The document provides a comprehensive comparison between the Income-tax Act, 1961 and the proposed Income-tax Act, 2025, highlighting structural reorganisation rather than substantive overhaul. It maps old sections to new provisions across major heads of income such as salary, house property, business income, capital gains, and other sources, showing renumbering and consolidation of provisions. Key changes include shifting exemptions to schedules, redefining deduction frameworks, and reorganising compliance provisions like audit, TDS, and reporting. The new regime emphasizes simplification through grouped sections, clearer definitions, and integrated schedules. It also introduces revised tax slabs under the default tax regime, streamlined audit forms (Form 26 replacing multiple forms), and unified compliance formats. Importantly, while section numbers and structure change significantly, the underlying principles of taxation largely remain intact. The document serves as a practical mapping guide for professionals to understand transitions, compliance requirements, and interpretation under the new law.

Income Tax Comparison Table

A Bird Eye View

| Head of Income | Old Act (1961) – Series | New Act (2025) – Series |

| Income from Salary | Section 15–17

*Please see the comparison table for Section 10 series i.e. deductions available under the salary head |

Section 15–19 (Exemptions in Schedule III) |

| Income from House Property | Section 22–27 | Section 20–25 |

| Profits & Gains from Business or Profession | Section 28–44 | Section 26–66 |

| Capital Gains | Section 45–55A | Section 67–91 |

| Income from Other Sources | Section 56–59 | Section 92–95 |

| Set-off & Carry Forward of Losses | Section 70 – 80 | Section 108 – 121 |

| Deductions from GTI (Chapter VI-A) | Section 80A–80U | Section 123–150 (Read with Schedule XV) |

| Audit & Presumptive Taxation | Section 44AB–44AE | Section 58–63 |

| Advance Tax | Section 208 | Section 404 |

| Others | Section 115BAC | Section 202(See chart on next page) |

| Section 115BA | Section 199, read with 205*1 | |

| Section 115BAA | Section 200, read with 205*1 | |

| Section 115BAB | Section 201, read with 205*1 | |

| Section 115BAD | Section 203, read with 205*1 | |

| Section 87A (Rebate) | Section 156 (Rebate) | |

| *1 Section 205 of IT ACT, 2025 Conditions for tax on income of certain companies and co-operative societies. | ||

–

| INCOME UNDER THE HEAD SALARIES | |

| Old Sections (1961 Act) | New Section (2025 Act) |

| Section 15 Charging section | Section 15 Charging Section |

| Section 16 Deductions from salary | Section 19 Deductions from salary |

| Section17 (2) Perquisites | Section16 -Income from Salary

Section17-Perquisite Section 18-Profits in lieu of salary |

| Section17 (3) Profits in lieu of salary | |

| Section10 (5) Leave Travel Concession (LTC/LTA) | Schedule III (8) – The value of any travel concession or assistance |

| Section10(10) Gratuity | Section19- Deductions from salaries

Schedule III (38) – Gratuity on death of employee |

| Section10(10A) Commuted Pension | Section 19 specify deduction allowable table

See entry no 8 in that table |

| Section10 (10AA) Leave Encashment | Section 19 specify deduction allowable table

See entry no 13 and 14 in that table |

| Section10 (10B) Retrenchment Compensation | Section 19 Deduction from salaries

(1) SL No. 10 describes nature and computation of deduction (2) (c) deemed retrenchment compensation |

| Section 10(10C) Voluntary Retirement Compensation (VRS) | Section 19 Deduction from salaries

(1) SL No. 12 describes nature and computation of deduction (2) (h)employees eligible for claiming for such deduction |

| Section 10(11) Statutory Provident Fund | Schedule II (3) – Any payment from a provident fund to which the Provident Funds Act, 1925 (19 of 1925) applies, or from any other provident fund set up by the Central Government and notified by it in this behalf Read with section 11 |

| Section10(12) Recognized Provident Fund | Schedule II (4) – The accumulated balance due and becoming payable to an employee participating in a recognized provident fund to the extent provided in paragraph 8 of Part A of the Schedule XI Read with section 11 |

| Section 10(13A) House Rent Allowance (HRA) | Schedule III (Table: Sl.No 11) See note 1- to see the Rule No.145 of the Draft Income tax rule 2026 |

| Section10 (14) Special Allowances | Schedule III Table: Sl.No 12

– Any special allowance or benefit to the extent to which such expenses are actually incurred for that purpose |

| Section 89 Relief in case of arrears or advance salary | Section 157 Relief when salary, etc., is paid in arrears or in advance. |

| Section 192 TDS on salary | Section 392 read with section 402 for the purposes of interpretation of certain items in the above section |

