Page Contents

- ♦ Notified ITR Forms for the AY 2018-19 AND applicability

- ♦ % of ITR Wise receipt of e-Return in FY 2017-18

- ♦ ITR to filed Online except in certain cases:

- ♦ More details of salary and house property income

- ♦ Penalty for not Filing of ITR on or before due date

- ♦ Capital Gains in case of transfer of unquoted shares

- ♦ Revised Depreciation Schedule

- ♦ Details of business transactions with registered and unregistered suppliers under GST

- ♦ Other Disclosure w.r.t. GST

- ♦ Other Disclosure w.r.t. GST …. cont.

- ♦ Foreign Bank Details in case of Refund to NRI

- ♦ Disallowance of expenses in case of TDS default

- ♦ Transfer of TDS Credit to Other Person

- ♦ Breakup of Payments / Receipts in Foreign Currency

- ♦ Breakup of Payments / Receipts in Foreign Currency

- ♦ Misc. Changes

- Conclusion

♦ Notified ITR Forms for the AY 2018-19 AND applicability

ITR – 1 (Sahaj) Individuals being a resident other than not ordinarily resident having Income from Salaries, one house property, other sources (Interest etc.) and having total income upto Rs.50 Lakh

ITR – 2 Individuals and HUFs not having income from profits and gains of business or profession

ITR – 3 Individuals and HUFs having income from profits and gains of business or profession

ITR – 4 Presumptive Income From Business & Profession

ITR – 5 persons other than,- (i) individual, (ii) HUF, (iii) company and (iv) person filing Form ITR-7

ITR – 6 Companies other than companies claiming exemption under section 11

ITR – 7 persons including companies required to furnish return under sections 139(4A) or 139(4B) or 139(4C) or 139(4D) or 139(4E) or 139(4F)

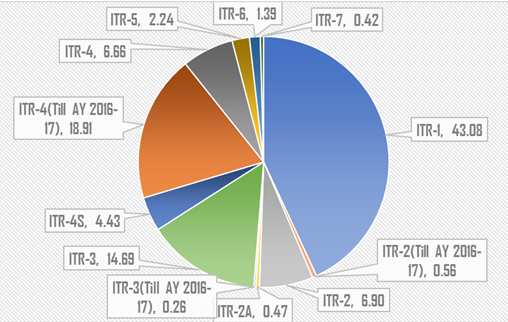

♦ % of ITR Wise receipt of e-Return in FY 2017-18

(source – https://www.incometaxindiaefiling.gov.in/moreStatistics)

Total 6,74,74,904 e-returns filed during the FY 2017-18

♦ ITR to filed Online except in certain cases:

- All the tax returns have to filed online as was the case last year. However, there are certain exceptions where the ITR can be filed in paper/physical form.

- If the individual is of age 80 years or more and

- the tax return is furnished using in ITR Form-1 (Sahaj) or

- ITR-4 (Sugam)

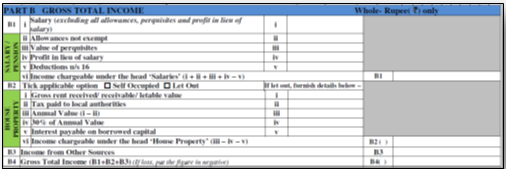

♦ More details of salary and house property income

- [Applicable for ITR 1 to 4]

- Earlier only Taxable amount was reported – New ITR forms require the individual assessee to provide detailed calculation in case of salary & house property income.

♦ Penalty for not Filing of ITR on or before due date

- [applicable for all ITR Forms]

- Penalty for not Filing of ITR on or before due date – as amend by the Finance Act, 2017

- [applicable for ITR 2, 3, 5, 6 and 7]s

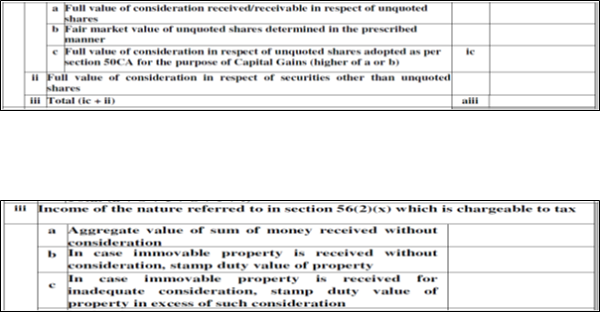

- Capital Gains in case of transfer of unquoted shares – for providing consequential reporting as per amended new Section 50CA inserted by Finance Act, 2017 new column inserted.

