I. Introduction:

The Government of India along with the Ministry of Finance has widened the tax base. Which has resulted in bringing more and more compliance responsibilities on the companies. Companies must be aware that non-compliance with respect to certain high-value transactions might get them an Income Tax notice. The Income-tax department requires companies to submit a statement of Specified Financial Transactions (SFT). SFT reporting is mandatory for certain reporting entities from Finance Act 2014 by introducing section 285BA followed by additions made in Finance Act 2020 through notification no. 16/2021, dated 12-03-2021. This article focuses on SFT reporting which is applicable to the companies and documents require for reporting such transactions.

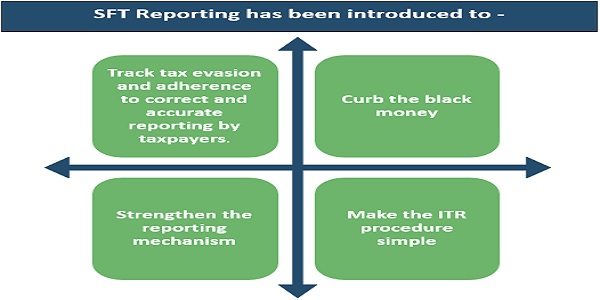

II. Why SFT has been introduced?

III. Nature & value of Reportable Transactions:

The below-mentioned table shows the nature of the transactions to be reported and documents require to file SFT:

| Reporting person | Nature of transactions | Threshold limit | Mandatory fields of SFT Return | Information Required for SFT Return |

| The company issuing Bonds or Debentures | Receipt from any person for acquiring bonds or debentures issued by the company or institution (other than renewal) | Rs. 10 lakh or more | Details of persons to whom Bonds or Debentures are issued:

Name, PAN, Aadhar, Email ID, complete Address, Pin code, mobile number, person type Details of Debentures issued: No. of debentures or bonds issued, issue price, face value, premium/ discount amount (if any). |

– PAN

– Aadhar – Address Proof – Form PAS 3 – Debentures or Bonds Subscription Agreement – Debenture/ Bonds issue certificate |

| The Company issuing shares | Receipt from any person for acquiring shares (including share application money) issued by the company | Rs. 10 lakh or more | Details of persons to whom shares are issued:

Name, PAN, Aadhar, Email ID, complete Address, Pin code, mobile number, person type Details of Shares issued: No. of shares issued, face value, issue price, premium amount (if any) |

– PAN

– Aadhar – Address Proof – Form PAS 3 – Shares subscription agreement – Share certificate |

| Reporting person | Nature of transactions | Threshold limit | Mandatory fields of SFT Return | Information Required for SFT Return |

| The Company other than unlisted Companies | Buyback of shares from any person (other than the shares bought in the open market) | Rs. 10 lakh or more | Details of persons from whom shares were bought back:

Name, PAN, Aadhar, Email ID, complete Address, Pin code, mobile number, person type Details of shares bought back: No. of shares buyback, buyback price, premium (if any) |

– PAN

– Aadhar – Address Proof – Form SH 11 |

| The Company liable for tax audit under sec 44AB | Cash receipt for sale, by any person, of goods or services of any nature | Rs. 2 lakh or more | Details of persons from whom the cash was received:

Name, PAN, Aadhar, Email ID, complete Address, Pin code, mobile number, person type Particulars of cash received: Amount of cash received

|

– PAN

– Aadhar – Address Proof – Copy of Invoice |

| The Company paying dividend | Payment of Dividend | NA | Details of persons to whom the dividend is paid:

Name, PAN, Aadhar, Email ID, complete Address, Pin code, mobile number Details of dividend paid: Amount of dividend paid /credited during the year |

– PAN

– Aadhar – Address Proof |

Ⅳ. Rectification of SFT Report:

Rectification of SFT report can be done in two cases viz. in case of rejected statement & in case the report is processed with some defects or exceptions-

- In case of rejected statements, no statement ID is generated & the return needs to be resubmitted by validating errors. The process of resubmission of rejected statement is the same as the case of uploading the original statement.

- But in case the return is processed with defects or exceptions, the return needs to be resubmitted as per the below-mentioned steps-

1. Log into SFT Portal & download the DQR file statement which has defects. DQR is an XML file. This DQR file is to be downloaded from the statements pending for correction tab under the statement head. OR we can also download the DQR file from the generic submission utility. In such utility go to the tab download DQR. Enter the user ID & password of the SFT portal & also enter the statement ID for which we want to download the DQR. Click on download DQR File.

2. Now open the report generation & validation utility available on the portal & go to the View DQR tab.

3. In this tab you need to upload the DQR report & corresponding original statement which you need to rectify. Make sure that the DQR file number & original file number should match.

4. Defects & exceptions are highlighted in the validation error details sidebar. Click on the defects. It will open the corresponding defective entry. Correct all defects & validated the file.

5. After the validation click on generate the XML file.

6. Then submit the XML file through the generic submission utility. The entire procedure for submission of a defective report will remain the same as in the case of uploading the original statement.

Ⅳ. Due date of filing SFT:

The company needs to furnish its statement of financial transactions on or before 31st May of the next financial year for every previous financial year where the above-mentioned transaction occurs.

Ⅴ. Advice:

- Companies need to focus on updating their ERP for SFT reporting compliance. Companies would have to work with their respective IT department & assess whether SFT reporting can be effectively implemented in the ERP. For effective SFT reporting through ERP system, the role of the IT department becomes crucial.

- If SFT reporting using ERP is not possible then companies would have to update their Internal Financial Controls relating to SFT reporting. Companies would be required to have a strong compliance reporting of SFT transactions to avoid delay in report filing & late fees.

Ⅵ. Conclusion:

Thus, by introducing SFT, Government will keep a watch on high-value transactions undertaken by the taxpayer. The company must be aware of all those compliances related to SFT transactions. Keeping in mind all the consequences of non-compliance, companies need to upgrade their systems according to the requirements and need to be responsible.

Authors:

CA Aakash Mehta | Partner | E-mail: aakash.mehta@masd.co.in

Varsha Dhake | Consultant | E-mail: varsha.dhake@masd.co.in

Vikash Parashkar | Associate Consultant

Author Bio

Hi, If an Indian company issued equity shares to a foreign body corporate thn does indian company need to file SFT. Because the foreign body corporate wont have PAN and PAN is mandatory. Please share the solution for this case.