Krishna Mohan Prasad

Principal Chief Commissioner, Income-tax,

National e-Assessment Centre, Delhi

krishna.m.prasad@incometax.gov.in

Krishna Mohan Prasad is a Graduate in Economics, Law and Post Graduate in Education. An IRS officer of 1984 batch, he has long experience of working in the fields of assessment, search and seizure operations, tax-policy, tax-administration, judicial, representation before ITAT, Intelligence & Criminal Investigation, Legal & Research and is the first Principal Chief Commissioner of Income-tax, National e-Assessment Centre. He has been writing on various aspects of improvement of tax structure in the country and has published article in Economic Times, Financial Express, Journal of Indian Institute of Public Administration, besides contributing to the reports of various committees set up by CBDT and publications of the department like Techniques of Investigation, Audit Manual, and Manual for CIT (Appeals) etc. His hobbies include gardening, Yoga, reading, travelling etc.

Executive Summary

With a view to impart greater efficiency, transparency and accountability, the idea of group assessment of income has been proposed over the last few decades. In the course of the re-structuring of the department, in 2001, a system of group assessment was sought to be introduced by way of setting up of assessment range, where Joint Commissioner of Income-tax, Assistant Commissioner of Income-tax and Income-tax officer were given concurrent jurisdiction over the cases. But as said by Alphonse Karr’s epigram “plus ça change, plus c’est la même chose”usually translated as “the more things change, the more they stay the same,” (Les Guêpes, July 1848), applied ! The group assessment of income actually never took off. Despite notifying dynamic jurisdiction from JCIT to ITO within a Range in 2001, things remained the same and the assessments continued to be made by single Income-tax Officer or Assistant Commissioner of Income-tax or Deputy Commissioner of Income- tax or Joint Commissioner of Income-tax for any assessee for a specific assessment year.

Now, the Group Assessment Scheme has fructified by the legislation of sections 143(3A) and 143(3B) in the Income-tax Act by the Finance Act 2018 and notification of E-assessment Scheme by the notifications S.O. Nos 3264 and 3265 dated 12.09.2019. The scheme is popularly called ‘Faceless Assessement’- both within the Department, amongst tax professionals and in he – print and digital media.

Though, facelessness is a significant aspect of the E-assessment Scheme, the most significant features and the real paradigm shift is group-based assessment in the scheme. As a matter of fact, significant facelessness has been in existence in the assessment system of the Income-tax Department, as the assessing officer seldom saw the face of the taxpayer. The visit of the taxpayers to the Income-tax office and their face to face meeting with the Assessing Officer has always been very rare and in exceptional circumstances. Thus the real and extremely noteworthy change is, in fact, introduction of the system of group assessment with dynamic jurisdiction.

E-assessment Scheme: Group Assessment Scheme:

For the first time in the Income-tax Department, the concept of group assessment will be possible because of the brilliant piece of legislation in the form of E-assessment Scheme 2019. In the paras that follow, the framing of group assessment scheme, it’s essential features and the path to its successful implementation are discussed.

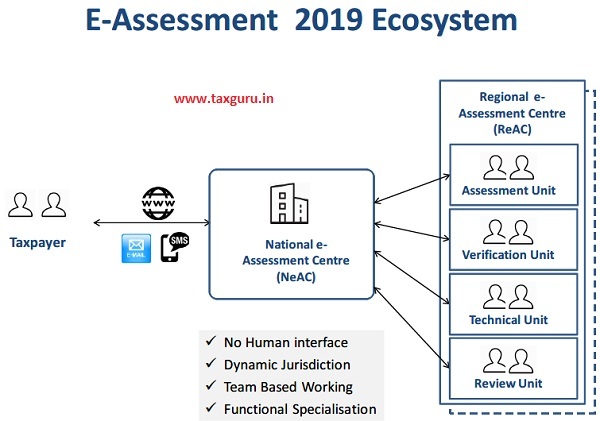

The Group Assessment under the E-assessment Scheme shall be executed through setting up of National e-Assessment Centre at Delhi and following centers and units:

Regional e-Assessment Centers (ReAC)

The number of units is as under:

Units |

India |

Delhi |

Mumbai |

Kolkata |

Chennai |

Ahmedabad |

Bengaluru |

Pune |

Hyderabad |

AU |

100 |

20 |

16 |

16 |

16 |

08 |

08 |

08 |

08 |

VU |

25 |

05 |

04 |

04 |

04 |

02 |

02 |

02 |

02 |

TU |

04 |

01 |

01 |

01 |

01 |

00 |

00 |

00 |

00 |

RU |

09 |

03 |

02 |

02 |

02 |

00 |

00 |

00 |

00 |

Total |

144 |

29 |

23 |

23 |

23 |

10 |

10 |

10 |

10 |

The National e-Assessment Centre (NeAC) has issued notices by electronic mode [under section 143(2) of the Income-tax Act] to 58,322 assesses selected by way of Risk Assessment done by the Directorate of Risk Assessment on the basis of an exercise in Data Mining, and application of Risk rules to the huge amount of data collected by the Directorate of Intelligence and Criminal Investigation, the data from TDS returns, the Income-tax returns and also from various others sources.