Note1 for the purpose of Computation of HRA

Rule 279

Limits for the purposes of Schedule III (Table: Sl. No 11)

(1) The amount which is not to be included in the total income of an assessee in respect of the special allowance referred to in Schedule III (Table: Sl. No 11) shall be the least of the following—

(a) the actual amount of such allowance received by the assessee in respect of the relevant period; or

(b) the amount by which the expenditure actually incurred by the assessee in payment of rent in respect of residential accommodation occupied by him exceeds one-tenth of the amount of salary due to the assessee for the relevant period; or

(c) in case of an assessee employed in the location mentioned in column (B) in the table below, an amount equal to such percentage of salary, mentioned in column (C) thereof, due to the assessee in respect of the relevant period,—

| Sr. No. | Location of residential accommodation | Percentage of salary |

| A | B | C |

| i) | Mumbai, Kolkata, Delhi, Chennai, Hyderabad, Pune, Ahmedabad and Bengaluru. | 50% |

| ii) | Any other place | 40% |

(2) In this rule

(a) “salary” includes dearness allowance, if provided for under the terms of employment, but excludes all other allowances and perquisites.

(b) “relevant period” means the period during which the said accommodation was occupied by the assessee during the tax year.

| INCOME FROM HOUSE PROPERTY | |

| Section22 Chargeability | Section 22 Charging section of the head “Income from the House Property |

| Section23 Determination of Annual Value | Section 21 Determination of the Annual Value |

| Section24 Deductions (Standard deduction & interest) | Section 22 Deduction from income from the House property |

| Section25 Amounts not Deductible under the head House Property | Section 22 Deduction from income from the House property |

| Section25A Arrears / unrealised rent recovered | Section 23 Arrears of rent and unrealised rent received subsequently. |

| Section26 Property owned by Co-owners | Section 24 Property owned by co-owners |

| Section 27 “Owner of house property”, “annual charge”, etc., defined (concept of Deemed owner) | Section 21 Determination of annual value. Read with Section 25 which provides interpretation of of certain words in above section |

–

| INCOME FROM PROFIT AND GAINS FROM BUSINESS AND PROFESSION | |

| Section 28 Profit and Gains from Business and Profession | Section 26 Income under head “Profits and gains of business or profession”.

Read with Section 66 which give special definitions for this Part-D (i.e. For the purposes of Profit and Gains from Business and Profession) |

| Section 29 Income from profits and gains of business or profession, how computed. | Section 27 Manner of computation profits and gains under business and profession |

| Section 30 Rent, rates, taxes, repairs and insurance for buildings. | Section 28 Rent, rates, taxes, repairs and insurance. |

| Section 31 Repairs and insurance of machinery, plant and furniture. | Section 28 Rent, rates, taxes, repairs and insurance. |

| Section 32 Depreciation | Section 33

Read with special meaning prescribed under the section 66 of the income tax act 2025 |

| Section 36 Other Deductions Insurance of stock/business assets

Bonus/commission to employees Interest on business loans Employer’s contribution to PF / gratuity / superannuation Employee’s PF/ESI contribution (if deposited in time) Bad debts written off Provision for bad debts (banks etc.) Discount on zero-coupon bonds Family planning expenditure (company) Securities Transaction Tax (STT) Keyman insurance premium |

Section 29-Deductions related to employee welfare

Section 30-Deduction on certain premium Section 31 – Deduction for bad debt and provision for bad and doubtful debt Section 32-Other deductions Section 66 – Interpretation |

| Section 37 other deduction that are allowable (not described in section 30 to section 36) | Section 42 other deduction that are allowable (not being an expenditure of the nature specified in sections 28 to 33, 44 to 49, 51 and 52 and not being in the nature of capital expenditure or personal expenses) |

| Section 145 Method of Accounting | Section 276 Method of Accounting |

| Section 40 amounts NOT deductible while computing Profits & Gains of Business or Profession (PGBP). |

Section 60 Amounts not deductible in certain circumstances.

