ICAI has further requested CBDT to extend time for submission of Tax Audit Reports and related returns from 30th September, 2018 to 31st October, 2018 as CBDT has not followed Norms of Earlier Years of discussing Important Changes in Tax Audit Report with ICAI, there was Constant changes in Utilities relating to Tax Audit Forms, Delay in release of utilities and there were Issue in utility of ITR Form No. 5.

ICAI has made a Similar Representation earlier on 31.08.2018 which can be accessed at the following link- Extend Tax Audit Due Date to 31st October, 2018: ICAI

ICAI has made its thirs representation on 17.09.2018, which can be accessed at the following link – Extend due date to submit Tax Audit Reports & ITR: ICAI

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

(Set up by an Act of Parliament)

ICAI/DTC/2018-19/Rep – 34

10th September, 2018

Shri Sushil Chandra Ji,

Chairman,

Central Board of Direct Taxes,

Ministry of Finance,

Government of India,

North Block,

New Delhi-110 001.

Respected Sir,

Further submissions: Reg. our representation dated 31st August, 2018 for extension of time for submission of Tax Audit Reports and related returns from 30th September, 2018 to 31st October, 2018.

This has a reference to the representation no. ICAI/DTC/2018-19/Rep — 27 dated 31st August,2018 submitted to your good office with a request for extension of time for submission of Tax Audit Reports and related returns from 30th September, 2018 to 31st October, 2018.

As you are kindly aware that ‘ICAI, being a partner in nation building, has always tried to strengthen the relationship between the taxpayers and the Department by placing before your good office, the difficulties being faced by assessees in respect of matters relating to direct taxes for appropriate solution. In view of the same, members have raised their concerns which were enumerated in the aforementioned representation.

In addition, to our above submissions, please kindly consider further submissions as follows:

Page Contents

1. Norm followed in earlier years:

It is pertinent to mention that in the year 2006-07 when the tax audit report was revised through Notification No. 208/2006 dated 10,8.2006, the same was made effective prospectively for AY 2007-08 and not retrospectively. Intact, in the AY 2006-07, despite of applicability of new forms prospectively, the due date of filing tax audit reports and their corresponding ITR were extended to 30th November, 2006. Similar approach should have been adopted this time also.

2. Constant changes in Utilities relating to Tax Audit Forms:

Continuous and regular updations are being made to the utility of Form No. 3CA/3CD and 3CB/3CD. Recently, the department has released/amended the utility of Form No. 3CB on 7th September 2018. Due to the frequent changes in the utilities, tax payers are facing difficulties in filing their tax audit reports efficiently as they need time to digest the changes. Such changes are causing further time consumption on the part of members.

Further, the changes made in the utility on 1st September, 2018 in Clause No. 9(a) of Form No. 3CB, there is a requirement of mentioning the details of the partners of the firm, which is a mandatory field. The present utility does not allow the assessee to enter any data in this field and the field is locked, inspite of the status of the assessee selected as partnership firm. Kindly refer to the representation no. ICAI/DTC/2018- 19/Rep – 32 dated 07th September,2018 highlighting the same. There has been no further update in this matter and the partnership firm’s auditors are not able to complete their audits due to this error.

The relevant screenshot of the error is as below:

3. Delay in release of utilities:

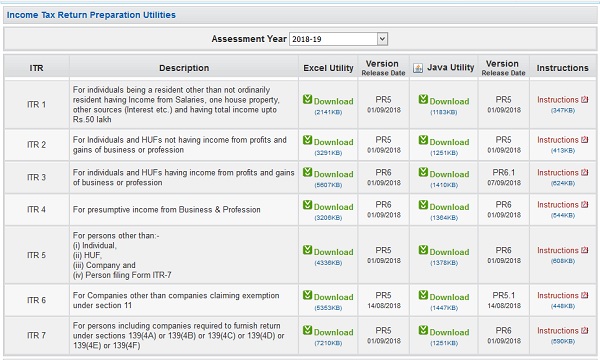

Due to the delay in e-enabling of return forms, the effective time available for filing of return of income became very less, causing genuine hardship to the assessees and members of the profession. The table below shows the effective time available for filing return of income/tax audit report(TAR) of A.Y.2018-19 whose last date for filing return of income/TAR falls due on 30th September, 2018:

S. No. |

ITR Forms/ TAR |

Time

|

Date of Notification |

Date of enabling E-Filing |

Delay in release of

|

Effective time available for filing of return of income/ TAR (from the date of

|

Numb er of

|

Last modified date |

| 1 | ITR 3 |

days | 03.04.2018 | 18.05.20 18 | 48 days |

135 days | 5 | 07.09.2 018 |

| 2 | ITR 5 & 7 | 183 days | 03.04.2018 | 21.05.20 18 | 51 days |

132 days | 5 | 01.09.2 018 |

| 3 | ITR 6 | 183 days | 03.04.2018 | 26.05.20 18 | 56 days |

127 days | 4 | 14.08.1 8 |

| 4 | Form 3CA,3CB, 3CD | 183 days | 20.07.2018 | 20.08.20 18 | 143 days | 40 days | 5 | 07.09.2 018 |

The relevant screenshots of ITR Forms & Form 3CD utilities updation are as under:

The main cause of concern for our members is that they need sufficient time to discharge all their professional obligations in an effective manner. It is also to be noted that whenever there is a schema change and the release of new utility by the CBDT, it requires time to understand the changes made in comparison to the earlier version. It is also seen that whenever the new utility is released, there are issues specially relating to the blocking of the mandatory fields for reporting, resulting in delay for completion of audit (Refer Point-2 for blocking of Clause 9(a) field).

Many assessees and auditors are using the softwares which are prepared by the software providers, based on the schema released by the CBDT. The software vendors take almost around a week’s time to update the software after the schema is released, due to which the working days get reduced.

More particularly, it is also our concern that the quality of audit conducted by them should not be compromised in any manner due to lack of sufficient time.

4. Issue in utility of ITR Form No. 5:

At present, the utility of ITR Form No. 5 is computing the late fee under Section 234F of the Income-tax Act, 1961 which is actually not leviable/applicable, since the return is filed within the time specified under the provisions of Section 139(1) of the Income-tax Act, 1961. Kindly refer to the representation no. ICAI/DTC/2018-19/Rep – 31 dated 07th September,2018 highlighting the same issue.

The relevant screenshot of the error is as below:

Reiteration of Suggestion:

In view of the above reasons and the reasons stated in our earlier representation, we suggest and request that the due date of filing returns of income under section 139(1) of the Income-tax Act, 1961 for assessees mentioned under clause (a) of Explanation 2 to section 139(1) and also the ‘specified date’ for filing tax audit reports be extended from 30th September, 2018 to 31st October, 2018 for AY 2018-19 as also the due date for filing tax audit reports.

We reiterate our request to grant an appointment to the undersigned as per your convenience to enable us elaborate our viewpoints.

We hope that our concerns would be favourably considered.

Yours faithfully,

-Sd‑

Chairman, Direct Taxes Committee

The Institute of Chartered Accountants of India

Ease of doing business – different java for Income tax dsc, ROC, GST. Different emsigner for GST, Income Tax returns, ROC, TDS filing. With all above difficulties its duty of government to extend date of filing of Income Tax returns to 31st dec. Instead of asking seperate Annual return form 9 and GST Audit Report, TAR, Company Audit Report – Incorporate all clauses in common form and ask us to file single AUDIT Report

Where we are moving, instead of doing ease of business daily new amendments, new forms, no proper website to know at one place all recent changes, our FM complicated gst, dsc regn problems, where we are moving. Instead of complicated Tax audit report ask client to load complete set of books as soft copy, allocate on random basis to CA and get report. It’s duty of government to give sufficient time for TAR and returns.