The National e-Assessment Centre (NeAC) shall allocate cases by way of Automated Allocation System, on the basis of algorithm for randomized allocation of cases, by using suitable technological tools, including artificial intelligence and machine learning. This would ensure optimum use of resources of 100 assessment units located at 8 Regional e-Assessment Centers at the metropolitan cities of Delhi, Chennai, Kolkata, Mumbai, Ahmedabad, Bengalore, Hydrebad and Pune.

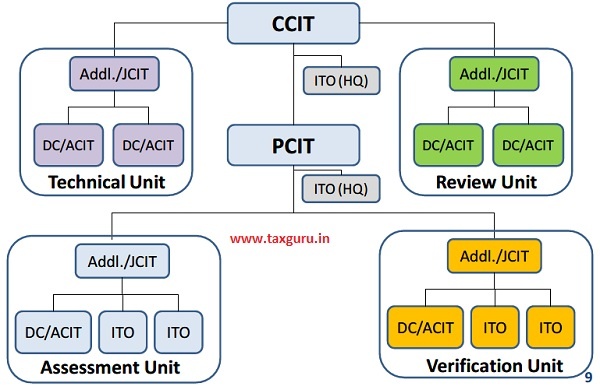

An Assessment Unit (AU) consists of One Joint Commissioner of Income-tax, One Assistant Commissioner of Income-tax, Two Income-tax Officers, assisted by Inspectors of Income-tax, Tax-assistants,Stenographers and Multi-tasking Staff(MTS). The AUs shall be examining the return of income and other documents and shall be preparing notices under section 142(1) of the Income-tax Act for the purpose of inquiry before assessment clearly specifying the accounts and documents which the AO may require. The notice under section 142(1) shall be carefully prepared by AUs and sent to NeAC. The NeAC shall serve the notices to the assessee by electronic mode and when the reply of the assessee by the electronic mode is received, the same shall be forwarded to the concerned AUs.

The AUs shall be sending requests to the NeAC for conducting inquiries and verifications by the Verification Units and for seeking technical assistance from the Technical Units.

The Draft Assessment orders prepared by Assessment Units, incorporating inputs from VUs and TUs are sent to AUs by NeAC. The NeAC shall examine the draft assessment order in accordance with Risk Management strategy and also by way of Automated Examination tools. The action would be followed by either finalization of the assessment order or providing an opportunity to assessee, in case of proposed modification in the return of income in the draft assessment order, or assign it to the review unit.

The Review Unit may concur or suggest modifications to the draft assessment order. The NeAC, on receiving the concurrence of Review Unit may decide to finalize the assessment order or in case modification is suggested by RU, the NeAC shall communicate the same to AU. On receiving further draft assessment order, suggesting modification in RoI, provide opportunity to assessee. Thus, cycle will run and re-run till the draft assessment order is finalized by NeAC.

On finalization of assessment order, NeAC shall serve a copy of the order, notice for penalty proceedings, if any, along with the demand notice, specifying the sum payable or refund due to the assessee.

On completion of assessment, the NeAC shall transfer the entire electronic record of the assessee to the jurisdictional AO for imposition of penalty, collection of demand and other post assessment work.

The Scheme also provides that the NeAC may at any stage of assessment, if it considers necessary, transfer a case to the jurisdictional AO.

For non-compliance of any notice, direction or order under the scheme, on the recommendation of any units of ReAC, the NeAC shall serve a show cause notice for levy of penalty to the assessee or any other person. The response shall forward to the concerned unit recommending penalty, the concerned unit may drop the penalty under intimation to NeAC or make a draft penalty order and send it to NeAC. The NeAC shall levy penalty as per the draft order.

The appeal against assessment made by NeAC shall lie before CIT(A) having jurisdiction over jurisdictional AO.

All communications between NeAC and the assessee/his authorized representative and all internal communication between NeAC and ReAC and various units shall be made exclusively by electronic mode.