Read with section 66 which prescribe certain meaning for this section and PGBP |

| Section 43B Certain deductions to be only on actual payment.

1. Tax, duty, cess, fee 2. Employer’s PF/ESI/gratuity contribution 3. Bonus/commission to employees 4. Interest to banks / FI / NBFC 5. Leave encashment 6. Railway usage charges

|

Section 37 Certain deductions to be only on actual payment.

1. Tax, duty, cess, fee 2. Employer’s PF/ESI/gratuity contribution 3. Bonus/commission to employees 4. Interest to banks / FI / NBFC 5. Leave encashment 6. Railway usage charges Read with section 66 which prescribe certain meaning for this section and PGBP Also see corresponding definitions which is relevant for above section in the Section 2 of the Income Tax Act 2025 |

| Section 43

definitions for computing business income (PGBP). Key Clauses:

|

Section 39 – Computation of actual cost

Section 41 – Written down value of depreciable asset Section 66 – Interpretation Section 2-Definitions |

| Section 50 Special Provisions for Computing Capital Gains for Depreciable Assets | Section 74 Special Provisions for Computing Capital Gains for Depreciable Assets |

| Section 139 Return of Income | Section 263 Return of Income

Section 349 Return of Income for Registered Non-Profit Organization |

–

| INCOME UNDER THE HEAD CAPITAL GAINS | |

| OLD (INCOME TAX, ACT, 1961) | NEW (INCOME TAX, ACT 2025) |

| Section 45- Charging Section | Section 67 |

| Section 2(14)- Capital Asset Definition | Section 2(22) |

| Section 2(47)- Transfer Definition | Section2(109) |

| Section 48- Mode of Computation of Capital Gains | Section 72 Mode of Computation of Capital Gains |

| Section 50C – Special provision for full value of consideration in certain cases.

|

Section 78- Special provision for full value of consideration in certain cases.

|

| Section 50CA- Special provision for full value of consideration for transfer of share other than quoted share. | Section 79- Special provision for full value of consideration for transfer of share other than quoted share. |

| Section 50D- Fair market value deemed to be full value of consideration in certain cases. (when consideration is not ascertainable) | Section 80- Fair market value deemed to be full value of consideration in certain cases. (when consideration is not ascertainable) |

| Section 49- Cost with reference to certain modes of acquisition

(Gift, will, succession/ transfer of right to another partner/any other similar nature of transfer) |

Section 73- Cost with reference to certain modes of acquisition

(Gift, will, succession/ transfer of right to another partner/any other similar nature of transfer) |

| Section 50- Capital Gains for Depreciable Assets | Section 74- Capital Gains for Depreciable Assets |

| Section 50B- Capital Gains on Slump Sale | Section 77-Capital gains on slump sale |

| Section 51- Advance money forfeiture | Section 81 Advance money on forfeiture |

| Section 70 Set off of loss from one source against income from another source under the same head of income. | Section 108 Set off of losses under same head of income. |

| Section 71 Set off of loss from one head against income from another. | Section 109- Set off of losses under any other head of income. |

| Section 74- Carry Forward of Capital Loss | Section 111 Carry forward and set off of loss from Capital gains. |

| Section 54- Profit on sale of property used for residence. (Exemption for Residential House) | Section 82- Profit on sale of property used for residence. (Exemption for residential house) |

| Section 54F- Exemption – Sale of another asset | Section 86- Capital gains on transfer of certain capital assets not to be charged in case of investment in residential house. |

| Section 54H- Extension of time for acquiring new asset or depositing or investing amount of capital gain. | Section 89 Extension of time for acquiring new asset or depositing or investing amount of capital gains. |

| Section 54B- Capital gain on transfer of land used for agricultural purposes not to be charged in certain cases. | Section 83 Capital gains on transfer of land used for agricultural purposes not to be charged in certain cases. |

| Section 111A-Tax on short-term capital gains in certain cases. | Section 196 Tax on short-term capital gains in certain cases. |

| Section 112- Tax on long-term capital gains. | Section 197-Tax on Long term capital gains |

| Section 112A- Tax on long-term capital gains in certain cases | Section 198- Tax on long-term capital gains in certain cases |