- Reporting of sum taxable as Gift – new clause 56(2)(x) as Inserted by Finance Act 2017 is applicable to all assessees –

- Same changes have been also made in ITR Form 3, 5, 6 & 7

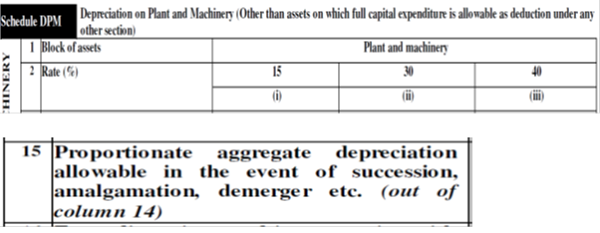

♦ Revised Depreciation Schedule

- [applicable for ITR Form 3, 5 & 6]

- Revised Depreciation Schedule – CBDT vide Income-Tax (Twenty Ninth Amendment) Rules, 2016, dated 07-11-2016 had restricted the highest rate of depreciation for any block of asset to 40%. i.e. all block of assets which were eligible for depreciation at the rate of 50%, 60%, 80% or 100% would be eligible for depreciation at the rate of 40%

- New Column also inserted to report the claim of proportionate depreciation in the event of business reorganisation, i.e., demerger, amalgamation, etc.

- Same changes have been also made in ITR 5 & 6

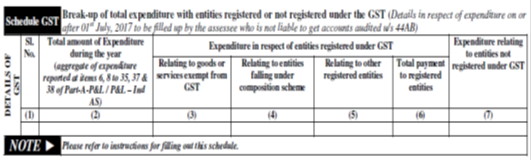

♦ Details of business transactions with registered and unregistered suppliers under GST

- [applicable for ITR Form 6]

- Detailed analysis asked with respect to Details of business transactions with registered and unregistered suppliers under GST

♦ Other Disclosure w.r.t. GST

- [applicable for ITR Form 3, 5 & 6]

- Under Schedule PL have been modified to include GST related details;

- Income: GST Received or receivable in respect of Goods Sold or supplied (Part A P&L, Point 1C)

- Expenses: GST paid or payable in respect of Goods and service purchased (Part A P&L, Point 7)

- Expenses: GST paid or payable to Government (excluding taxes on income) (Part A P&L, Point 36)

- Refund of GST not credited to Profit and loss account (PART A-OI, 5)

- Amount of credit outstanding in account in respect of GST (Part A-OI, 12)

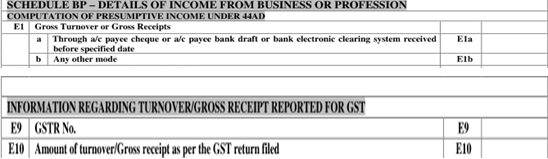

- [applicable for ITR Form 4]

- Now, there is an additional requirement to quote GSTR No. and turnover/gross receipts as per GST return filed. Under Schedule BP vide point E9 and E10, GST No in respect of details of business and profession computed under presumptive basis u/s 44 AD (or) 44AE (or) 44ADA – if applicable..

- Amount of Turnover/Gross Receipt as per the GST return filed if applicable..

- Note: ‘Aggregate turnover has been defined in GST law as the aggregate value of all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis), exempt supplies, exports of goods or services or both and inter-State supplies of persons having the same Permanent Account Number to be computed on all India basis but excludes central tax, State tax, Union territory tax, integrated tax and cess.

- Turnover includes Taxable, exempted, Zero rated, Nil Rated and Non GST supplies.

- The Turnover as mentioned above should match with Gross Receipt to be shown in Schedule BP point no E1.

♦ Other Disclosure w.r.t. GST …. cont.

- [applicable for ITR Form 4]

- Relevant Extracts;

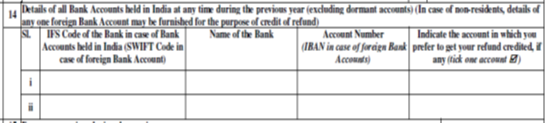

♦ Foreign Bank Details in case of Refund to NRI

- [applicable for ITR Form 2 to 7]

- In case of refund claimed by the NR, then same can be get credited in the Foreign Bank Account by providing details of same

♦ Disallowance of expenses in case of TDS default

- [applicable for ITR Form 2, 3, 5, 6 &7]

- Section 40(a)(ia) disallow 30% of certain expenditures if tax is not deducted in respect of those expenditures in accordance with Chapter XVII-B or if tax is deducted but not deposited on or before the due date for filing of return of income.

- new column has been inserted in the ITR Forms to report such disallowances

♦ Transfer of TDS Credit to Other Person

- [applicable for ITR Form 2 to 7]

- Where an income, which is added to the common pool, has been subjected to TDS, the assessees face difficulties in proving their claim for TDS Credit.

- There are other similar situations, where a person is entitled to claim the credit for tax deducted in the name of another person, i.e., inheritance, Partners TDS deducted in Firm’s PAN and vice versa., Deposits held in Joint Name and TDS deducted only in First Name, etc.

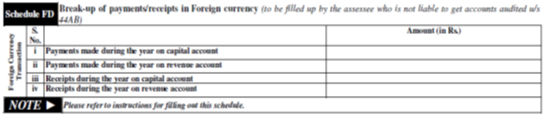

♦ Breakup of Payments / Receipts in Foreign Currency

- [applicable for ITR Form 6]

- Assessees are required to provide the details of payment made and sum received in foreign currency towards capital and revenue account.

