Case Law Details

Indian Renewable Energy Development Agency Ltd Vs PCIT (Delhi High Court)

In a recent ruling, the Delhi High Court addressed a writ petition with substantive prayers seeking relief for the petitioner against the notice dated 19.07.2018 issued by Respondent No.1. The petitioner sought the quashing of the notice aiming to revive time-barred assessment proceedings for the assessment years 1998-99 to 2009-10. The court was urged to declare the pending proceedings as barred by limitation, direct the acceptance of the petitioner’s returned income, and grant a stay on the operation of the impugned notice.

The court had initially issued a notice on 08.08.2018, permitting the respondents/revenue to proceed with the assessment order but with a condition not to enforce it. Additionally, no coercive action was to be taken against the petitioner.

The core contention of the petitioner was rooted in the expiration of the limitation under Section 153(2)(A)/153(3) of the Income Tax Act, 1961. The petitioner argued that, following orders from the Income Tax Appellate Tribunal, the Assessing Officer (AO) lacked jurisdiction to pass a fresh assessment order.

To provide context, the petitioner had filed returns for Assessment Year (AY) 1998-99 to AY 2009-10, which were subjected to scrutiny, leading to separate assessment orders under Section 143(3) of the Act.

The court’s order on appeals in 2011 set aside certain orders, remanding the matter to the Tribunal for fresh consideration. Subsequent orders in 2014 and 2015 further directed the AO to reevaluate the assessments for multiple years.

Despite notices issued by the AO, the petitioner contended that, due to the expiration of limitation, the AO could not proceed with a fresh assessment order. This stance was communicated in responses to notices in 2016, emphasizing the limitation issue and presenting the petitioner’s position on merits.

In response to the petitioner’s non-compliance, the AO issued a notice on 19.07.2018, prompting the petitioner to move the court through the writ petition. The central question before the court was whether the limitation for fresh assessment orders had expired.

On 02.02.2023, the court sought information on whether any assessment orders had been passed. The court was informed that, despite the opportunity granted, no assessment orders had been issued by the AO.

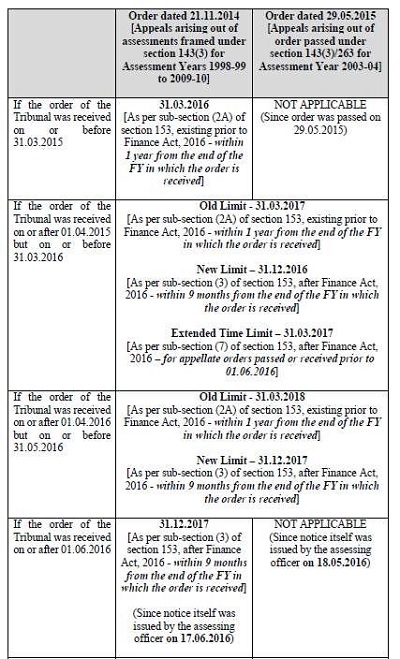

The court noted the amendments to Section 153 of the Act and, based on the provided table, highlighted the significance of dates concerning the Tribunal’s orders and their service to the petitioner.

Considering both the old provision (Section 153(2)(A)) and the amended provision (Section 153(3)), the court concluded that, as of the present date, the AO lacked jurisdiction to pass assessment orders. Consequently, the prayers in the writ petition were allowed, and the assessment proceedings were deemed time-barred.

The court directed the AO to accept the returned income for the specified assessment years, leading to the disposal of the writ petition. The interim order dated 08.08.2018 was vacated in light of the court’s decision.

FULL TEXT OF THE JUDGMENT/ORDER OF DELHI HIGH COURT

1. The substantive prayers made in the writ petition read as follows:

“(A) issue a writ in the nature of mandamus/ certiorari or any other appropriate writ, order or direction quashing the impugned notice dated 19.07.2018 issued by Respondent No.1, seeking to revive/ re- initiate/ continue the already time-barred set-aside assessment proceedings in the case of the Petitioner for assessment years 1998-99 to 2009-10, as void ab initio and patently illegal;

(B) declare the pending set-aside assessment proceedings for assessment years 1998-99 to 2009-10 in the case of Petitioner, pursuant to the appellate orders of the Tribunal dated 21.11.2014 and 29.05.2015, as barred by limitation in terms of section 153 of the Act;

(C) issue a writ in the nature of mandamus or any other appropriate writ, order or direction directing the Respondents to accept the returned income of the Petitioner for assessment years 1998-99 to 2009-10 and consequently determine and process, the tax payable and/or refund due, if any, to the Petitioner;

(D) grant ad-interim ex-parte stay on the operation of the impugned notice dated 19.07.2018 issued by Respondent No.1 and all consequential set-aside assessment proceedings in the case of the Petitioner for assessment years 1998-99 to 2009-10 during the pendency of the present petition.”

2. The record shows that notice in this writ petition was issued by a coordinate bench on 08.08.2018. While issuing notice, the court permitted the respondents/revenue to proceed and pass an assessment order, with the condition that they would not give effect to it.

2.1 Furthermore, the court indicated that no coercive action would be taken against the petitioner.

3. The principal reason why the petitioner has approached this court is that since limitation under Section 153(2)(A)/153(3) of the Income Tax Act, 1961 [in short, “the Act”] had expired pursuant to the orders passed by the Income Tax Appellate Tribunal [in short, “Tribunal”], the Assessing Officer (AO) had been emasculated of the jurisdiction to pass a fresh assessment order.

