyone for any loss or damage caused by errors or omissions.

Author Bio

Very clear article with the example

Which means rented the loss can be set off every year and carried forward

Thanks Sir