- This schedule is applicable only to assessee who is not liable to Audit u/s 44AB

♦ Breakup of Payments / Receipts in Foreign Currency

- [applicable for ITR Form 4]

- Earlier only 4 financial particulars of the business (1) total creditors, (2) total debtors, (3) total stock-in-trade and (4) cash balance were reported

- Now whole balance sheet in condensed form also required to be furnished

♦ Misc. Changes

- Partners cannot use ITR 2 – for the Assessment Year 2018-19, an individual or an HUF, who is a partner in a firm, shall be required to file his ITR in Form ITR 3 only

- Reporting of sum taxable as Gift – Finance Act, 2017 had extended the scope of this provisions of Section 56(2)(vii) by introducing a new clause, i.e., Section 56(2)(x) which covers all taxpayers within its ambit. Consequently, new columns have been inserted in all ITR forms except ITR 1 and ITR 4 under ‘Schedule OS’ to report any income as specified in Section 56(2)(x).

- Assessee claiming DTAA relief is required to report more details – new ITR Forms seeks additional details for current year vis, Rate as per treaty, rate as per IT Act, Section of IT Act and Applicable Rate

- Capital gains exemption to be furnished in detail – exemption under Sections 54, 54B, 54EC, 54EE, 54F, 54GB and 115F shall be reported in details and separately.

- Taxability on remission of trading liability in case of ‘Income from other source’ – new ITR forms require separate reporting of such remission or cessation, which is taxable as per Section 59, in Schedule OS

- Details of GST paid and refunded – new ITR forms have introduced new columns to report CGST, SGST, IGST and UTGST paid by, or refunded to, assessee

- Removal of ‘Gender’ from personal information in the ITR 2, 3 and 4

- Declaration required by Political Parties to confirm if cash donations are received [Section 13A] – new ITR 7 requires the political parties to provide a declaration by selecting the ‘Yes’ or ‘No’ check-box to confirm whether it has received any cash donation in excess of Rs. 2,000

- Reporting of CSR appropriations – new column has been inserted in ITR Form 6 to provide details of apportionments made by the companies from the net profit for the CSR activities

- Details of fresh registration upon change of objects [Section 12A] – A trust will be required to furnish the following details if there is any change in its stated objects:

- Date of change in objects

- Whether application for fresh registration has been made within stipulated time period?

- Whether fresh registration has been granted?

- Date of such fresh registration.

Conclusion

There are also other numerous reporting requirements are made mandatory in ITR Forms for the AY 2018-19. The Departments now seeks more and more information from the Assessees because the department is now moving towards E-Assessment. Further, in view of implementation of GST, also new reporting requirement are sought, Therefore, the applicable reporting and discloser requirement may vary from case to case depending upon circumstances.

Disclaimer: This document is intended for private circulation and knowledge sharing purpose only. All efforts have been made to ensure the accuracy of information in this publication. The information contained in this document is published for the knowledge of the recipient but is not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient. The publication is a service to our clients to provide an overview of the Direct Tax Proposals and shall not be construed as professional advice or an authoritative opinion. Whilst due care has been taken in the preparation of this publication and information contained herein, we will not be responsible for any errors that may have crept in inadvertently and do not accept any liability whatsoever, for any direct or consequential loss howsoever arising from any use of this publication or its contents or otherwise arising in connection herewith.

Surana Maloo & Co. | Chartered Accountants

2nd Floor, Aakashganga Complex Parimal Under Bridge, Paldi, Ahmedabad – 380007

vidhansurana@suranamaloo.com, sunilmaloo@suranamaloo.com

CONGRATS. KEEP IT UP. INCOME TAX ACT IS VERY CLUMSY AND EVERY SECTION OF THE ACT BEGINS WITH :PROVIDED THAT” WHEREAS”. U R DETAILED EXPLANATION IS VERY MUCH LAUDABLE. THANKS…PREM SAGAR KUNDE

YOUR PORTAL IS MAKING HUGE CONTRIBUTION FOR CREATING DEPENDABLE AWARENESS OF TEDIOUS SUBJECT OF TAX-CORPORATE LAWS AND ALSO GIVING OPPORTUNITY TO WIDE SPECTRUM OF CONTRIBUTION OF KNOWLEDGE

WISHING GRAND SUCCESS OF YOUR PORTAL. HOPING IT WILL CREATE RECORDS AND BIG HIT.

ITR-1 applicable for income from pension.

Dear Sir / Madam,

Kindly provide me the selling to customer rates for silver and gold for the period from 16/07/2015 to 31/07/2015.

Also, please let me know the making charges, if any for silver coins and gold ornaments. How much or what percentage of the silver coins or gold jewelry, it could be?

Your early response in the above mater would be highly appreciated.

Thanking You,

Yours Sincerely,

Rajen Chowdhury,

Contact # 9432389280.