CA Gourav Goyal

Brief about Employee Stock Option Plan (ESOP)

Employee Stock Option Plan (ESOP) is a frequently used incentive mechanism used by organizations. There are various reasons for which the employees of a company are given such stock options. The phenomena of stock options is more prevalent in start-up companies which cannot afford to pay huge salaries to its employees but are willing to share the future prosperity of the company. In such cases the employees are given the stock options as part of the compensation package.

It is a common practice among organizations to reward performing employees by giving ESOPs as a part of the salary and ensure long-term commitment of the employee. It aims at improving the performance of the company, increasing the value of the shares by involving stock holders, who are also the employees, in the working of the Company and further, ESOPs help in minimizing problems related to incentives. However, one must also analyze the tax implications of ESOPs for employee as well as the company.

Page Contents

- A. Introduction to Employee Stock Option Plan (ESOP)

- B. Objective of issuing ESOPs

- C. Eligibility for ESOP

- D. Requirement for Employee Stock Option scheme (ESOP)

- I. Sanction by Special Resolution

- II. Employees to whom ESOPs may be issued

- III. Disclosures in the explanatory statement annexed to the notice for passing of the resolution

- IV. Pricing

- V. Shareholders’ approval by way of separate resolution

- VI. Variation of terms of ESOP

- VII. Minimum vesting period

- VIII. Lock-in-period for shares issued on exercise of option

- IX. Right to receive dividends

- X. Forfeiture/ Refund of amount paid by employees at the time of grant of option under ESOP

- XI. Options not transferable

- XII. Who can exercise the option

- XIII. Disclosures in Board of Directors Report

- XIV. Register of Employees Stock Options

- E. Valuation of ESOPs

- F. Taxation Implications of ESOP

- G. Conclusion

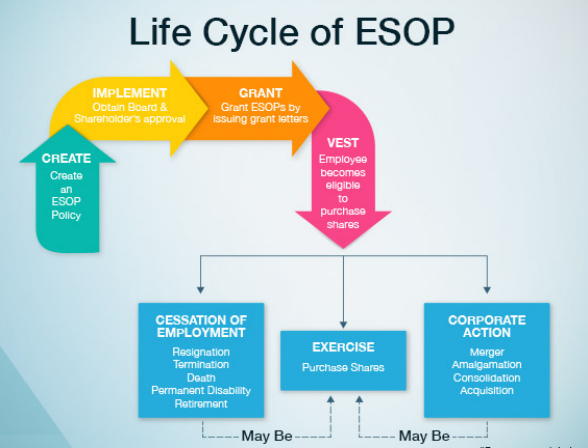

A. Introduction to Employee Stock Option Plan (ESOP)

The idea that employees should have an ownership stake in the company led to the emergence of concept of Employee Stock Option Plan (ESOP). Definition of “Employee Stock Option” was first incorporated by way of a clause (15A) in Section 2 of the Companies Act, 1956, based on the recommendations of Working Group. Section 62 of the Companies Act, 2013 further incorporates enabling provision for the issue of ESOPs subject to the sanction of special resolution and compliance with Rules (in case of unlisted public company) and SEBI Regulations (in case of listed companies). Let us discuss the compliances for an unlisted company in detail.

ESOPs

The Employee Stock Option Plan (ESOP) or Employee Stock Option Scheme (ESOS) is the option or a right which is being offered by a company to its employees to purchase its shares at a pre-determined price in the future. ESOP is not an obligation rather it is a right of the employee to purchase certain amount of share of the company at a pre decided price.

ESOP is basically a tool used by a company to retain its employees and get them awarded for being associated with the company. As a part of an employee’s compensation ESOP creates a sense of ownership in the mind of employees and their interest in the organization remains intact. ESOP plays a vital role to attract employees at the growing stage of the company.

Sec 2(37) of Companies Act, 2013 defines “employees stock option” which means, ‘the option given to the directors, officers or employees of the company or of its holding company or subsidiary company or companies, if any, which gives such directors, officers or employees, the benefit or right to purchase, or to subscribe for, the shares of the company at a future date at a pre-determined price.’ This provision needs to be read with Rule 12 of The Companies (Share Capital and Debentures) Rules, 2014.

