1. Concept of PE – Introduction

1. PE is primarily a concept relevant from tax treaty perspective. Under a treaty regime, business profits are ordinarily taxable in the country of residence except when there exists a PE in source country.

2. Article 5(1) U.N. Model Tax Convention and OECD Model Convention– Basic rule PE “a fixed place of business, through which the business of an enterprise is wholly or partly carried on.”

3. For example, A Inc. is an US company engaged in manufacturing industrial equipment and exporting to various countries including India. The income which A Inc. earns from India can be taxed only if A Inc. has a permanent establishment in India.

4. This division of rights i.e. a correct and fair allocation of profits to the PE in the host country is imperative. This will ensure that the tax authorities, especially of a developing nation, are not apprehensive of erosion of their fair share of taxes.

2. Service PE – Key Aspects

It is to be noted that Article 5(3)(b) of the UN Model differs from OECD Model regarding Service PE. OECD Model does not include a Service PE clause; however, a suggested Service PE clause is included in the OECD Commentary on Article 5.

– First inserted in the U.N. Model Tax Convention in 1980.

Article 5(3) of the UN Model (2017 update)

(b) The furnishing of services, including consultancy services, by an enterprise through employees or other personnel engaged by the enterprise for such purpose, but only if activities of that nature continue within a Contracting State for a period or periods aggregating more than 183 days in any 12-month period commencing or ending in the fiscal year concerned.”

Service PE is formed if the following conditions are satisfied:

- Furnished within a source state.

- Furnished by Foreign Enterprise through employees or other personnel.

- Period of furnishing services increase the specified threshold limit.

Some Key Concepts to be Considered

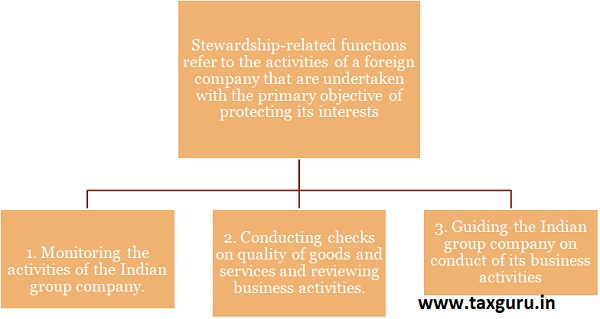

1. Stewardship – related activity

> The stewardship related activities of a foreign company in India should not constitute its Service PE. [Case of Morgan Stanley (SC) discussed later].

2. Secondment/Deputation of Employees

Secondment means deputation of employees by a foreign company to its Indian group company, based on the latter’s requirements. They work under the control and supervision of Indian Entity.

- Tekmark Global Solutions – worked under control & supervision of Indian Co. and carried out work allocated to them by Indian Co. and FE is reimbursed the salary of deputed employees (Service PE – not created).

- Morgan Stanley/ Teradata Operations – FE retains lien over it (Service PE – created)

- Centrica India Offshore – services rendered on behalf of foreign company (Service PE – created).

⇒ Services in the nature of ‘fees for technical services’

1. Some of India’s tax treaties mandate that a Service PE cannot be constituted in India when services provided by foreign companies and the consideration received qualify as FTS or FIS.

2. This is a measure to ensure minimal levy of tax on such transactions in order to attract technical experts to India from abroad.

3. However, where the tenure of such employees in India is for a long duration, a fixed place PE may be constituted in the country, depending on the nature of activities undertaken in it.

⇒ Other Personnel

1. Service PE can be constituted if services are provided by “other personnel” who are not a company’s employees, but are under the control and supervision of a foreign company.

2. In the case of e-Funds IT Solutions, the Supreme Court interpreted the term “other personnel” to mean persons (other than employees) engaged or appointed by a foreign company.

3. Similarly, in the case of Lucent Technologies, Delhi HC observed that the term “other personnel” refers to persons over whom the foreign company has a certain degree of control.

3. Interpretation of Service PE clause in UN Model/Indian Treaties

Interpretation of “Services furnished within the source state”

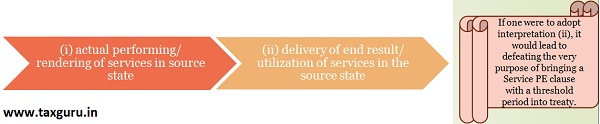

As per Art. 5(3) UN MTC – a threshold period for formation of a PE, indicates the meaning intended for the word ‘furnishing’, i.e., being the actual performance of services in the source state.