–

| INCOME UNDER THE HEAD OTHER SOURCES | |

| Old Sections (1961 Act) | New Section (2025 Act) |

| a. 56(2)(i) – Dividends | 92(2) – Specific Incomes Covered

92(2)(a) – Dividend |

| a. 56(2)(x) – Gifts (money/property without consideration or inadequate consideration)

|

|

| b. 56(2)(xi) – Compensation on termination/modification of business contract | |

| Section 57 – Deductions allowed under the head Income from the other sources | Section 93 Deductions allowed under the head Income from the other sources |

| DEDUCTIONS AVAILABLE FROM GTI | |

| Old Sections (1961 Act) | New Section (2025 Act) |

| Section 80C Deduction in respect of life insurance premia, deferred annuity, contributions to provident fund, subscription to certain equity shares or debentures, etc. | 123 Deduction for life insurance premia, deferred annuity, contributions to provident fund, etc.

read with SCHEDULE XV of the income tax act 2025 |

| Section 80CCD(1B) Deduction in respect of contribution to pension scheme of Central Government. | Section 125 read with SCHEDULE XV of the income tax act 2025 |

| Section 80D Deduction in respect of health insurance premia. | Section 126 Deduction in respect of health insurance premia. |

| Section 80G Deduction in respect of donations to certain funds, charitable institutions, etc. | Section 133 Deduction in respect of donations to certain funds, charitable institutions, etc.

read with – Section 332 Registration of Non- Profit Organization – Section354 Application for approval for purpose of Section 133 |

| Section 80P deduction for co- operative societies | Section 149- deduction for co-operative societies

Section 150- Some meanings have been given for the purposes of interpretation of section 149 |

–

| AUDIT AND PRESUMPTIVE TAXATION | |

| Section 44AB Audit of accounts of certain persons carrying on business or profession. | Section 58-Special provision for computing profits and gains of business or profession on presumptive basis in case of certain residents

Read with Section 63-Tax audit |

| Section 44AD | Section 58-Special provision for computing profits and gains of business or profession on presumptive basis in case of certain residents

Read with Section 63-Tax audit |

–

| Section 44ADA | Section 58-Special provision for computing profits and gains of business or profession on presumptive basis in case of certain residents

Read with Section 63-Tax audit |

| Section 44AE | Section 58-Special provision for computing profits and gains of business or profession on presumptive basis in case of certain residents

Read with Section 63-Tax audit |

| Section 269T-Mode of repayment of certain loans or deposits. For clause 31(c) of Old TAR | Section 188-Mode of repayment of certain loans or deposits or specified advances. |

| Section 269SS- Requirement As To Mode Of Acceptance, Payment Orrepayment In Certain Cases To Counteract Evasion Of Tax. For Clause31(a) of Old TAR | Section 185-Mode of taking or accepting certain loans, deposits and specified sum. |

Income Tax – New Tax Regime (Section 202)

(PREVIOUSLY 115BAC OF INCOME TAX ACT,1961)

Quick Concept Table

| PARTICULARS | KEY POINTS |

| Applicable Persons | Individual, HUF, AOP (other than co-operative society), BOI, Artificial Juridical Person |

| Nature of Regime | Default tax regime unless taxpayer opts out |

| Main Concept | Lower tax rates but most deductions and exemptions are not allowed |

| Loss Set-off Rule | House property loss cannot be set-off against other income |

| Carry Forward Loss | Loss related to disallowed deductions treated as already adjusted |

| Business Income Rule | Option exercised before return due date; can withdraw only once |

| No Business Income | Taxpayer may choose regime every year while filing return |

