Gist and a Snap Analysis of SC Judgment – Union of India Vs Ashish Agarwal (Supreme Court), Appeal Number : Civil Appeal No. 3005/2022, Date of Judgement: 04/05/2022

1. The Union felt aggrieved due to the adverse outcome of several writ petitions which were filed on PAN India basis against notices issued u/s 148 of the Income Tax Act 1961. The common underlying premise was that the same are bad in law considering the amendment by Finance Act 2021 whereby provisions were substantially changed in respect of sections 147 to 151 w.e.f April 1,2021 (changes essentially introduced in the light of the decision in the case of GKN Driveshafts (India) Ltd. Vs. Income Tax Officer and ors; (2003) 1 SCC 72. Thus, this civil appeal was filed to seek justice.

2. In a nutshell, all such appeals and petitions sought relief on the following grounds from the High Courts:

a. No valid “reason to believe”

b. No tangible/reliable material/ information in possession of the AO leading to formation of the belief that income has escaped assessment;

c. No enquiry being conducted by the AO prior to the issuance of notice and the reopening is based on change of opinion of the AO;

d. Lastly, the mandatory principle/procedure laid down by the GKN Driveshafts (India) Ltd. Vs. Income Tax Officer and ors; (2003) 1 SCC 72 is not followed in principle

3. This Judgement, in anticipation, was mooted as an extremely crucial and far reaching one in that almost 90000 notices were issued by the revenue. In a spirited movement challenging the same to be bad in law, 9000 writ petitions were filed on pan India basis to seek justice from the Apex Court as a last resort.

4. Apex Court has passed above judgement under Article 142 of the Constitution of India (reproduced below) which would govern all other judgements and orders passed by various High Courts. Thus, Revenue need not file any further appeals in any other court in the light of this judgement.

Article 142 in The Constitution of India 1949

“142. Enforcement of decrees and orders of Supreme Court and unless as to discovery, etc ( 1 ) The Supreme Court in the exercise of its jurisdiction may pass such decree or make such order as is necessary for doing complete justice in any cause or matter pending before it, and any decree so passed or orders so made shall be enforceable throughout the territory of India in such manner as may be prescribed by or under any law made by Parliament and, until provision in that behalf is so made, in such manner as the President may by order prescribe

(2) Subject to the provisions of any law made in this behalf by Parliament, the Supreme Court shall, as respects the whole of the territory of India, have all and every power to make any order for the purpose of securing the attendance of any person, the discovery or production of any documents, or the investigation or punishment of any contempt of itself”

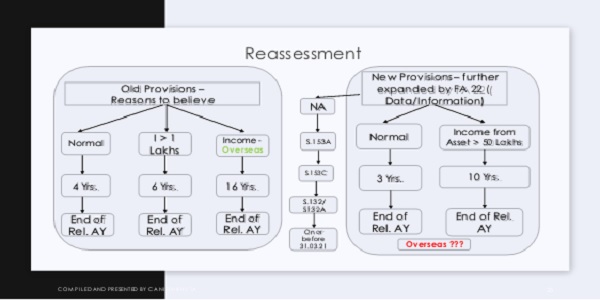

5. Reassessment provisions prior to 01.04.21, after 01.04.21 (Simple pictorial presentation with GKN Driveshafts India Ltd Judgement implications) and now amended by Finance Act 2022.

Interestingly, the new provisions (Section 148A) introduced by FA 21 were considered as radical, reformative and assessee friendly; and such changes were mooted as part of the initiative towards simplifying tax administration, easing compliances and reducing litigations through the introduction of remedial and benevolent provisions.

It now appears that with the relevant amendments ushered in by the Finance Act 2022, the period of 3 years u/s 148A is technically extended to 10 years. Therefore, changes introduced after 1.4.21 are only for academic discussions. Using RMS and AAS and requirements of approval for such selection is practically dispensed away with.

