Following major proposed amendments have been covered:

1. Incentives for affordable rental housing

2. Extension of date of sanction of loan for affordable residential house property

3. Extension of date of incorporation for eligible start up for exemption and for investment in eligible start-up

4. Increase in safe harbour limit of 10% for home buyers and real estate developers selling such residential units

5. Relaxation for certain category of senior citizen from filing return of income-tax

6. Rationalisation of provisions of Minimum Alternate Tax (MAT)

7. Rationalisation of the provisions concerning withholding on payment made to Foreign Institutional Investors (FIIs)

8. Rationalisation of provisions relating to tax audit in certain cases

9. Advance tax instalment for dividend income

10. Extending due date for filing return of income in some cases, reducing time to file belated return and to revise original return and also to remove difficulty in cases of defective returns

11. Payment by employer of employee contribution to a fund on or before due date

12. Constitution of Dispute Resolution Committee for small and medium taxpayers

13. Constitution of the Board for Advance Ruling

14. Income escaping assessment and search assessments

15. Provision for Faceless Proceedings before the Income-tax Appellate Tribunal (ITAT) in a jurisdiction less manner

16. Discontinuance of Income-tax Settlement Commission

17. Reduction of time limit for completing assessment

18. Rationalisation of the provision of slump sale

19. Rationalisation of provision of transfer of capital asset to partner on dissolution or reconstitution

20. Rationalisation of the provisions of Equalisation Levy

21. Depreciation on Goodwill

22. Rationalisation of the provision of presumptive taxation for professionals under section 44ADA

23. Definition of the term ―Liable to tax

24. Rationalisation of the provision relating to processing of returned income and issuance of notice u/s 143(1) & (2) of the Act

25. Tax Deduction at Source (TDS) on purchase of goods

26. TDS/TCS on non-filer at higher rates

27. Taxability of Interest on various funds where income is exempt

Incentives for affordable rental housing

Sec 80IBA profits and gains derived from the business of developing and building affordable housing project, now includes rental housing project as notified by the CG.

Approval under for this affordable housing can now be taken till 31/03/2022 to claim deduction.

Extension of date of sanction of loan for affordable residential house property

Deduction u/s 80EEA can now be taken for interest on loan taken for residential house property sanctioned till 31/03/2022.

Monetary Limits:

- Deduction: <= Rs. 1,50,000/-

- Stamp Duty of Residential House Property <= Rs. 45,00,000/-

Extension of date of incorporation for eligible start up for exemption and for investment in eligible start-up

Sec 80-IAC: Deduction of 100% profits to eligible start-up incorporated between 01/04/2016 to 31/03/2022 for 3 consecutive AYs out of initial 10 AYs; Total Turnover <= Rs. 100 crores

Sec. 54GB: Exemption of Capital Long-term on transfer of Residential property (house or Plot of land) transferred on or before 31/03/2022 (extended from 31/03/2021) on investing the net consideration for subscription in the equity shares of an eligible start-up.

4. Increase in safe harbour limit of 10% for home buyers and real estate developers selling such residential units [w.e.f. AY 2021-22]

Sec. 43CA: Increase in Safe Harbour Limit to 20% (from 10%) for Real Estate Developers in selling Homes subject to following conditions:

> Transfer of Residential Unit >= 12th November 2020 <= 30th June 2021

> Transfer of the Unit is 1st time allotment to any person

> Consideration <= Rs. 2 crores

Sec. 56(2)(x): Increase in Safe Harbour Limit to 20% (from 10%) for buyers of the residential units mentioned above

5. Relaxation for certain category of senior citizen from filing return of income-tax [w.e.f. AY 2021-22]

- Resident of India

- Age >= 75 Years

- Have Pension income + Interest Income from Same Bank in which he is receiving pension

- Bank to be specified Bank by CG

- This Assessee require to furnish Declaration to the Bank as per prescribed form

- On basis of declaration the Bank would do TDS as per rates in force after considering the Chapter VI-A Dedcution+ any rebate u/s 87A

- Points to ponder: Oonchi Dukaan Feeka Pakwaan

6. Rationalisation of provisions of Minimum Alternate Tax (MAT) [w.e.f. AY 2021-22]

Sec 115JB: Adjustment in relation to following proposed under this section:

> Past year income included in Books of PY on account of adjustment due to APA u/s 92CC or Secondary Adjustment u/s 92CE to be adjusted on request made by assessee to the AO for recomputing the book profit of the past years and tax payable, if any, as prescribed.