Tax Slab Rates

| TOTAL INCOME | TAX RATE |

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Memory Trick: 4L Nil → every next 4L slab increases tax by 5% until 30%.

| MAPPING OLD V/S NEW TAX AUDIT REPORT | |

| Clause 9(a) – If firm/AOP/BOI, details of partners/members. | 11(a) |

| Clause 9(b) – Profit-sharing ratio of partners/members. | 11(b) |

| Clause 10(b) – Change in nature of business/profession. | 12(a) |

| 12(b) | |

| Clause 11(a) – Books prescribed | 13 |

| Clause 11(b) – Books maintained | 13&14 |

| Clause 11(c) – Address of books | 14(a) |

| Clause 12 – Presumptive income reported (if included in P&L) → 19 | 19 |

| Clause 13(a) – Method of accounting employed. | 15(a) |

| Clause 13(b) – Change in method of accounting. | 15(b) |

| Clause 13(e) – Disclosure required under ICDS. | 18 |

| Clause 14 – Method of valuation of closing stock and any change. | 16(a) |

| Clause 15 – Capital asset converted into stock-in-trade. | 22 |

| Clause 16(d) – Any other income chargeable but not credited. | 21 |

| Clause 18 – Depreciation allowable under Income-tax Act. | 36 |

| Clause 22 – MSME interest disallowance (Sec 23 MSMED Act) | 33 |

| Clause 30 – Primary adjustment in transfer pricing (Sec 92CE). | 40 |

| Clause 30A – Interest deduction limitation (Sec 94B – EBITDA based) | 41(a)/(b)/(c) |

| (Note: Split into current year, brought forward & carried forward limits) | |

| Clause 31(a) – Loans/deposits accepted violating Sec 269SS. | 45(a) |

| Clause 31(b) – Repayment violating Sec 269T. | 45(b) |

| Clause 31(c) – Transactions violating Sec 269ST. | 45(c) |

| or | |

| Clause 31 – Cash transaction violations (269SS/269T/269ST) | 45(a) to 45(d) |

| Clause 32(a) – Details of brought forward losses. | 37(a) |

| Clause 34(a) – Whether the assessee is required to deduct or collect tax as per the provisions of Chapter XVII-B or Chapter XVII-BB, if yes please furnish: | 50(a) |

| Clause 34(c) – Details of TCS/TDS Details furnished | 50(b) |

| Clause 34(b) – Interest payable under Section 201(1A). | 50(c) |

| Clause 35(a) – Quantitative details of goods manufactured/traded. | 53a/53b |

| Clause 37 – Cost audit applicability and report. | 12(c) |

#Note- New Form 26 is a restructured format; mapping is conceptual and not strictly one-to-one. Some clauses are merged, split, or reported through schedules.