As per OECD commentary – emphasized upon ‘performance’ of services in the source state as a necessary ingredient for formation of Service PE.

However, a contrary view was taken by Bengaluru Trib. (ABB-FZ-LLC) where it held that a UAE company (‘the taxpayer’) had a Service PE in India since the tax payer has been furnishing services to the Indian company even without any substantial physical presence of its employees in India (in this case the physical presence of employee was only 25 days in the previous year).

Test of Duration of ‘furnishing of services’

4. Service PE vis-à-vis Domestic Tax Law

It is generally a basic presumption that in most cases where revenues are earned from services rendered in India (and the same is not characterized as FTS under the Act or Treaty), a business connection under the Act (Sec. 9) exist.

“BC” is the Indian equivalent of PE. It is much wider in connotation and has been very effectively used by the revenue authorities to tax the income of non-residents in India.

Despite being referred to in the ITA, the term was not defined till the Finance Act, 2003 which inserted a explanation to Section 9 of the Indian Income Tax Act, 1961.

Section 92F(iiia) , includes a fixed place of business through which the business of the enterprise is wholly or partly carried on

- CBDT Circular No. 14/2001-Income Tax dated 09.11.2001 explaining the provisions of Finance Act 2001, states that the term PE has not been defined in the Act, but its meaning may be understood with reference to treaty entered into by India.

- Finance Act 2002 introduced definition of PE in Sec.92F. Circular No. 8 of 2002 explaining the provisions of Finance Act 2002 states that a separate definition of ‘permanent establishment’ on the lines of the definition found in tax treaties entered into by India with other countries have been provided.

- PE definition under the Act has been vaguely dealt with by the Supreme Court in case of Morgan Stanley. wherein it states that the intention in adopting an inclusive definition of PE so as to cover Service PE, Agency PE, Construction PE etc.

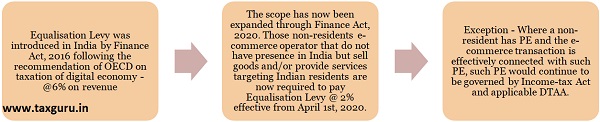

5. Equalisation Levy vis-à-vis Service PE

In re Master Card (2014) – AAR ruled that Indian operations of MasterCard has resulted into formation of fixed place, dependent agent PE & Service PE in India under Indo-Singapore DTAA. Aggrieved by the ruling of AAR, MasterCard has filed writ petition before Delhi High Court.

While the decision of the Hon’ble Delhi High Court is pending, introduction of 2% Equalisation Levy has landed MasterCard between a rock and a hard place.

The assessees, engaged in providing services which attracts Equalisation Levy, would always be under a predicament that whether Equalisation Levy is payable or not in cases where there is a possible litigation on existence of PE.

The difficulty assumes further importance in the light of the fact that there is no specific provision in the Finance Act which provides for either refund of Equalisation Levy or adjustment against the income-tax liability by way of credit in a case where Equalisation Levy has already been paid and the existence of PE is established.

6. Impact of Covid-19 on creation of Service PE in India

> Due to COVID-19, many employees who were seconded to India have been stuck in India due to travel ban as per Government directions. Whether extending stay of seconded employees not by choice but by compulsion would cause creation of PE of such foreign company in India is a matter require special consideration.

- OECD’s Approach – In view of the special circumstances, wherein there is forced stay of people who may continue to render services in a State (other than the State of usual residence), ideally no PE should be created.

– The concept of Force Majeure in case of a home office- a place being available to the foreign enterprise and management being ‘ordinarily’ exercised in case of PoEM have been discussed.

– Thus, the Covid situation is termed as exceptional and temporary and is not to be treated as a normal period.

- CBDT Circular – Vide Circular No. 11 dated 8-5-2020 has laid down certain parameters to exclude the number of days of stay in India between 22-3-2020 and 31-3-2020 in case it is occasioned by quarantine or suspension of international travel.

– The Circular also records that the objective is to provide relief to the persons who ‘intended’ to maintain status of non-resident but who are forced to become residents because the threshold is satisfied.

- Article 61 of the Vienna Convention on the Law of Treaties – provides that supervening impossibility of performance of a treaty may be a ground for suspension or withdrawal.

– Article 62 provides that a fundamental change in the circumstances not foreseen at the time of conclusion of the treaty may be invoked as a ground for suspension or withdrawal from the treaty in certain cases.

– However, the text of the treaty and the understanding of the parties will have precedence.