4. To adjudicate the issue etched out hereinabove, the following broad facts must be noticed:

(i) The petitioner had filed its return for Assessment Year (AY) 1998-99 to AY 2009-10 under Section 139 of the Act. The petitioner was subjected to scrutiny concerning the above-mentioned AYs, and accordingly separate assessment orders were framed under Section 143(3) of the Act.

5. The record discloses that insofar as AY 1998-99 to AY 2002-03 were concerned, the matters were carried in appeal by the revenue on certain aspects to this court. This court passed a combined order dated 21.10.2011 concerning appeals preferred vis-a-vis the AYs referred to hereinabove.

5.1 Via the said order, the court set aside the impugned orders and remanded the matter to the Tribunal for a fresh consideration. Upon remand by this court, the Tribunal via order dated 21.11.2014 in turn remitted the matter to the AO, not only concerning AY 1998-99 to AY 2002-03, but also for AY 2003-04 to AY 2009-10.

6. The record further discloses that the Tribunal via yet another order dated 29.05.2015, remanded the matter to the AO for AY 2003-04 with regard to two issues. The AO was directed to pass a fresh assessment order having regard to the remand order. It is important to note that in this order, the Tribunal was dealing with the appeal effect order passed under Section 143(3)/263 of the Act.

7. This started the process of the AO engaging with the petitioner with regard to completion of proceedings. Notices were issued, to which responses were furnished by the petitioner. The first notice was issued by the AO pursuant to the Tribunal’s order dated 29.05.2015, on 18.05.2016. Insofar as the remand order dated 21.11.2014 is concerned, the AO issued a notice on 17.06.2016 concerning AY 1998-99.

7.1 Since limitation had expired, the petitioner while responding to the notices in and about 2016, also took the stand that the AO could not now proceed to pass a fresh assessment order. This is evident upon perusal of communication dated 15.07.2016. Pertinently, this communication not only raised a specific objection with regard to expiration of limitation, but also projected the petitioner’s stand on merits.

7.2. It is in this context that on 28.06.2018, the petitioner approached the AO that its returned income should be accepted and accordingly refund should be granted.

8. The AO, on the other hand, on 19.07.2018 issued a notice to the petitioner for being represented by an authorised representative on 07.2018, to answer the queries with respect to the AYs in issue, i.e., AY 1998-99 to AY 2009-10. The petitioner was also directed to produce the relevant documents/accounts and other evidence in support of its stand.

9. The issuance of this notice propelled the petitioner to address communications dated 25.07.2018 and 02.08.2018 to the AO. In these communications, the petitioner took the stand that the limitation for passing assessment order had expired.

9.1 Since the AO did not drop the proceedings and accepted the income as declared by the petitioner in its return, the petitioner was constrained to move this court by way of the instant writ petition. As noted right at the outset, the writ petition came up for hearing before this court on 08.08.2018. Pursuant to notice being issued, a counter-affidavit was filed by the respondents/revenue. The record shows that the petitioner filed a rejoinder to the counter-affidavit.

10. As indicated above, the central point which arises for consideration in the present writ petition is: Whether limitation for passing fresh assessment order(s) in consonance with aforementioned order of the Tribunal had expired?

11. Having regard to the aforesaid circumstances, on 02.02.2023, we had asked Mr Abhishek Maratha, learned senior standing counsel, to return with instructions as to whether any assessment order(s) had been passed pursuant to the order dated 08.08.2018 passed by the coordinate bench. Time for this purpose was granted on 26.05.2023 and 18.08.2023.

12. Mr Maratha informs us that he is instructed to convey to the court that no assessment order(s) had been passed by the AO, despite an opportunity being given by the court via order dated 08.08.2018.

13. We may note that the earlier avatar of Section 153 of the Act was Section 153(2A). It is also relevant to note that Section 153 of the Act was amended via Finance Act, 2016 with retrospective effect, i.e., from 01.06.2016.

14. Having regard to the amendments made to the aforesaid provisions, the petitioner has adverted to the following table, which is incorporated in its written submissions:

15. Significantly, the counter-affidavit filed on behalf of the respondents/revenue, does not indicate the dates of which add „of‟ the orders dated 21.11.2014 and 29.05.2015 passed by the Tribunal were served on the petitioner.

16. As would be evident, the best scenario for the respondents/revenue would be if the order of the Tribunal was served on or after 01.04.2016, but on or before 31.05.2016. It is not in dispute that as per Section 153(2)(A) [which is the old provision], the limitation would expire on 31.03.2018. However, if the amended provision, i.e., Section 153(3) of the Act were to be taken into account, the limitation would expire on 31.03.2017. It is also not disputed that this aspect of the matter is covered by the judgments of the coordinate bench rendered in Nokia India (P.) Ltd. v. Deputy Commissioner of Income-tax, [2017] 291 Taxman 85 (Delhi) and Aricent Technologies (Holdings) Ltd. v. Assistant Commissioner of Income Tax & Anr., 2023/DHC/001521.

17. Thus, whichever regime we take into account, i.e., the time limit fixed as per Section 153(2)(A) of the Act or the time limit fixed by the amended provision i.e., Section 153(3) of the Act, as of today the AO is bereft of jurisdiction and hence, would have no legal locus to pass assessment order(s). Therefore, the prayers made in the writ petition are allowed.

18. The assessment proceedings concerning AY 1998-99 to AY 2009-10, pursuant to the orders of the Tribunal dated 21.11.2014 and 29.05.2015, have become time-barred. The AO is thus directed to accept the return income lodged by the petitioner for the aforementioned AYs. Resultantly, the return as available on record will be processed and consequential orders would be passed.

19. The writ petition is disposed of in terms of the aforesaid directions.

20. Accordingly, the interim order dated 08.08.2018, which was made absolute on 09.08.2019, shall stand vacated.