Department of finance has introduced a new return on April 29, 2022. The New return is known as ITR-U. What is meant by ITR-U? When will an Assesse can file ITR-U? Details are the Following;-

(1) Idea of ‘ updated return‘ has been introduced in the Finance Act 2022. As per newly introduced Section 139(8A) of the Income- Tax, an Assesse can ‘update‘ his/her Income-Tax return within 2 years (option available)

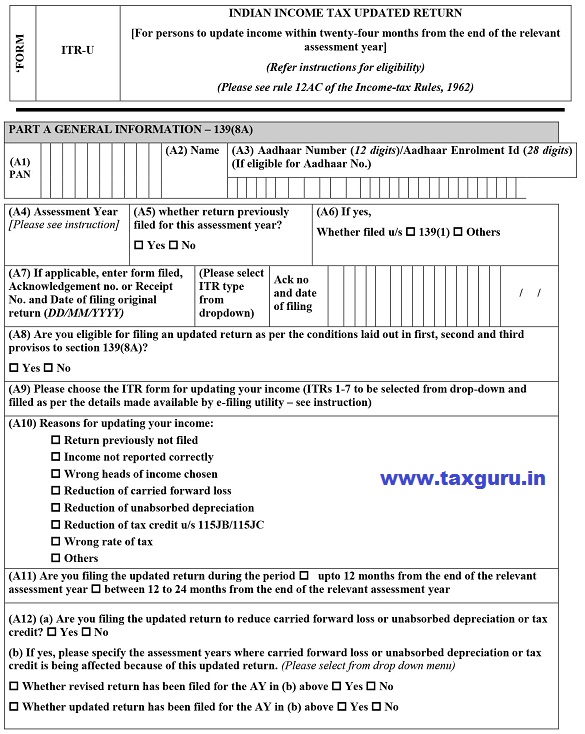

For Example: you can update Income Tax of the Assessment year 2022-23 up to 31/3/2025. You can file only one updated return in a single assessment year.

(2) Following are the reasons to file updated returns as per April 29, notification.

(a) Income Tax return has not been filed previously

(b) Recording Income as Incorrect

(c )You have selected wrong heads of Income

(d) Reducing the carried-forward loss, depreciation as per the previous return

(e) Reducing Income Tax credit as per Sec 115 JB/ 115 JC

(f) Selecting correct tax slabs.

(g) Others.

(3) You cannot file updated returns under the following Circumstances

(a) To get Refund

(b) To reduce the Income Tax liability at previous returns

(c )When facing the proceedings of the Income-Tax Department.

(4) Following are the additional taxes applicable

(a) If updated return files before 12 months from the end of the relevant assessment year- 25% of tax is to be remitted as additional income tax

(b) If updated return files after 12 months from the end of the relevant assessment year but before 24 months from the end of the relevant assessment year- 50% of the tax is to be remitted as additional income tax.

(5) You can only use the Electronic verification methods and Digital Signatures for the verification

(6) Now, you can file updated return in the Income-Tax website.

Part A of ITR-U

Author Bio