The authentication of electronic record by the originator in the NeAC and ReAC shall be by affixing digital signature as per Section 3(2) of the Information Technology Act, 2000 and by the originator being an assessee or any other person by the digital signature or by way of electronic signature or electronic authentication technique as per Section 3A(2) of the Information Technology Act, 2000.

The delivery of electronic record i.e. notice or order or electronic communication under the Scheme to the assessee shall be done by way of placing authenticated copy to the assessee’s registered account; or sending to the registered email address of the assessee or AR, or uploading it on the assessee’s Mobile App; and followed by real time alert.

The assessee shall file his response through his registered accounts and once acknowledgment is sent by the NeAC, containing hash result, the response shall be deemed to be authenticated.

No personal appearance by the assessee or AR shall take place at NeAC or ReAC. The assessee shall be provided opportunities or may seek personal hearing to make oral submission in a case of proposed modification of RoI in the draft assessment order and the hearing shall be conducted exclusively through video conferencing or video telephony as per procedure laid down by Board. A similar procedure is to be followed for any examination or recording of statement (except the statement recorded in course of search u/s 133A.)

The Principal CCIT, NeAC, has been given the power to specify Format, Mode, Procedure and Process (FMPP) for effective functioning, general administration, grievance mechanism of NeAC, ReAC and Unit set up in the automated and mechanized environment.

In the course of Gyan Sangam on 01 September 2017, Shri Narendra Modi, Prime Minister of India, asked the tax officer to introduce a system in which taxpayers do not have to come to the tax-office and taxpayer and tax official do not come face to face. The reactions of the senior tax officials were that – ‘it’s impossible, legally as well as administratively’, ‘scrutiny assessment made without face to face with the taxpayer wouldn’t stand judicial scrutiny’, ‘it’s extremely difficult and is not required as the taxpayers shall be facing the authorities in the course of appeal at the level of CIT(A), ITAT, HC or SC so eliminating face to face contact at one level does not serve much purpose’.

The Group & Faceless E-assessement has been made possible on account of enormous legislative and administrative knowledge and wisdom acquired and developed in the Income-tax department over past many decades in preparing draft for direct tax legislations, finance bills, issuing of circulars, clarification, notifications etc. for improvement in direct tax structure.

The innovative legislation was introduced by the Finance Act, 2018 in form of sub-sections (3A), (3B) and (3C) in Section 143(3) of the Income-tax Act with effect from 01.04.2018.

Section 143(3A) provides that the central government shall make a scheme for the purpose of making assessment so as to impart greater efficiency, transparency and accountability by eliminating the interface between the Assessing Officer and the assessee in the course of proceedings to the extent technologically feasible; optimizing utilization of the resources through economies of scale and functional specialization and introducing a team-based assessment with dynamic jurisdiction.

Section 143(3B) provides that the central government may for giving effect the Scheme direct that any provisions of the Income-tax Act relating to the assessment of total income shall not apply or “shall apply with such exceptions, modifications and adaption as may be specified in the notification before 31.03.2020.

Section 143(3C) provides that the notifications under section 143(3A) and 143(3B) shall be laid before each house of the Parliament as soon as the notification is issued.

The central government framed E-assessment Scheme, 2019 vide S.O. No 3264 dated 12.09.2019, also known as Notification No 61/2019 and directions vide notification S.O. No 3265 dated 12.09.2019, details of which have been discussed above.

The Group & Faceless E-assessment Scheme, 2019 can successfully be implemented with the help of the enormous infrastructure and skills developed by the Directorate of Systems of Income-tax Department which has been undertaking extensive computerization over the past three decades. The office of Director General of Income Tax (Systems) is an attached office of the Central Board of Direct Taxes, consisting of five ADG (Systems), CIT (CPC-ITR) at Bengaluru, CIT(CPC-TDS). It carries out the work of conceptualization, planning, procurement, installation and maintenance of various projects and related hardware etc. procurement of software packages, development and maintenance of application software, technical support, Management of National Databases, monitoring of all-India network, recruitment of technical personnel, training of non-technical and technical Officers and staff etc. as part of modernization of the Department through comprehensive computerization.

The Directorate of Systems stellar achievement has been in developing and maintaining the facilities for enormous collection of significant financial transactions, collected on the basis of 285BA of the Income-tax Act by the efforts of Directorate of Intelligence & Criminal investigation, data obtained under FATCA of USA, under CRS from more than hundred countries as per OECD provisions, data of TDS, information from ROI of taxpayers, and information from various other agencies. The data is analyzed by the Directorate of Risk Assessment in collaboration with the ‘Project Insight’ headed by ADG(Systems).

The Portal www.incometaxindia.gov.in for filling e-returns and also portal designated under e-Assessment Scheme, is maintained by a team headed by ADG(Systems).