B. Objective of issuing ESOPs

B. Objective of issuing ESOPs

The objective of issuing ESOP is to:

- Provide incentive to attract, retain and reward employees of the company

- Motivate employees to contribute to the growth and profitability of the company

Important Terms:

- Option: a right but not an obligation– to purchase the shares of the company on the fulfillment of the conditions mentioned in the ESOP plan at the price decided at the time of grant of options.

- Grant: The eligibility of a particular employee (depending on the criteria set) for grant of stock options based on his role and performance is known as grant of option

- Vesting: It is the entitlement of the option to an employee.Before exercise of the option, the employee has to wait for a limited period as a condition of ESOP grant.

- Exercise:The activity of converting the options granted to an employee into shares by paying the required exercise price, i.e., allotment. The companies have freedom to determine the exercise price in conformity with the applicable accounting policies, if any.

The effective date of exercise is the date on which the Company allots the shares.

C. Eligibility for ESOP

C. Eligibility for ESOP

Approval of shareholders

- Private Companies : To offer ESOP, approval of shareholders by way of ordinary resolution is required. (Notification dated 5th June, 2015).

- Listed Companies: Rule 12(11) specifically provides that where the equity Shares of the Company are listed, the ESOP shall be issued as per the SEBI Regulations.

- Other than the Private Companies ( i.e., Unlisted Public Companies): Approval of shareholders by way of special resolution is required as per Sec 62(1)(b) of Companies Act, 2013, read with Rule 12 of The Companies (Share Capital and Debentures) Rules, 2014.

D. Requirement for Employee Stock Option scheme (ESOP)

I. Sanction by Special Resolution

The issue of Employee Stock Option scheme shall be approved by the shareholders of the company, by passing a Special Resolution.

II. Employees to whom ESOPs may be issued

For the purpose of the Section 62(1)(b) and Rule 12, “Employee” means –

a. A permanent employee of the company who has been working in India or outside India; or

b. A director of the company, whether a whole time director or not but excluding an independent director; or

c. An employee as defined in clause (a) or (b) of a subsidiary, in India or outside India, or of a holding company of the company or of an associate company, but does not include-

i. An employee who is a promoter or a person belonging to the promoter group; or

ii. A director who either himself or through his relative or through any corporate, directly or indirectly, holds more than 10% of the outstanding equity shares of the company.

However, in order to promote startups, the Ministry of Corporate Affairs vide Notification dated 19.07.2016 issued the Companies (Share Capital and Debentures) Third Amendment Rules, 2016 wherein it was provided that Startups may issue the shares under ESOP to their promoters and directors who hold more than 10% for the first 5 years from the date of their incorporation. The restriction on issuing shares under ESOP to promoters and such directors continues for companies which does not fall under the category of startups.

III. Disclosures in the explanatory statement annexed to the notice for passing of the resolution

The company shall make the following disclosures in the explanatory statement annexed to the notice for passing of the resolution:

- the total number of stock options to be granted;

- identification of classes of employees entitled to participate in the Employees Stock Option Scheme;

- the appraisal process for determining the eligibility of employees to the Employees Stock Option Scheme;

- the requirements of vesting, period of vesting and the maximum period within which the options shall be vested;

- Exercise Price/Pricing Formula/Exercise Period/Method of valuation;

- the Lock-in period, if any;

- the maximum number of options to be granted per employee and in aggregate;

- the method which the company shall use to value its options;

- the conditions under which option vested in employees may lapse e.g. in case of termination of employment for misconduct;

- the specified time period within which the employee shall exercise the vested options in the event of a proposed termination of employment or resignation of employee;

- a statement to the effect that the company shall comply with the applicable accounting standards.

IV. Pricing

The companies granting option to its employees pursuant to Employees Stock Option Scheme will have the freedom to determine the exercise price in conformity with the applicable accounting policies, if any.