> Similar treatment to dividend as there is for capital gains on transfer of securities, interest, royalty and Fee for Technical Services (FTS) in calculating book profit u/s 115JB (where such income is taxed at lower rate than MAT rate due to DTAA)

7. Rationalisation of the provision concerning withholding on payment made to Foreign Institutional Investors (FIIs) [w.e.f. AY 2021-22]

Sec. 196D: TDS on income of FII from securities u/s 115AD(1)(a) (other than interest referred in section 194LD)

Proviso to section 196D(1): In case of a payee to whom an agreement referred u/s 90(1) or 90A(1) applies and such payee has furnished the tax residency certificate referred to in section 90(4) or 90A(4), then the TDS to be lower of following:

a. 20%; or

b. rate or rates of income-tax provided in such agreement for such income.

8. Rationalisation of provisions relating to tax audit in certain cases [w.e.f. 2021-22]

Sec 44AB: Threshold limit for a person carrying on business for Tax Audit purposes increased to Rs. 10 crores (from Rs. 5 crores) where:

(i) aggregate of all receipts in cash during in PY <= 5% of such receipt; and

(ii) aggregate of all payments in cash during in PY <= 5% of such payment.

9. Advance tax instalment for dividend income [w.e.f. AY 2021-22]

Sec. 234C: No interest on Advance Tax calculated on Dividend if full tax paid in subsequent Advance Tax instalment due to intrinsic nature of this income post when it became taxable in hands of the recipient

10. Extending due date for filing return of income in some cases, reducing time to file belated return and to revise original return and also to remove difficulty in cases of defective returns [w.e.f. AY 2021-22]

Sec. 139(4) and (5): Due date for filing Belated Return [139(4)] as well as Revised Return [139(5)] preponed to 31st December of the relevant AY from 31st March (i.e. end of relevant AY)

Sec. 139 (9): Return would not be considered defective for a class of assessee or shall apply with such modifications, as maybe specified

11. Payment by employer of employee contribution to a fund on or before due date [w.e.f. AY 2021-22]

Sec 36 and 43B: Provisions of Sec 43B do not apply and deemed to never have been applied to a sum received by the assessee from any of his employees to which provisions of section 2(24)(x) applies, i.e., any sum received by assessee from its employees as contribution to any PF or superannuation fund or ESI Act or any other fund for welfare of the employees. Therefore, u/s 36(1)(va) “due date” to mean the date by which the assessee is required as an employer to credit an employee’s contribution to the employee’s account in the relevant fund under any Act, rule, order or notification issued there-under or under any standing order, award, contract of service or otherwise.

12. Constitution of Dispute Resolution Committee (DRC) for small and medium taxpayers [w.e.f. AY 2021-22]

Sec. 245MA (New):

> CG shall constitute >=1 DRC

> DRC shall resolve disputes of persons or class of persons specified by CBDT, optional for these assessees

> Monetary Limits for disputes

-

- Returned Income <= Rs. 50 lakhs

- Aggregate amount of variation proposed <= Rs. 10 lakhs

> Specified orders u/s 132 (Search), 132A (Requisition), 133A (Survey), 90 & 90A (information received under an agreement referred these sections) – Not eligible for DRC

> Benefit of this section would not be available in cases of detention, prosecution or conviction of assessees under various specified laws.