7. Conundrum of Physical Presence of Employees (Traditional Approach)

In 10th and 11th sessions, in 2014 and 2015 respectively, the U.N. Committee of Experts on International Cooperation in Tax Matters discussed about the physical presence of employees.

1. Majority View – the traditional interpretation of the Service P.E. requires the physical presence in the source country of individuals.

2. Minority View – emphasized the term “furnishing” as used under Article 5(3)(b) of the U.N. MTC and contended that the furnishing of services does not require a physical presence.

The U.N. Committee acknowledged that the growth of technology has made it possible to furnish services without any physical presence in the source country and, for that reason, did not reject outright the minority view. Rather, it asked the countries adopting the minority view to seek agreement through a mutual agreement procedure under Article 25.

In 2016, Saudi Arabia adopted the minority view and formally implemented guidelines to recognize the existence of a Service P.E. without the presence of employees in Saudi Arabia.

India’s Position – ABB FZ (discussed later), Tribunal observed that Article 5(2) of the India-U.A.E. tax treaty, which, inter-alia, includes the concept of Service P.E., broadens the scope of Article 5(1), which defines P.E. as a fixed place of business in the source country. Therefore, Article 5(2) was not a prerequisite to fulfilling the requirement of Article 5(1), as Article 5(2) is independent of Article 5(1) and the condition of fixed place of business is not attached.

8. Legal Precedents

1. DIT (International Taxation) v. Morgan Stanley & Co. [2007] 162 Taxman 165/292 ITR 416 (SC)

Facts of the case – MS & Co. was incorporated in the US. It was in the business of providing financial advisory services, corporate lending and securities underwriting services. MSCo was wholly owned subsidiary of Morgan Stanley, US. It was an investment bank and Morgan Stanley Advantage Services Private Limited (‘MSAS’) was incorporated and set up by the MSG in India, to support the group members’ front office functions in their global operations.

– Under the service agreement, Stewardship activities MSCo, like any other customer, had undertaken certain stewardship and similar activities. This was done for ensuring that MSAS achieved the overall global value benchmarks of the Morgan Stanley Group.

– Employees on Secondment / Deputation MSCo’s staff was also sent on deputation at the request of MSAS, to work under its control and supervision. It was agreed that the staff would continue to be employed or engaged and their salaries and fees would be directly paid by the MSCo. MSAS reimbursed the compensation cost to the MSCo with no profit element.

AAR Ruling – MSCo. sought advance ruling on whether it had a PE in India. The AAR ruled that the applicant would be regarded as having a PE if it sends some employees to India as stewards in the employment of the Indian company. Both the US Company and the Department preferred cross appeals before the Supreme Court.

SC Ruling – Court overruled the AAR decision as regards the Indian company being regarded as PE where the foreign company sends some of its employees as stewards. It explained the role of stewardship activities which is to ensure that the Indian staff adequately meet the requirements of foreign associate. The objective is to protect the interest of the foreign company and the stewards were not involved in day to day management.

However, the people sent on deputation by the Foreign Entity [MSCO] to Indian Entity [MSAS] constitute Service PE of the Foreign Entity.

2. DDIT v. M/s. Tekmark Global Solutions LLC [2010] 4 ITR(T) 1 (Mumbai Trib.)

Facts – The assessee, an American company, had an arrangement with an Indian company to depute its personnel to the Indian company on a hire-out basis. The personnel were to work under the direction, supervision and control of the Indian company. The assessee raised invoices on the Indian company to recover the salary paid by the assessee to the deputed personnel.

The Assessing Officer held that the said income directly accrued to the assessee in India through its employees who were provided to the Indian company and, hence, amount recovered by the assessee from the Indian company was taxable. The Commissioner (Appeals) held that the assessee did not have a permanent establishment in India and, accordingly, its business income was not taxable in India. Revenue appealed to ITAT.

Ruling – The assessee had provided was selecting and offering personnel to work under the control and supervision of the Indian company. It was not a part of any technical services to be rendered by the assessee to the Indian company.

– The deputed persons were for all practical purposes employees of the Indian company. They carried out work allotted to them by the Indian company. The assessee had no control over the activities or the work to be performed by the deputed persons. The Indian company had a right to remove the deputed persons from the service. What the assessee recovered was the actual salary payable to the deputed persons.

– When the services rendered were independent of and not under the control of the assessee, the deputed persons could not be considered as constituting a permanent establishment of the assessee in India. Hence, there was no PE of the assessee in India. The actual salary of the deputed personnel was also reimbursed by the Indian company.