The approval of shareholders by way of separate resolution shall be obtained by the company in case of:

- grant of option to employees of subsidiary or holding company; or

- grant of option to identified employees, during any one year, equal to or exceeding one percent of the issued capital (excluding outstanding warrants and conversions) of the company at the time of grant of option.

VI. Variation of terms of ESOP

The company may by special resolution, vary the terms of Employees Stock Option Scheme not yet exercised by the employees provided such variation is not prejudicial to the interests of the option holders. The notice for passing special resolution for variation of terms of Employees Stock Option Scheme shall disclose full details of the variation, the rationale therefore, and the details of the employees who are beneficiaries of such variation.

VII. Minimum vesting period

There shall be a minimum period of one year between the grant of options and vesting of option. In a case where options are granted by a company under its Employees Stock Option Scheme in lieu of options held by the same person under an Employees Stock Option Scheme in another company, which has merged or amalgamated with the first mentioned company, the period during which the options granted by the merging or amalgamating company were held by him shall be adjusted against the minimum vesting period required under this clause.

The company shall have the freedom to specify the lock-in period for the shares issued pursuant to exercise of option.

IX. Right to receive dividends

The Employees shall not have right to receive any dividend or to vote or in any manner enjoy the benefits of a shareholder in respect of option granted to them, till shares are issued on exercise of option.

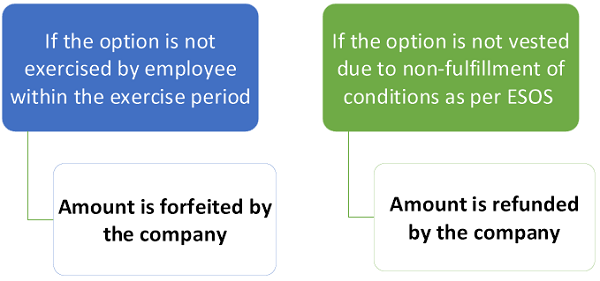

X. Forfeiture/ Refund of amount paid by employees at the time of grant of option under ESOP

XI. Options not transferable

XI. Options not transferable

- The option granted to employees shall not be transferable to any other person.

- The option granted to the employees shall not be pledged, hypothecated, mortgaged or otherwise encumbered or alienated in any other manner.

XII. Who can exercise the option

- No person other than the employees to whom the option is granted shall be entitled to exercise the option. However, in the event of the death of employee while in employment, all the options granted to him till such date shall vest in the legal heirs or nominees of the deceased employee.

- In case the employee suffers a permanent incapacity while in employment, all the options granted to him as on the date of permanent incapacitation, shall vest in him on that day.

- In the event of resignation or termination of employment, all options not vested in the employee as on that day shall expire. However, the employee can exercise the options granted to him which are vested within the period specified in this behalf, subject to the terms and conditions under the scheme granting such options as approved by the Board.

XIII. Disclosures in Board of Directors Report

The Board of directors, shall, inter alia, disclose in the Directors’ Report for the year, the following details of the Employees Stock Option Scheme:

- Options granted/ vested/ exercised;

- The total number of shares arising as a result of exercise of option;

- Options lapsed;

- The exercise price;

- Variation of terms of options;

- Money realized by exercise of options;

- Total number of options in force;

- Employee wise details of options granted to;-

(i) key managerial personnel;

(ii) any other employee who receives a grant of options in any one year of option amounting to five percent or more of options granted during that year.

(iii) identified employees who were granted option, during any one year, equal to or exceeding one percent of the issued capital (excluding outstanding warrants and conversions) of the company at the time of grant;

XIV. Register of Employees Stock Options

- The company shall maintain a Register of Employee Stock Options in Form No. SH.6 and shall forthwith enter therein the particulars of option granted under clause (b) of sub-section (1) of section 62.

- The Register of Employee Stock Options shall be maintained at the registered office of the company or such other place as the Board may decide.

- The entries in the register shall be authenticated by the company secretary of the company or by any other person authorized by the Board for the purpose.

