CA Vishrut Shah

In this article I have compared provision related to Depreciation & Amortization under Companies Act, 1956 and Companies Act, 2013. I have explained the same in tabular form, in simple manner for better understanding of readers-

| Sr. No. | Particulars | Position as per Companies Act,1956 | Position as per Companies Act,2013 |

| 1 | Governing Section | Section 205 & Section 350 | Section 123 |

| 2 | Concept | Rates of Depreciation | Useful Life of Asset |

| 3 | Method of Depreciation | Straight Line Method (SLM), Written Down Value Method (WDV) & Unit of Production Method (UPM) | Straight Line Method (SLM), Written Down Value Method (WDV) |

| 4 | Applicability on Tangible Assets | Rates are Prescribed | Useful life is prescribed[ Definition of Useful Life -Useful life is the period over which an asset is expected to be available for use by an entity, or the number of production or similar units expected to be obtained from the asset by the entity ] |

| 5 | Applicability on Intangible Assets | Rates are Prescribed | Nothing is Prescribed, Treatment as per Accounting Standard |

| 6 | Schedule mentioning Rates / Useful Life | Schedule XIV | Schedule II |

| 7 | Flexibility in Rates/ Useful Life | Companies have to follow the minimum rates prescribed under the schedule | Companies are allowed to follow Lower useful life of asset than prescribed subject to following conditions :(a) Disclosure of the said fact &(b)Technical Justification for selection of different useful life |

| 8 | Residual Value of Asset | There was no concept of residual value it was governed as per As – 6 | Maximum Residual Value of 5% is defined however companies have option to choose higher residual value subject to following conditions :

(a)Disclosure of the said fact & (b)Technical Justification for selection of different useful life |

| 9 | Component Accounting | There was no concept of Component Accounting | Component Accounting is voluntary for financial year starting from 01/04/2014 and it is compulsory from the financial year starting from 01/04/2015 [As per Notification issued by MCA on August 29, 2014][Meaning of Component Accounting –Companies will need to identify and depreciate significant components with different useful lives separately ] |

| 10 | Effect of More than Single Shift | Specific rates are prescribed for double and triple shift | It is mentioned that value of depreciation shall increase by 50% for no. of days working in double shift and by 100% for no. of days working in Triple shift |

| 11 | Depreciation of low value asset | 100% Depreciation need to be provided in the first year itself for asset having value less than 5000/- | Option is given to the management to decide materiality based on size of the company and accordingly 100% depreciation need to be provided for such value of assets subject to same fact need to be disclosed in as part of accounting policies |

| 12 | Amortisation of Intangible Assets | Revenue based Amortisation of all intangible assets | Amortisation will be done in accordance with Accounting Standard 26 |

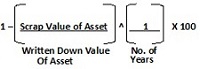

| 13 | Rates of Depreciation under SLM | As per the rates specified | Working shall be done in following manner : |

| 14 | Rates of Depreciation under WDV | As per the rates specified | Working shall be done in following manner : |

(Author can be reached at +91-9824798534 or on Vishrut1303@gmail.com)

Kindly Refer to

Privacy Policy &

Complete Terms of Use and Disclaimer.

Dear Mr. Dixit Ranka,

with respect to your quarries please find below answers :

1) Schedule and Act is silent on the matter but as per the Guidance Note issued by ICSI on Depreciation as per Schedule II of Companies Act,2013 it states that this is decision to be taken based on the materialism followed. So the decision to be take b y management to decide such limit and give justification for the same in notes to accounts.

2) Again Sir this depreciation formula is given in the guideline issued by ICSI only and hence the working is shown.

However the case you are referring of Zero residual value will never arise in reality as there can be at least some scrap value of anything. And second important thing is in order to keep residual value zero as per schedule II you need to give technical justification along with accounting justification in notes to accounts.

Dear Mr. Sujit Kumar Das & Mr. Shanker Chandak

You are correct sir it is typographical error from my side and sorry for the inconvenience.

The residual value as mentioned in point no.8 is Min 5% or it shall not be more than 5% of the asset.

Dear Vishrut,

I have two queries,

1) Could you please site the provision for depreciation of low value assets in Companies Act, 2013. (Provide from ACT)

2) As above mentioned formula for WDV rate, In this example if i take Scrap value as ZERO then depreciation rate will be 100%. Does this mean if assets do not have any scrap value then it should be 100% depreciated in the year of acquisition.

Regards

Dixit Ranka

HOW TO SAVE TAX MONEY

Dear Vishrut Shah

Your Serial No.8 for Co’s Act2013 speaks for Minimum Resudual Value of 5%. It should be Maximum Residual Value of 5%.

Otherwise it’s fine.

Regards

Sujit Kumar Das

9433036600