The functionality of allocation of cases and electronic communications between assessee and NeAC and among NeAC & ReACs and NeAC & Jurisdictional AO is provided by ITBA team headed by ADG(Systems).

Thus, the Directorate of Systems provides the fulcrum for implementation of E-assessment Scheme which is well depicted as under:

The E-assessment Scheme, 2019 has made a significant beginning by undertaking assessment of 58,322 cases of limited and unlimited scrutiny, consisting of cases of individual, firm, companies etc. The Human Resource sanctioned for implementing the Scheme is form of sanctioned strength of one Principal Chief Commissioner of Income-tax and One Commissioner of Income- tax, two additional commissioner of Income-tax, Four Deputy Commissioner of Income-tax, One Income-tax Officer, eleven Income-tax Inspectors, Administrative Officers, Office Superintendent, Senior Tax Assistants & Tax Assistants, Stenographers II & III, Personal Secretaries and Multi Tasking Staffs at NeAC, and for ReACs four Chief Commissioner of Income-tax, twenty-five Principal Commissioner of Income-tax, and other officers and officials as under:

| Officers/Officials

|

HQs of CCIT & PCIT | Assessment Unit | Verifi-cation Unit | Tech-nical Unit | Review Unit | Total |

| Addl./JCIT | 00 | 100 | 25 | 04 | 13 | 142 |

| DC/ACIT | 00 | 100 | 25 | 08 | 26 | 159 |

| ITO | 29 | 200 | 50 | 00 | 00 | 279 |

| Inspector of IT | 29 | 500 | 100 | 16 | 39 | 684 |

| Executive Assistants | 112 | 700 | 75 | 20 | 52 | 959 |

| Multi Tasking Staff | 58 | 400 | 100 | 12 | 39 | 609 |

| Total no of Officers & Officials | 228 | 2000 | 375 | 60 | 169 | 2832 |

India is one of the pioneers to launch Group and Faceless E-assessment Scheme with minimal Human Interface. The scheme is likely to reduce cost of compliance of the taxpayers and administrative cost of the Government and litigation significantly.

It is an eco-friendly scheme in view of electronic communications and substantial elimination of use of paper. As traveling to Income-tax office would not be required for e-Assessment proceedings, it would lead to better traffic management, and reduction in air pollution of cities in India. The Group & Faceless E-assessment Scheme would lead to greater transparency, efficiency and better assessment of Income, it is win-win for all except the unscrupulous taxpayers; the honest taxpayers benefit in form of better assessment of Income and significant reduction, if not elimination of high-pitched Assessments, the conscientious tax collector benefit in form of improved image of its service and greater job satisfaction.

The media coverage of National e-Assessment Scheme has been unprecedented. There has been wide coverage in the print and electronic media as well as on the social media like twitter, face- book etc. and the response has been encouraging and positive. The prime minister, finance minister and large number of eminent policy maker, tax advisor have hailed it as a mile stone for taxation reforms in India to a major step in improving the ease of doing business and even the ruling party has hailed it as ‘Modifying The Indian Economy The Digital Way’.

The exceptional interest and focus on E-assessment has placed onerous responsibility upon the group of 619 officers and 2319 officials posted to undertake the complex work of assessment of 58,322 cases selected in the first phase, consisting of 15,084 complete scrutiny cases, 9,527 corporate limited scrutiny cases and 33,711 limited scrutiny cases of individuals, firms, etc. The format, mode, procedure and process for effective functioning and standards for effective functioning of NeAC and ReAC are being prescribed. Intensive training of Human Resources, Infrastructure like office space and its designing, computer resources and its specification, financial requirements, further legislative changes required, co-ordination with the Directorate of Systems, office of the Cadre Control Principal Chief Commissioner of Income Tax, Central Board of Direct Taxes, Directorate of Infrastructure, National e-Governance Division of government of India etc are under way to implement this prestigious and significant scheme.

The faceless assessment is going to be the new face of Income-tax Department as this scheme is likely to be expanded substantially as time goes by. The initial thought of the author is to expand the Group & Faceless E-assessment Scheme to 5,00,000 assessments – 4,00,000 Limited and 1,00,000 unlimited, Setting up of 500 assessment units and with view to curb tax-evasion and detection of black money, it is imperative to have effective deterrence in form of levy of penalty for concealment of income and launching of prosecution for willful evasion of tax. The E-assessments should lead to levy of penalty in at least one lakh cases and launching of prosecution in 25000 cases each year. This would lead to realization of dream of Late Shri Arun Jaitley, our beloved Finance Minister in making India a more tax compliant nation.