–

| Proposed Old V/s New Forms ( By Draft Income Tax Rules,2026) | |||

| Category | Particulars | Old Forms | New Forms(Proposed) |

| Audit | Tax Audit | 3CA/3CB, 3CD, 3CE | 26 |

| Audit | Transfer Pricing Audit | 3CEB | 48 |

| Audit | MAT Audit | 29B | 66 |

| Audit | Trust / NGO Audit | 10B, 10BB | 112 |

| Filing | TDS Return (Salary) | 24Q | 138 |

| Filing | TDS Return (Other – Resident) | 26Q | 140 |

| Filing | TDS Return (Other – Non-Resident) | 27Q | 144 |

| Filing | TCS Return | 27EQ | 143 |

| Filing | SFT Filing | 61A | 165 |

| Filing | Donation Statement | 10BD | 113 |

| Filing | Trust Accumulation Statement | 10 | 109 |

| Filing | Form 26AS Summary | 26AS | 168 |

| Application | PAN Application (India) | 49A | 94 |

| Application | PAN Application (Foreign) | 49AA | 95 |

| Application | TAN Application | 49B | 135 |

| Application | Lower TDS Certificate | 13 | 128 |

| Application | Trust Registration (Provisional) | 10A | 104 |

| Application | Trust Final Registration | 10AB | 105 |

| Appeal | CIT Appeal | 35 | 99 |

| Appeal | ITAT Appeal | 36 | 115 |

| Appeal | ITAT Cross Objection | 36A | 116 |

| Certificate | Tax Residency Certificate | 10FA | 42 |

| Certificate | TDA Benefit Declaration | 10F | 41 |

| Certificate | Salary TDS Certificate | 16 | 130 |

| Certificate | TDS Certificate (Others) | 16A | 131 |

| Certificate | Donation Certificate | 10BE | 114 |

| International Taxation | Foreign Remittance | 15CA | 145 |

| International Taxation | CA Certificate (Foreign Remittance) | 15CB | 146 |

| Special | Option for Charitable Purpose | 9A | 108 |

| Certificate / Declaration | Self-declaration for NIL TDS (15G/15H) | 15G / 15H | 121 |

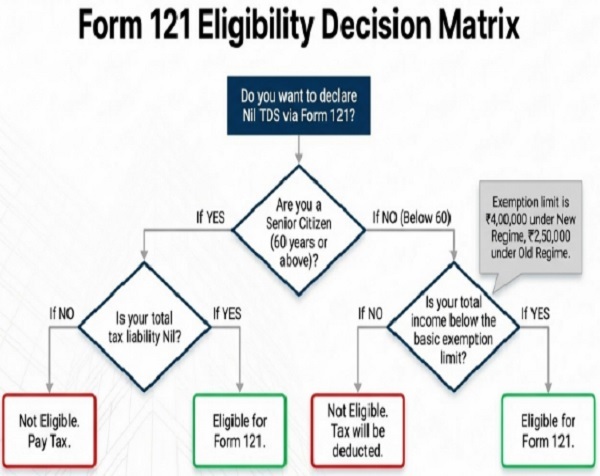

Form 121 – Nil TDS Declaration (Effective from 1 April 2026) (as per Draft Income-tax Rules, 2026 )

From 1 April 2026, the Income Tax Department has introduced Form 121, which replaces Form 15G and Form 15H. This single form allows taxpayers to declare Nil tax liability and avoid Tax Deducted at Source (TDS).

Eligibility Criteria

| Category | Condition |

| Non-Senior Citizens (Below 60 years) | Total income must be below the basic exemption limit |

| Senior Citizens (60 years and above) | Total tax liability must be Nil |

Basic Exemption Limit

New Tax Regime: ₹4,00,000

Old Tax Regime: ₹2,50,000

Applicability

Form 121 can be submitted to prevent TDS on:

Bank FD interest

Dividend income

Rent income

Insurance commission

Certain Provident Fund withdrawals

Key Details to Fill in Form 121:-

1. Personal Details

Name (as per PAN)

Address

PAN number

Status (Individual / HUF)

Residential status

2. Age & Contact Information

Senior citizen status (Yes/No)

Email ID and mobile number

3. Tax Year

Mention the relevant financial year (e.g., 2026–27)

4. Income Declaration

Point 10: Estimated income from the institution where the form is submitted

Point 11: Income declared in other Form 121 submissions to other banks

Point 12: Total aggregate income from all declarations

5. Total Estimated Income

Point 13: Total income for the year including all sources (interest, pension, etc.)

6. Previous ITR Details

Provide ITR acknowledgement numbers and total income of the previous two years.

Disclaimer: This document is prepared for educational and comparative purposes only. The comparison between the Income-tax Act, 1961 and the Income-tax Act, 2025, including references to the Draft Income-tax Rules, 2026, is based on publicly available sources. It should be noted that the Draft Income-tax Rules, 2026 are not yet finally notified, and the provisions may change when the final rules are issued. Therefore, the section mappings and interpretations in this document are indicative in nature. Readers are advised to refer to the official Act, Rules, and notifications and perform proper due diligence before applying the contents of this document in practice.

Data Source:

- Income-tax Act, 1961

- Income-tax Rules, 1962

- Income-tax Act, 2025

- Draft Income-tax Rules, 2026

Author Bio

try to cover each changes . however it is good presentation by author of the article.

just what i was looking for