6. Extension of Time Limits – Section 3 of Relaxation Act 2020 – to extend time limits of section 149/148 for reassessments

| Notification Date | Original Limitations for issuance of notice u/s 148 of the Act | Extended Notification Date |

| 31.03.2020 | 20.03.20 to 29.06.20 | 30.06.20 |

| 24.06.2020 | 20.03.20 to 31.12.20 | 31.03.21 |

| 31.03.2021* | 31.03.21 | 30.04.21 |

| 27.04.2021* | 30.04.21 | 30.06.21 |

* Stipulated that the provisions, as they existed prior to the amendment by the Finance Act, 2021, shall apply to the reassessment proceedings initiated thereunder.

Will this rather exceptional Supreme Court ruling encourage and pave the way for introduction and promulgation of ordinances by the Authority whenever such a need arises? That would be ominous as it would provide scope for extensions with alternate time limits for the Revenue, which could frustrate the established provisions relating to reassessment proceedings.

7. It needs to be mentioned here that the Delhi HC judgement quashed such reassessment notices albeit with their accompanying remark that:

Quote

” if the law permits the revenue to take further steps in the matter, they

shall be at liberty to do so. “

Unquote

“Did such a specific remark lay the foundation, thereby inviting the differing view and judgement of the Supreme Court under Article 142 of Constitution of India?” (Some food for thought …)

Further, while it was expected that the High Courts would have given some leeway in favour of Revenue, what about the genuine Taxpayers – are they not in the reckoning to be entitled to a similar benefit?

8. Final Ratio

a. All notices issued are considered as issued under Section 148A of the Income Tax Act 1961, thus they are considered as valid in law;

b. AO is now required to provide material and information to the Assessee within 30 days from today i.e., on or before 02.06.2022 for such reopening;

c. Assessee should file the reply within two weeks from date of delivery of such communications (On SMS/E-mail/Portal/App etc.) as applicable;

d. The requirement of the specified authority seeking prior approval is done away with as a one-time measure for all such notices which were quashed by HCs (9000 writ petitions);

e. AO is expected to follow the procedure laid down as per section 148A(b) and shall pass a speaking order u/s 148A(d) to proceed further in respect of each of the assessee (90000 of them)

f. All defenses are kept open for either side viz. assessee & AO

g. In view of verdict passed under Article 142 of Constitution of India, is it that the judgements and verdicts passed shall be substituted or modified to that extent to safeguard the interests of Revenue only? Can it really be viewed as a balanced verdict which is equitable to both the parties?

Concluding Comment: Is it fair? does it evoke the feeling that principles of natural justice are followed? Did the verdict miss the opportunity of correction under Article 142? I leave my thoughts with all readers to study, deliberate and reflect analytically this intriguing verdict through the prism of their knowledge and experience.

The decision of Apex Court needs to be accepted with humility and honour, the wisdom thereof needs to be understood and evaluated.

Encl: Copy of the Judgement passed on 04.05.2022

(Union of India v. Ashish Agarwal Civil Appeal No. 3005 of 2022)

Author Bio

First Notice was issued on 30Mar21. will sec 148A will be applicable.

if case is reopened after 8 yrs, then escapement of income should be > Rs 50L. But during reassessment, if it is realised that escapement is < Rs 50L then is the reassessment is right.

If assessments proceedings are taken up and if the same has been co-operated by the assessee then you can file your objections in the defense to take the stand as the value involved is beyond the applicability of such provisions and if the defense is considered valid with substantiation and then such proceedings may be dropped by AO. It all depends on facts to facts of each case.

Now CIT will decide appropriately… you should defend on merits to seek relief desired as orders passed and assessee has filed Appeals so this judgement may not help technically

Dear Nitin bhai,

What will be the status of those cases wherein , though notices issued after 31.3.21, but the due procedures/steps not followed by AO and he has already passed orders violating principles of natural justice? Since the cases are pending in appeals , can CIT appeals take recourse this judgement of honorable SC to decide the case afresh ?

Plz guide