Sir plz extend the date of balance sheet 17-18 year

Dear sir please announce to extend date 31st Oct today because it’s difficult to finalize gst reconciliation

In earlier years due dates were divided According to the entities eg.July,October and December.It was easy to comply with the law and now computerisation has eased but the compliances have been increased along with the accountability in the same proportion but the time given is too less .Perhaps it’s expected to commit mistakes and punish the assessees for those mistakes alongwith the professionals.Are we heading towards development or dictator ship ?

Dear Sir,

All these years proper compliance was done regarding outreach. Since GST has been introduced which is consuming lot of time hence request to extend the return date

Sir please please extend the date from 30 Sep to 31 Oct because it very difficult to finalize books due to gst please annonced extended date today

SIR

WE REQUEST YOU KINDLY EXTENDED THE DUE DATE OF TAX AUDIT AND 2A ITC DEALINE FOR THE FY 2017-18

Because due to busy sheduled we are unable to reconcile gstr-2a with 3b and not able to close the books of account of manu client due to statutry complence of all indirect tax old and new audit as well as direct tax

pls extend Tax audit date To 31/10/2018

sir.date nhai badi to mere job bhe chout jaygi aur due salary bhe nhi melegi mera car.chopat ho jayga

sir. pl.new tax audit du date 15-11-2018

Dear sir please extend the date from 30th Sep to 31st Oct and please announce early

The due dates for all the compliances have left very little time for CA to complete audits and finalization on time. It is necessary to extend the due date. And the extension has to come well before the other due dates.

Hope the finance ministry hears soon.

Dear sir please extend the date for tax audit and please announce asap

The due date for non audit cases was extended to August 31st 2018 Similarly the due dates for audit cases to be extended to December 31st 2018. This will restore the position to what it was on the introduction of the common previous year from AY 1989-90.See then Section 139(1). There will be no such petitions year after year. . If department wants to account the taxes early,amend the Act and delink filing of returns from audit.

Please extend the due date & announce it as earliest as possible.

pls extend Tax audit date To 31/10/2018

We CAs should be bold enough to exert our right as Citizens of India, I have seen all responses pleading please, please, please….to CBDT.

CBDT should suo-moto monitor the situation and grant extension, rather than waiting till 28th. September and multiple representations from ICAI and its members to take the decision to sign a 100 word notification extending the date for 44AB and consequent return filing.

I have also never seen any assessee pleading for extension. Once extension is granted, those very client of ours would postpone their auditing and again we would be burning our midnight oil in last week of October or Novemeber or December whatever the extension may be.

It is disgusting to see self esteem of CA community down the drain in front of clients as well as CBDT.

Thanks to all for being extend of filling of Tax Audit date. As we are facing much of problems due to GST. Now we will get some more time to file the return in a frequant manner.

Thanks again to all.

Tax Audit & Return date extend necessary by reasaon in changes GST return i.e. 3 B ,GST R1 and TRAN 1 & 2 again open for filling ,Annual Retrun date delcare so tax audit date 31.10.18

Pl extend the due date of Tax Audit till 30th November as no of articled clerks with CA’s will go on leave for CA Exams which is to be held till Nov 18. Also compliances are more and presently performance of income tax portal is pathetic. Govt’s policy are like they are treating tax payers as CHOOR & BEWAKOOF. Very pathetic Govt

pls extend tax audit date to 31/10/18

Please Please extend to tax audit date to 31st October’2018

Till 31st August professional were occupied in firling ITR of non tax audit assessees, and now occupied in DIR – 3 KYC forms, making followups from DSC reseller and assessee. Unfortunately DSC servers are also facing traffic on server and they are facing difficulty for downloading the DSC. Penalty has also been increased in MCA forms as well as ITRs. Kindly consider request of ICAI on behalf of all professionals.

no need to again mention about various reasons why we need extention.

extention is needed other wise it is impossible to follow due date.

i feel that the extention shall be upto 30.11 or 31.12

Please Extend the Due Date of Tax Audit Report From 30-09-2018 to 31-10-2018.

