ICAI has further requested CBDT to extend time for submission of Tax Audit Reports and related returns from 30th September, 2018 to 31st October, 2018 as CBDT has not followed Norms of Earlier Years of discussing Important Changes in Tax Audit Report with ICAI, there was Constant changes in Utilities relating to Tax Audit Forms, Delay in release of utilities and there were Issue in utility of ITR Form No. 5.

ICAI has made a Similar Representation earlier on 31.08.2018 which can be accessed at the following link- Extend Tax Audit Due Date to 31st October, 2018: ICAI

ICAI has made its thirs representation on 17.09.2018, which can be accessed at the following link – Extend due date to submit Tax Audit Reports & ITR: ICAI

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

(Set up by an Act of Parliament)

ICAI/DTC/2018-19/Rep – 34

10th September, 2018

Shri Sushil Chandra Ji,

Chairman,

Central Board of Direct Taxes,

Ministry of Finance,

Government of India,

North Block,

New Delhi-110 001.

Respected Sir,

Further submissions: Reg. our representation dated 31st August, 2018 for extension of time for submission of Tax Audit Reports and related returns from 30th September, 2018 to 31st October, 2018.

This has a reference to the representation no. ICAI/DTC/2018-19/Rep — 27 dated 31st August,2018 submitted to your good office with a request for extension of time for submission of Tax Audit Reports and related returns from 30th September, 2018 to 31st October, 2018.

As you are kindly aware that ‘ICAI, being a partner in nation building, has always tried to strengthen the relationship between the taxpayers and the Department by placing before your good office, the difficulties being faced by assessees in respect of matters relating to direct taxes for appropriate solution. In view of the same, members have raised their concerns which were enumerated in the aforementioned representation.

In addition, to our above submissions, please kindly consider further submissions as follows:

Page Contents

1. Norm followed in earlier years:

It is pertinent to mention that in the year 2006-07 when the tax audit report was revised through Notification No. 208/2006 dated 10,8.2006, the same was made effective prospectively for AY 2007-08 and not retrospectively. Intact, in the AY 2006-07, despite of applicability of new forms prospectively, the due date of filing tax audit reports and their corresponding ITR were extended to 30th November, 2006. Similar approach should have been adopted this time also.

2. Constant changes in Utilities relating to Tax Audit Forms:

Continuous and regular updations are being made to the utility of Form No. 3CA/3CD and 3CB/3CD. Recently, the department has released/amended the utility of Form No. 3CB on 7th September 2018. Due to the frequent changes in the utilities, tax payers are facing difficulties in filing their tax audit reports efficiently as they need time to digest the changes. Such changes are causing further time consumption on the part of members.

Further, the changes made in the utility on 1st September, 2018 in Clause No. 9(a) of Form No. 3CB, there is a requirement of mentioning the details of the partners of the firm, which is a mandatory field. The present utility does not allow the assessee to enter any data in this field and the field is locked, inspite of the status of the assessee selected as partnership firm. Kindly refer to the representation no. ICAI/DTC/2018- 19/Rep – 32 dated 07th September,2018 highlighting the same. There has been no further update in this matter and the partnership firm’s auditors are not able to complete their audits due to this error.

The relevant screenshot of the error is as below:

3. Delay in release of utilities:

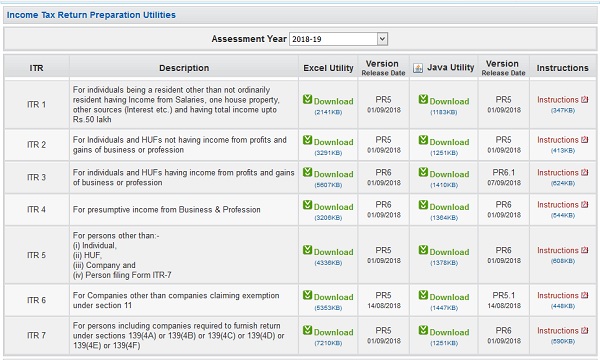

Due to the delay in e-enabling of return forms, the effective time available for filing of return of income became very less, causing genuine hardship to the assessees and members of the profession. The table below shows the effective time available for filing return of income/tax audit report(TAR) of A.Y.2018-19 whose last date for filing return of income/TAR falls due on 30th September, 2018:

S. No. |

ITR Forms/ TAR |

Time

|

Date of Notification |

Date of enabling E-Filing |

Delay in release of

|

Effective time available for filing of return of income/ TAR (from the date of

|

Numb er of

|

Last modified date |

| 1 | ITR 3 |

days | 03.04.2018 | 18.05.20 18 | 48 days |

135 days | 5 | 07.09.2 018 |

| 2 | ITR 5 & 7 | 183 days | 03.04.2018 | 21.05.20 18 | 51 days |

132 days | 5 | 01.09.2 018 |

| 3 | ITR 6 | 183 days | 03.04.2018 | 26.05.20 18 | 56 days |

127 days | 4 | 14.08.1 8 |

| 4 | Form 3CA,3CB, 3CD | 183 days | 20.07.2018 | 20.08.20 18 | 143 days | 40 days | 5 | 07.09.2 018 |

The relevant screenshots of ITR Forms & Form 3CD utilities updation are as under:

The main cause of concern for our members is that they need sufficient time to discharge all their professional obligations in an effective manner. It is also to be noted that whenever there is a schema change and the release of new utility by the CBDT, it requires time to understand the changes made in comparison to the earlier version. It is also seen that whenever the new utility is released, there are issues specially relating to the blocking of the mandatory fields for reporting, resulting in delay for completion of audit (Refer Point-2 for blocking of Clause 9(a) field).

Many assessees and auditors are using the softwares which are prepared by the software providers, based on the schema released by the CBDT. The software vendors take almost around a week’s time to update the software after the schema is released, due to which the working days get reduced.

More particularly, it is also our concern that the quality of audit conducted by them should not be compromised in any manner due to lack of sufficient time.

4. Issue in utility of ITR Form No. 5:

At present, the utility of ITR Form No. 5 is computing the late fee under Section 234F of the Income-tax Act, 1961 which is actually not leviable/applicable, since the return is filed within the time specified under the provisions of Section 139(1) of the Income-tax Act, 1961. Kindly refer to the representation no. ICAI/DTC/2018-19/Rep – 31 dated 07th September,2018 highlighting the same issue.

The relevant screenshot of the error is as below:

Reiteration of Suggestion:

In view of the above reasons and the reasons stated in our earlier representation, we suggest and request that the due date of filing returns of income under section 139(1) of the Income-tax Act, 1961 for assessees mentioned under clause (a) of Explanation 2 to section 139(1) and also the ‘specified date’ for filing tax audit reports be extended from 30th September, 2018 to 31st October, 2018 for AY 2018-19 as also the due date for filing tax audit reports.

We reiterate our request to grant an appointment to the undersigned as per your convenience to enable us elaborate our viewpoints.

We hope that our concerns would be favourably considered.

Yours faithfully,

-Sd‑

Chairman, Direct Taxes Committee

The Institute of Chartered Accountants of India

Should ICAI not go to the shelter of Court to explain their problems, extension for further due date as 30.11.2018 ?

Plz extend the date of filling tax audit report for Ac. year 2018-19

Respected Sir,

With humbly and respectively I informing to Good Office that in A & N Islands area was poor net work due Cyclone & in schedule rainy season.

So, requested that extension the time for IT & Tax Audit filing.

Thanking you,

Your obdiently

Sir, Kindly extension due date to 31st oct 2018, due to First year GST Implementation

Dear Sir.

Please extend the due of Tax audit AT 2018-19 up to 31.10.2018….Because we are totally uncontrollable so please extend due date as soon as possible….Thank You.