> Other conditions which CBDT would prescribe

> DRC’s Powers:

-

- Reduce or waive penalty under the Act; or

- Grant immunity from prosecution for any offence under the Act

13. Constitution of the Board for Advance Ruling:

The Authority for Advance Rulings (AAR) shall cease to operate with effect from such date, as may be notified by the CG, due to long vacancy of its Chairman and Vice-chairman positions as unable to search for eligible candidates Instead

Proposed that CG shall constitute >= 1 Board for Advance Rulings:

√ Which consists of 2 members, each being an officer not below (>) the rank of Chief Commissioner

√ Where Advance rulings of such Board shall not be binding on the applicant or the Department and can be appealed by the aggrieved party before the High Court

14. Income escaping assessment and search assessments [w.e.f. AY 2021-22]

New Proposed procedure for Income escaping assessment:

Sec. 148A (New): Before issuing any notice u/s 148 to any assessee for assessment or reassessment or recomputation u/s 147, AO have to perform following tasks (except for search or requisition cases):

-

- Get approval of specified authority

- conduct enquiries, if required, w.r.t. information which suggests that income has escaped assessment

- provide an opportunity of being heard to the assessee by serving upon him a notice to show cause

- After considering reply of the assessee and other material on record, AO shall decide whether it is a fit case for issue of notice u/s 148 and serve a copy of such order along with such notice with prior approval of specified authority

Sec 148: After following procedure u/s 148A, the AO shall serve on the assessee a notice, along with a copy of the order passed, if required, u/s 148A(d), requiring him to furnish return of his income or the income of any other person in respect of which he is assessable under, within such period as may be specified in such notice.

[Explanation 1 to Sec. 148 defines the information with AO which suggests that the income chargeable to tax has escaped assessment means,—

(i) any information flagged in the case of the assessee for the relevant AY in accordance with the risk management strategy formulated by the Board from time to time;

(ii) any final objection raised by the C&AG of India to the effect that the assessment in the case of the assessee for the relevant AY has not been made in accordance with the provisions of this Act.]

Sec. 147: AO can assess or reassess such income or recompute the loss or the depreciation allowance or any other allowance or deduction for such AY when income chargeable to tax has escaped assessment for that AY

Sec. 149: Time limit for notice u/s 148:

Normal Cases: Notice u/s 148 can be issued <= 3 years from the end of the relevant AY

Specific Cases: If AO has in his possession any evidence which reveal that the income escaping assessment, represented in the form of asset, amounts to or is likely to amount to >= Rs. 50 lakhs, notice u/s 148 can be issued > 3 years but < = 10 years from the end of the relevant AY.

15. Provision for Faceless Proceedings before the Income-tax Appellate Tribunal (ITAT) in a jurisdiction less manner [w.e.f. AY 2021-22]

Sec. 255(7), (8) & (9): CG may notify a scheme for the purposes of disposal of appeal by the ITAT so as to impart greater efficiency, transparency and accountability by,—

(a) eliminating the interface between the ITAT and parties to the appeal in the course of proceedings to the extent technologically feasible;

(b) optimising utilisation of the resources through economies of scale and functional specialisation;

(c) introducing an appellate system with dynamic jurisdiction.

Points to ponder:

- Whether such amendment can be made w.r.t. ITAT by way of Finance Bill?

- If ITAT becomes jurisdiction less, that means all future decisions by ITAT would prevail all over India?

- Centralisation of powers instead of decentralising and that too with the CG?

16. Discontinuance of Income-tax Settlement Commission [w.e.f. 01 Feb 2021]

17. Reduction of time limit for completing assessment

Sec. 153: Limit for completion of assessment proceedings proposed to be reduced further by 3 months i.e. time for completing of assessment is proposed to be <= 9 months from the end of AY in which the income was first assessable, for the AY 2021-22 and subsequent AY.

18. Rationalisation of the provision of slump sale [w.e.f. AY 2021-22]

Sec. 2(42C): Slump sale to include slump exchange, and definition of transfer widened by referring to definition of transfer u/s 2(47).