Due to GST Reconciliation lot of time spend in this month

please extend the tax audit date and for non audit also remove points related to expenses breakup of Registered, Unreg etc

Please Extend tax audit due date up to 31/10/2018

It is the rights of practitioner that they required additional minimum 1 months for tax audit and filing of IT return with quality in timely.Dear FM please extended date of audit with one month and also extend GSTR-1 return up to 30.11.2018.

Jaipal Nunani

Advocate

It must be extended as it is not possible to complete with in the due date. Till 31.08.2018 professionals are busy in filing personal returns.

CA fraternity has always stood by the Govt in Tax compliance issues. The Govt should also understand the difficulties of the Professionals and the pressure we under go during Tax Audit period. PLEASE EXTEND THE DATE TO 31.10.2018 AND IMPORTANTLY ANNOUNCE THE SAME WELL IN ADVANCE PLEASE !

please extend itr and tax audit date to 31.10.2018

thanks

Please extend the due date of Tax Audit and ITR as early as possible

Please extend Tax Audit date.

Dear SIR, TAX GURU IS ALWAYS REALLY PERFORMING VERY NICE ,UPDATE,PRECAUTIONARY,STEPS FOR THE GENUINE DIFFICULTIES OF ASSESSEES & tAX PRACTICENERS FROM LONG YEARS. THANKS HEARTILY.HOPE FOR DEPT.TO REVERT EARLY,FOR SOLVING GENUINE HARDSHIPS,AS STATED IN NUMEROUS REPRESENTATIONS FROM DIFFERENT CORNERS OF FORUMS.THAKING YOU,

Sincerely request you to extend due dates for filing Tax Audit Report & Income Tax Return from 30th September 2018 to 31st October 2018.

IT IS VERY NECESSARY TO GIVE THE TIME FOR THE VERIFICATION OF STATEMENT OF ACCOUNT, we were compelled to give time to file the income tax return of the assesses up to august, therefore please extend the time for audit

The board must have to think about extension of date because there are numerous compliance in the hand of CA. So one month is not sufficient to file ITR and audit because we were engaged in ITR till August.

if at all the CBDT is convinced to extend the time till 31st Octobter 2018 for 44AB and other auditable cases including trusts, firms, companies, etc., the CBDT should do and inform the public with in a day or two, latest by 15th of September 2018,otherwise there won’t be any meaning in extending on 30th of September extending upto 31st october 2018, when by that time almost all would have by hook or crook completed the work, leave alone the quality of audit work. PLEASE INFORM BEFORE 15TH OF SEPTEMBER 2018.

Yes, The same proceedure should be adopted as earlier.Due date should be extended to 31st october.

Yes Please date should be extended

Dear Sir,

Please extend date upto 31.10.2018 as early as possible

PLEASE EXTEND TAX AUDIT DUE DATE

pls extend tax audit due date 31.10.2018

Dear sir please extend the date as institute requested twice for this. We need extension very badly. Please extend the date today or by tomorrow so that we file gst without any tension. Do the needful.

Dear Sir,

I am an Accountant. I am also facing the problem due to GST. So please extend the due date of TAX AUDIT of AY 2018-2019 from 30.09.2018 to 31.10.18, Your early action will be highly appreciated. Thanks

Please Extend tax audit due date up to 31/10/2018

sir,

Due to the implementation of new indirect tax law , and changes made in I.T. Statutory forms , we are requesting the CBDT to extend the Tax Audit due date for the F.Y. 2017-18 till 31st October 2018 . after the implementation of GST Act this is the first Tax Audit

Please extend to tax audit date

IT IS THE NECESSITY OF TAX PROFESSIONALS TO WORK WITH ZEAL AND ENTHUSIASM.

pls extend Tax audit date To 31/10/2018