3. Dy. DIT v. JC Bamford Excavators Ltd. [2014] 43 taxmann.com 283 (Delhi Tribunal)

Facts – JCB UK had entered into a Technology Transfer Agreement (TTA) with its Indian subsidiary JCB India. Consequently, it also executed an International Personnel Assignment Agreement (IPAA) with JCB India. The Tribunal noted that the expatriate employees being located in India can be segregated into two categories :

(i) technical consultants & employees in senior managerial positions of JCB India who were deputed on assignment basis, and

(ii) personnel visiting India occasionally for random quality standard testing of the products manufactured by JCB India under TTA framework.

Ruling – The Bench held that the (ii) category of employees were performing preparatory and auxiliary services which cannot constitute a PE as per article 5(3)(e) of the Treaty.

Considering the (i) category of employees, in the context of the conditions laid out article 5(2)(k) of the Treaty for creation of a Service PE. The key findings were as follows:

– managerial services were being rendered within India for more than 90 days (though the Treaty provides a threshold of 30 days in case of services rendered to Associated Enterprises)

– the services were not taxable under article 13 as Royalty or FTS since they were linked to a PE

– the employees who were seconded to JCB India, though being on the payroll of JCB India, were employees of JCB UK who were providing services in relation to the transfer of technology by JCB UK under the TTA read with the IPAA.

Based on the above findings, the Bench held that the first category of employees constituted a Service PE of JCB UK in India as that expatriate personnel on deputation continued to be employees of the foreign company and hence can constitute a Service PE.

4. Centrica India Offshore (P.) Ltd., In re [2014] 44 taxmann.com 300 (Delhi High Court)

Facts -A U.K. and Canada based company, engaged in business of supplying gas and electricity, outsourced their back office support functions such as consumers billings, debt collections, etc. to third party vendors in India.

In order to ensure quality, applicant company is established in India to act as service provider to overseas entities. Overseas entity provided staff with knowledge of its processes and practices. Since object of secondment for fixed terms is to train and familiarize staff in India so that once secondment ceases, staff in India can apply processes and practices.

Ruling – Since employees continue to be employees of overseas entities and their employer continue to be overseas entity, and seconded employees are rendering services for their employer in India by working for a specified period for a subsidiary or associate enterprise of their employer, this will give rise to a service PE within meaning of article 5.2(k) of India-UK Treaty.

– On a reading of the secondment agreement, it is seen that the right of the seconded employees to seek their salaries and other emoluments is against the overseas entity. They cannot claim it as of right against the applicant. The right of dismissal of the employees vests in or rests with the overseas entity.

To determine existence of a service PE, substance of the employment relationship should be looked at and not the form;

─ The employment relationship between the secondee and the overseas entity was at no point terminated and the Indian entity did not have the right to modify the same. The employment with the overseas entity was permanent as compared to that of the Indian entity;

─ The fact that the payment from Indian entity was termed as ‘reimbursement’ or was not subject to mark-up, was not determinative of the nature of payment. Once it was established that there was provision of service, the payment would be for service.

5. Asstt. DIT v. E-Funds IT Solution Inc. [2017] 251 TAXMAN 280/399 ITR 34 (SC)

Facts – In this case, an Indian company whose entire shareholdings were held by two foreign companies both directly and indirectly. The Indian company being 100% subsidiary of the foreign companies carried out the assignments given by the foreign companies. The factual matrix was that the Indian company was subjected to tax on the income earned in India as well as its global income in accordance with the provisions of the Act. The dispute was that the two foreign companies were also held as chargeable to tax in India for the income attributable to India for the reason that they had permanent establishment in India.

Assessee US companies were rendering different types of management and support services to customers located outside India. Their Indian subsidiary company was rendering support services which, in turn enabled assessees to render services to their clients abroad.

Ruling – Whether so far as service PE is concerned, requirement of article 5(2)(1) of DTAA is that an enterprise must furnish services within India and that such services are furnished through employees or other personnel. Since no customers of assessees were located in India or had received any services in India, merely because auxiliary operations that facilitated such services were carried out in India, first ingredient contained in article 5(2)(1) was not satisfied and, thus, it was not necessary to advert to other ground.

– On the role of deputed employees, the Apex Court noted in particular the observations of the High Court that the employees were deputed towards the development of domestic work in India.

– The deputed employees were working under the control and supervision of E-funds India and their remuneration was borne by E-funds India only. Based on the above, the Apex Court accepted the contentions of the Taxpayers that they had not created a Service PE in India.

