Case Law Details

ITO Vs Malibu Estate Dispensary Pvt. Ltd (ITAT Delhi)

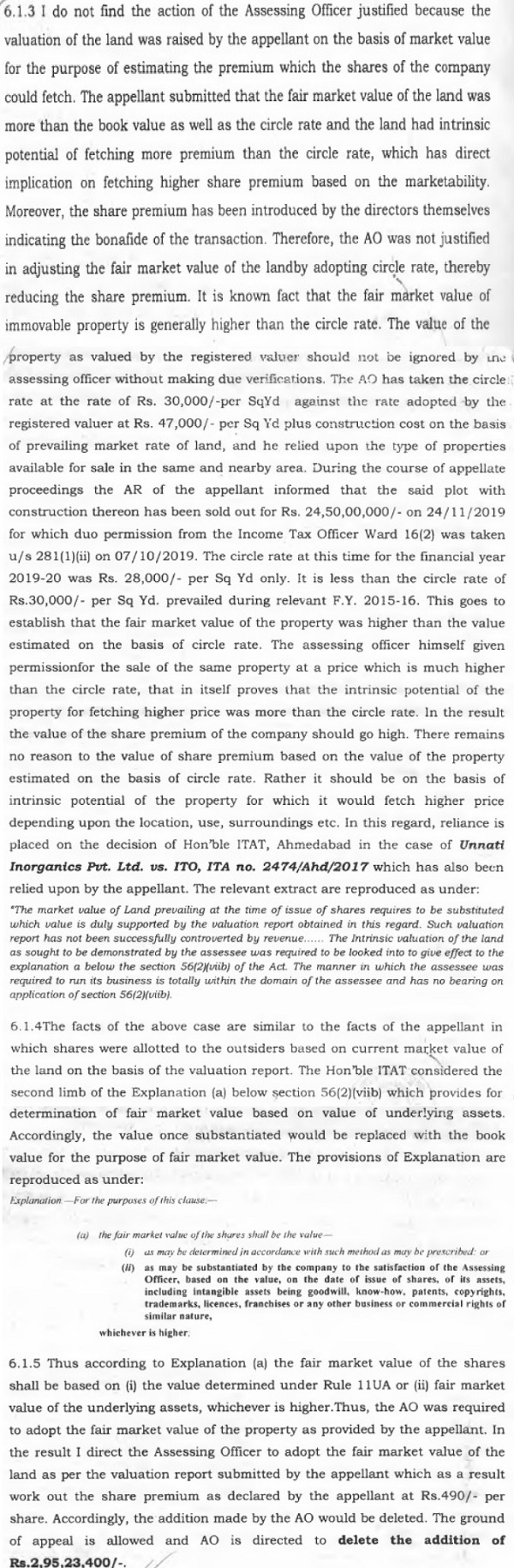

Briefly stated the facts of the case are that the assessee company is under taking construction of dispensary/ hospital at Gurgaon. During the year under consideration the assessee introduced share capital/ share premium in respect of total number of shares allotted at 152816 with face value of Rs.1428160/- and premium of Rs.69979840/-. The share premium was @ 490 per share. During the course of the scrutiny assessment proceedings and on perusal of the financial statements the AO learned that the NAV of shares was Rs. 10 as per rule 11 UA of the IT Rules as per book value of assets and liabilities as on 31.03.2015. Accordingly the AO was of the opinion that the total consideration as per NAV should be Rs.1428160/- and the AO formed a belief that the assessee company has received excess amount of Rs.69979840/- and a show cause notice was issued to the assessee asking it to give explanation for issuance of shares at huge premium. The assessee filed a detailed reply and supported its claim by a valuation report from a registered valuer and a certificate from the CA in respect of the valuation. The AO found that the stamp duty value / circle rate was Rs. 30,000/- per square yard and adopting the same the AO computed the addition on account of excess share premium received at Rs.29562912/-.

ITAT carefully perused the orders of the CIT(A) viz-a-viz the assessment order. There is no dispute that the AO has not given any valid reason for discarding valuation report of a registered valuer filed by the assessee. It is equally true that as per explanation a to section 56 (2)(viib) of the Act it has been specifically provided that the fair market value (FMV) of the shares shall be based on (1) the value determined under rule 11UA or (2) fair market value of the under lying assets whichever is higher. Therefore, in our understanding of the law the AO grossly erred in adopting the circle rate of the property. Considering the facts of the case in totality in the light of the relevant provisions of the Act we do not find any reason to interfere with the findings of the CIT(A). The appeal filed by the revenue is dismissed.

FULL TEXT OF THE ORDER OF ITAT DELHI

This appeal by the revenue is preferred against the order of the CIT(A)-32, New Delhi dated 30.12.2019 for A.Y.2016-17.

2. The solitary grievance of the revenue is that the CIT(A) erred in deleting the addition of Rs.29562912/- on account of difference in share price viz-a-viz Fair Market Value.

3. Briefly stated the facts of the case are that the assessee company is under taking construction of dispensary/ hospital at Gurgaon. During the year under consideration the assessee introduced share capital/ share premium in respect of total number of shares allotted at 152816 with face value of Rs.1428160/- and premium of Rs.69979840/-. The share premium was @ 490 per share. During the course of the scrutiny assessment proceedings and on perusal of the financial statements the AO learned that the NAV of shares was Rs. 10 as per rule 11 UA of the IT Rules as per book value of assets and liabilities as on 31.03.2015. Accordingly the AO was of the opinion that the total consideration as per NAV should be Rs.1428160/- and the AO formed a belief that the assessee company has received excess amount of Rs.69979840/- and a show cause notice was issued to the assessee asking it to give explanation for issuance of shares at huge premium. The assessee filed a detailed reply and supported its claim by a valuation report from a registered valuer and a certificate from the CA in respect of the valuation. The AO found that the stamp duty value / circle rate was Rs. 30,000/- per square yard and adopting the same the AO computed the addition on account of excess share premium received at Rs.29562912/-.

4. The assessee strongly agitated the matter before the CIT(A) and contended that the shares were issued by the company to the existing share holders and the AO has not cited any reason for rejection of valuation report for FMV of the property. It was further brought to the notice of the CIT(A) that the AO has not given any reason for the adoption of circle rates of land for valuation of property.

5. After considering the facts and the submissions the CIT(A) observed as under :-

6. Before us the DR strongly supported the findings of the AO but could not point out any factual error in the findings of the CIT(A) (supra).

7. We have carefully perused the orders of the CIT(A) viz-a-viz the assessment order. There is no dispute that the AO has not given any valid reason for discarding valuation report of a registered valuer filed by the assessee. It is equally true that as per explanation a to section 56 (2)(viib) of the Act it has been specifically provided that the fair market value of the shares shall be based on (1) the value determined under rule 11UA or (2) fair market value of the under lying assets whichever is higher. Therefore, in our understanding of the law the AO grossly erred in adopting the circle rate of the property. Considering the facts of the case in totality in the light of the relevant provisions of the Act we do not find any reason to interfere with the findings of the CIT(A). The appeal filed by the revenue is dismissed.

8. Decision announced in the open court on 21.09.2022.