19. Rationalisation of provision of transfer of capital asset to partner on dissolution or reconstitution [w.e.f. AY 2021-22]

Sec. 45 and 48: Capital Gain Taxable in the hands of Specified Entity which transfers any Capital Asset in lieu of/ against his proportion of capital contribution in the name of specified person at the time of dissolution or reconstitution of the said specified entity. FMV of the said capital asset on date of receipt by the specified person is deemed to be full value of consideration. Cost of acquisition would be the capital contribution of the specified person in the books of specified entity at the time of dissolution or reconstitution without taking into account any increase in capital due to revaluation of any asset or due to self-generated goodwill or any other self-generated asset.

Similar, ratio applicable to the receipt of any money or other asset by the specified person at time of dissolution or reconstitution of the specified entity.

For the purposes of Sec. 45 (4) and (4A)-

> Specified Person: is a person who is partner of a firm or member of other association of persons or body of individuals (not being a company or a cooperative society), in any previous year;

> Specified Entity: is a firm or other association of persons or body of individuals (not being a company or a cooperative society); and

> Self-generated Goodwill and Self–Generated Assets: are goodwill or asset, as the case may be, which has been acquired without incurring any cost for purchase or which has been generated during the course of the business or profession.

20. Rationalisation of the provisions of Equalisation Levy which is in respect of E-commerce operator [w.e.f. AY 2021-22]

Explanation to section 163 of the Finance Act, 2016:

Clarifying that Consideration received or receivable for specified services and consideration received or receivable for e-commerce supply or services shall not include consideration which are taxable as royalty or fees for technical services (FTS) in India under the Income-tax Act read with DTAAs or Treaties entered by India with respective Tax Jurisdictions.

Explanation to clause (cb) of section 164 of the Finance Act, 2016:

“Online sale of goods” and “online provision of services” shall include one or more of the following activities taking place online:

(a) Acceptance of offer for sale;

(b) Placing the purchase order;

(c) Acceptance of the Purchase order;

(d) Payment of consideration; or

(e) Supply of goods or provision of services, partly or wholly

[Clarifying and widening the scope of e-commerce supply or service]

165A of the Finance Act, 2016:

Consideration received or receivable from e-commerce supply or services shall include:

(i) consideration for sale of goods irrespective of whether the e-commerce operator owns the goods; and

(ii) consideration for provision of services irrespective of whether service is provided or facilitated by the e-commerce operator.

Exemption u/s 10 (50) have also been amended accordingly.

21. Depreciation on Goodwill [w.e.f. AY 2021-22]

No depreciation on Goodwill irrespective of the fact that it is either purchased or self-generated goodwill.

22. Rationalisation of the provision of presumptive taxation for professionals under section 44ADA [w.e.f. AY 2021-22]

Applicable to individual, HUF or partnership firm and not to LLP

Points to Ponder:

- How HUF can provide professional services?

- Whether any partnership firm converts into LLP, then it can come out of the Tax Audit due to applicability of Sec. 44ADA?

23. Definition of the term ―Liable to tax [w.e.f. AY 2021-22]

The Act currently does not define the term ―liable to tax, though this term is used in section 6, in clause (23FE) of section 10 and various agreements entered into under section 90 or section 90A of the Act. Hence, it is proposed to insert clause (29A) to section 2 of the Act providing its definition. The term ―liable to tax in relation to a person means that there is a liability of tax on that person under the law of any country and will include a case where subsequent to imposition of such tax liability, an exemption has been provided.

Widening of the scope for taxability.