E. Valuation of ESOPs

- Valuation:

At the time of grant of option, valuation of fair value of shares shall be done by registered valuer. At the time of exercise of option, valuation shall be done by Merchant banker.

- Valuation of ESOP in case of Unlisted Companies:

Fair value of shares at the time of “grant of Option” and “exercise of option” shall be done by registered valuer as per “Guidance note on accounting for employee share-based payment” (issued 2005). Income Tax Act, 1961 does not specify any method for computation of FMV of shares but Section 17 and Rule3(8) of the Act provides that for the purpose of perquisite valuation the FMV of ESOP shall be such value as determined by a merchant banker on the specified date.

“Specified Date” means the date of exercising of the option; or any date earlier than the date of the exercising of the option, not being a date which is more than 180 days earlier than the date of the exercising.

F. Taxation Implications of ESOP

A) For the Employee

There are no cash outflows or taxation implications when the options are granted as and when the options are vested in the employee.

The Income Tax Act, 1961 has laid down the following two stages of taxation for employees in respect of shares allotted to them under an ESOP.

- Stage 1 (Perquisites)– Upon allotment of shares after the employee exercises his option on the completion of the vesting period. Upon allotment of shares, the employer will have to compute the perquisite value of ESOP taxable in the hands of the employee under “income from salary” and deduct tax on such ESOP. The perquisite value and the tax deducted thereon by the company would be reflected in Form 16 and Form 12BA of the employee and treated as income from salary in the tax return.

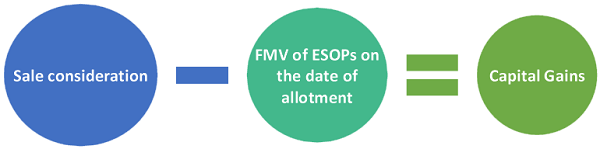

- Stage 2 (Capital Gains)– When the shares allotted to the employee are sold by him. If the company is listed on an Indian stock exchange and shares are held for more than 12 months, it will be considered as long-term capital gain and as per Finance Act 2018, it will be taxed u/s 112A at 10% exceeding Rs. 1 lakh of CG. If shares are held for less than 12 months, it will be considered as short-term capital gain and profit will be taxed at 15% u/s 111A.

Today, employees in start-ups and unlisted companies are also allotted ESOPs. These shares will be considered short-term assets if held for less than 24 months from the exercise date and taxed according to the respective tax slab. If the shares are held for more than 24 months, and sold after this period, these are considered as long-term gains and taxed at 20% after indexation of cost.

In case the employee chooses to not exercise his option, there shall be no tax implication for the employee.

B) For the Company

The Issuing Company can claim ESOP cost as deduction.

The discounts under the ESOP are an employee cost and should be allowed as a deduction over the vesting period, in the hands of the issuing company.

Furthermore, there may also be a situation when ESOP-shares are bought back by the Company.

When it comes to a buyback of shares of an unlisted company, then provisions under sections 10(34A) and 115QA of the Income Tax Act shall intervene.

As per section 10(34A), any income arising to a shareholder (including ESOP-shares) on account of buy back of unlisted shares by the company shall be exempt in the hands of such shareholder. Further, as per section 115QA, the tax @ 20% shall be paid by the unlisted company on the buyback of its shares.

Therefore, in the hands of the employees, the gain from the buyback of shares by an unlisted company shall be exempt and the company shall be liable to pay buyback distribution tax.

It is to be noted that if the employee sells ESOP-shcares to a third party instead of the company, then he shall be liable to pay capital gain tax and the company need not pay any taxes, as the transaction happened between an employee and the purchaser.

G. Conclusion

Undoubtedly, the ESOPs are a prevalent method used by companies to attract, motivate and retain employees. This tool of ESOPs have two fold benefit i.e. reducing cash outflow and retaining deserving employees for their growth. Employees also see this scheme as a long term investment for which they have to compensate with their cash perquisites and bonuses. Since many companies have now made ESOPs as part of the compensation for key employees, it is very important for an employee to be aware of its taxability. ESOPs are beneficial to both employees as well as Startups if implemented effectively. The sense of ownership acts as a motivation for the employees to work hard and diligently.