6. ABB FZ-LLC v. DCIT (International Taxation), [2017] 83 taxmann.com 86 (Bengaluru Trib.)

Facts – ABB FZ was engaged in the business of providing regional services to a related party in India. The employees of the L.L.C. were present in India for 25 days, during which services were provided.

However, the employees continued to render services on a regular basis from the U.A.E. through emails, video conferencing, and other electronic modes for more than nine months within a 12-month period.

Ruling – The Tribunal determined that ABB FZ had a Service P.E. in the facts presented and held that the presence of employees is not required in the source country for a Service P.E. to exist.

– The Tribunal emphasized that it is not the presence of the employees that is important. Rather, it is the furnishing of services for more than the specified period of time (regardless of the place of performance) that determines whether the nonresident employer has a Service P.E. in India.

– The decision of the Tribunal implies that the place of performance of services is not relevant for determining the source of income. Rather it is the place of final consumption/utilization of such service that determines its source. Instead of an income tax, which compensates a service provider for its actions performed at the location where employees are based, the activity is subject to consumption tax, which is based on the place of consumption.

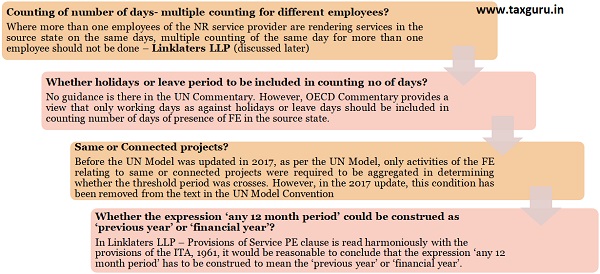

7. Linklaters v. Dy. DIT (IT) [2019] 106 taxmann.com 195 (Mum – Trib.)

Facts – The assessee, a partnership firm, was a tax resident of United Kingdom (UK) and was engaged in the practice of law. The assessee was appointed as legal advisor for some of the projects in India and provided legal consultancy services to them and received fees from the clients in India. However, the assessee filed its return declaring nil income contending that it had no Branch Office in India, the fee received was not chargeable to tax in India.

– The Assessing Officer noted that employees/other personnel of the assessee had rendered services in India for more than 90 days and, hence, the assessee had a PE in India in terms of article-5(2)(k)(i).

Ruling – The Tribunal observed that if the provisions of Service PE clause of the tax treaty is read harmoniously with the provisions of the Income-tax Act, 1961 (the Act), it would be fair and reasonable to conclude that the expression ‘any 12 month period’ has to be construed to mean the ‘previous year’ or ‘financial year’.

– The days of vacation availed by an employee who was in India should not be counted towards the threshold of 90 days to constitute a PE.

– Stay of employees in India on a particular day has to be taken cumulatively and not independently and multiple counting of employee in a single day is impermissible under article 5(2)(k)(i).

– Thus, the total number of days spent by the employees in India was 42 days. Therefore, in terms of Article-5(2)(k)(i) of the tax treaty, the taxpayer did not have PE in India during the year.

8. Teradata Operations Inc. v. DCIT [2020] 116 taxmann.com 404 (Delhi – Trib.)

Facts – Teradata Operations Inc. is a tax resident of the USA engaged in the business of providing data warehousing services. During FY 2013-14, the taxpayer rendered certain professional services and received royalty in respect of software licensed to its Indian group company, Teradata India Private Limited (TIPL).

The taxpayer also received reimbursement in respect of employees seconded to TIPL, which included:

─ Cost of seconded employees; and

─ Relocation expenses i.e. visa expenses and other travel costs.

The AO noted that there was a secondment agreement between the taxpayer and TIPL; and between the taxpayer and the seconded employees. However, there was no employment agreement between TIPL and the seconded employees. Further, the secondees continued to be employees of the taxpayer. Thus, Service PE arises. Aggrieved by this, Taxpayer appealed to ITAT.

Ruling – The ITAT in the current case noted that:

─ The taxpayer had seconded its employees to manage the affairs of TIPL and to provide technical knowledge;

─ The employees for all practical purposes remained employees of the taxpayer, even though they were stationed at TIPL’s premises;

─ The employees continued to make social security contributions in the USA and their salaries were distributed to their USA bank accounts;

─ There was no agreement between TIPL and the employees.

In view of the above, the ITAT upheld that the taxpayer had a PE in India as per the provisions of the India-USA tax treaty.

Author Bio

Excellent article, a comprehensive and concise guide to service PE, meticulously referencing law provisions and case laws!

Thanks and Regards,

CA. Shivam Agrawal