24. Rationalisation of the provision relating to processing of returned income and issuance of notice u/s 143(1) & (2) of the Act [w.e.f. AY 2021-22]

143(1)(a)(iv): Increase in income in the intimation on basis of audit report filed

143(1): Reduction in time limit for sending intimation from 1 year to 9 months from end of FY in which the return was furnished (i.e. 31st December after end of said FY)

143(2): Reduction in time limit for issue of notice from 6 months to 3 months from end of FY in which the return was furnished (i.e. 30th June after end of said FY)

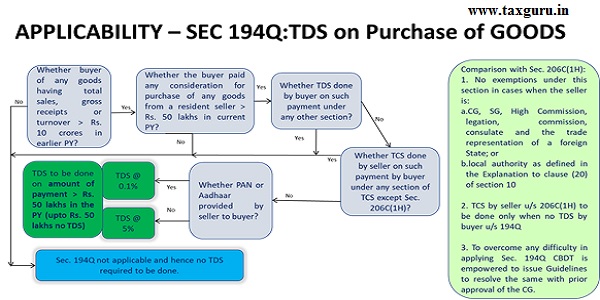

25. Tax Deduction at Source (TDS) on purchase of goods [w.e.f. 1st July, 2021]

Points to Ponder: Mirror provision of Sec. 206C(1H)

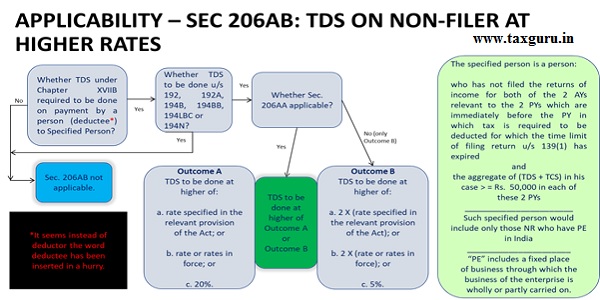

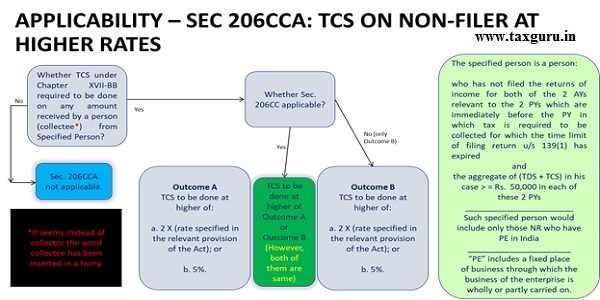

26. TDS/TCS on non-filer at higher rates [w.e.f. 1st July, 2021]

Points to Ponder:

- For almost 1st and 2nd Quarter of the in which TDS/ TCS to be done of the relevant FY, the 2 PYs would be different than PYs covered under the 3rd and 4th Quarters for identifying the persons non-compliance of ITR filing?

- How the deductor/ collector would come to know whether the deductee/ collectee have filed ITRs in the last 2 PYs?

- Also, how the deductor/ collector would come to know the aggregate of limit of TDS+TCS of the deductee/ collectee for last 2 PYs?

27. Taxability of Interest on various funds where income is exempt [w.e.f. AY 2022-23]

| Section | Nature of Exemption u/s 10 | Exemption not available in respect of |

| Sec. 10(11) | exemption with respect to any payment from a provident fund to which the Provident Funds Act, 1925 (19 of 1925) applies or from any other provident fund set up by the CG | Interest accrued during the PY in the account of a person to the extent it relates to amount or aggregate of amounts of contribution made by that person > Rs. 2,50,000 in any PY in that fund* |

| Sec. 10(12) | exemption with respect to the accumulated balance due and becoming payable to an employee participating in a recognised provident fund |

*This means maximum contribution to such funds against which interest income of which would be exempt can be Rs. 2,50,000/- in that PY. Interest on any contribution above this amount would attract tax liability. However, such interest would be computed as prescribed.

Disclaimer: This document has been prepared on the basis of information available in the public domain and is intended for guidance purposes only. We have taken reasonable care to ensure that the information in this document is accurate. It, however, accepts no legal responsibility for any consequential incidents that may arise from errors or omissions contained in this document. Also, all the information, contents, opinions and resources whatsoever provided in this article cannot be construed as tendering of professional legal advice. Interested parties are strongly advised to examine their precise requirements for themselves, form their own judgments and seek appropriate professional advice.

Author Bio