About the Author

Author is Gourav Goyal, FCA having expertise to develop high quality business strategies and plan ensuring alignment with short-term and long-term objectives of Foreign Companies. He has gained rich experience with expertise in the areas of Consultancy to Foreign companies, Non Resident Indians and Joint Ventures including work relating to FEMA matters, RBI and FIPB He is associated as “Director – India Entry Strategy” with Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm established in the year 1997 with its head office at New Delhi and can be reached at info@neerajbhagat.com.

ADMN / Author>” Income Tax Act, 1961 does not specify any method for computation of FMV of shares but Section 17 and Rule3(8) of the Act provides that for the purpose of perquisite valuation the FMV of ESOP shall be such value as determined by a merchant banker on the specified date.”

Do you think/opine that this, by any logic or sane/acceptable reasoning, could be taken to be applicable to RSU in holding company, provided to employee of any group / subsidiary company”?!

Your answer is required for me to suitably cover in my proposed Article to be sent to you as indicated y’day !

“E. Valuation of ESOPs”

Read more at: https://taxguru.in/income-tax/employee-stock-option-plan-unlisted-company.html?

As per my readining and perception , no mention has been made about the mandatory requirement of issue of a Notification in terms of sec 17, so as take ‘market -value’ or – quotation / ‘FMV’ for the purpose of reckonong the perqisite value for taxation/TDS. And me gather that no such Notification , to one’s knowledge, has been made. This is a point of no less relevance to ‘RSU’ as well. Without such a Notification , by virtue of the SC Judment in Srinivasa’a case, on that only ground alone, TDS by employer could be strongly objected to, with every chance of success !

Any view to share, to the contrary ?!

My recent comments , wrt the published Article / itat Order in HDFC Dubai based employee’s case should be of guidance !

courtesy

Hi

Can you please give your thoughts on below given query. As per Guidance note on ESOP, Company has to take valuation report at the time of granting of ESOPs. What if Company has not taken any valuation report and time limit of 180 days ahead of grant date also got expired?

Thank you

A comprehensive information that gives insights and a better perspective. Seeking your expert opinion and clarifications:

1. An unlisted company rolled out an ESOP scheme for the top management in 2015. A 10 rupee share price at Rs.750/share. Granted 1% over a period of four years at 0.25% each year. Shared the letters of offer every year.

2. Received a letter in March 2020 mentioned it as a Notice to terminate e ESOP.

If ESOP not yet granted, Do we need to disclose it in the List of Shareholders.

Hi. In my case

– Holding company (transferor) is acquired by subsidiary company (operational) for which appointed date is 01 April 2019 and effective date is 27th April 2020

– Holding company had issued ESOP’s in 2018-19

and first tranche was exercised in Nov 2019 i.e. after appointed date and before effective date

– ESOP scheme will be carried forward by subsidiary company (transferee)

Q1 – What will the impact on financial statements as on 31 March 2020.

Q2 – The Transferee Company shall issue and allot its shares to equity shareholders of the Transferor Company such that the entire equity share capital of the Transferee Company will be issued and allotted to the equity shareholders of the Transferor Company in proportion of their respective equity shareholding in the Transferor Company, as determined under the scheme. Since this will happen on 01 April 2019, what will happen to ESOP? do we have to increase the authorised capital to adjust the shares issued under ESOP?

Dear Sir,

As per the law, under ESOP, a company have the freedom to determine the exercise price of shares. But can a company issue such shares at a price lower than the face value of shares.

Dear Neeraj,

Thanks a lot for this article it gave me a good clarity on ESOP.

I just have a few clarifications in the below scenario.

if the Parent company who allotted ESOP is foreign entity

and they have Indian Subsidy . ESOP is been awarded to employee working in Indian subsidy

.

Before merger and Acquisition , if the Employee has exercised 20 % of the ESOP and rest of the 80% ESOP was not exercised.

but the parent company before merger has initiated request to pay cash for renouncement of the 80% ESOP accoording to current FMV.

What is the tax implication of the cash paid for the employee for renouncement of the share ?

In your earier response you have mentioned that

“Options not exercised by employee and the same was sold to the company itself as on Exercise date:

Difference of Sale Value and the exercise price will be considered as Capital Gain in the hands of employee”

Will renoucement of share is same as selling the share back to the company and will it be taxed has capital gains even thought it was not exercised or

will it be taxed has regular salary income ?

I read the perquisite is always taxed in same slab has salary income even thought employee not getting monetary benefit until sale ?

Is there anyway to defer tax on the perquisite ?

What will be your advise on how to find right CA to handle these kind of situations ?

Regards,

Kumar

Hi kumar – Did you ever find an answer to your question. I am in the same boat right now. Parent usa company has been bought and esop plan terminated with compensation paid out . What did finally happen in your case

If the company is unlisted foreign company. Stock option sale within 24 months is considered capital gain. Can I setoff against short term capital loss from sale of shares?

I had a question:

On the exercise date, does the beneficiary have to apply to the company for the Valuation Report?

Dear Sir

Are there any restrictions Under the CA2013 for a Pvt company to give its shares (trfd by the promoter) to its employees, as part of retention plan?

Dear Sir,

As mentioned above, valuation of Unlisted Company Shares is to be done by a Registered Valuer. Can it be done by a chartered Accountant also? Request you to please throw some light on this.

Thank you.

Dear SIr,

Can a private company funding its ESOP Trust provide interest free loan without passing any resolution to that effect. Based on the premise that Section 67 is not applicable to Private Company, pls advise ?

Does buyback / cancellation of vested (but not exercised) ESOP units by unlisted company (due to a change in control event) also fall under perview of 115QA and 10(34A)? I believe the sections apply to shares including “ESOP-shares” but not quite sure if ESOP (vested units) and ESOP-shares is one and the same thing. Any guidance would be much appreciated!

Did you ever find an answer to your question. I am in the same boat right now. Parent usa company has been bought and esop plan terminated with compensation paid out .

Dear Neeraj,

My ESOP has been vested and my company wants to close/cancel (not converted or brought shares) the ESOP and pay the employees. The company has recently bee acquired and therefore the closing of the ESOP and payout is happening. now since the company is unlisted the company will need to pay 20% and employee will be exempted from tax or how will it work for the employee on tax?

The New ITR-2 (2019) for has field in the “General” tab asking if we have held unlisted shares (and the details) in the FY for which returns are filed.

Do we have to count ESPP/ESOP of MNCs (listed outside India) in this (just the way we do for CG on those foriegn shares) ?

The doubt cropped up since unlike the CG section this one clearly wants us to identify the company as being ‘foriegn’ or ‘Indian’.

Dear Neeraj,

Thanks for really good article on ESOP taxation.

If I am allotted stocks of an MNC company not listed in India, do I need to declared them as foreign assets in ITR2?

Thanks

Saurabh Jain

Dear Mr. Girish,

I hope this article helped you.

Regarding your Query, If the parent company grant options to employee of subsidiary than the impact will be as under:

a) Options not exercised by employee and the same was sold to the company itself as on Exercise date:

Difference of Sale Value and the exercise price will be considered as Capital Gain in the hands of employee.

b) Option Exercised by employee

i. At the time of exercise: Difference of fair market value as on date of exercise and exercise price will be taxable as Perquisite in the hands of employee and employer needs to deduct TDS accordingly.

ii. At the time of sale of shares: Difference of Sale price and fair market value as on date of exercise will be taxable as Capital Gain in the hands of employee.

Further, please note that in Case-b above, Employee needs to intimate the details of ESOP to RBI through Authorised Dealer Bank.

Dear Sir,

Thank you. This is wonderful article on ESOP with details.

I need a clarification on :- if the Parent company who allotted ESOP is foreign country and where they have a office in India and where this employee is working in India. How the taxability to employer (in India ) and employee for India will arise? What legal compliance care India employer ands employee should take?