IMPORTANT CONCEPT AND PROVISIONS RELATING TO THE TAXABILITY OF NON-RESIDENT

Income Tax Act has contained various provisions relevant to Non-Resident person depend upon its residential status, Scope of Income, business connection or permanent establishment in India etc. Under this Article, I would like to draw attention toward those major areas which is the basic/initial point of determining the taxability of Non-resident in India. Once we checked these filters one by one on Non-resident, we can get clear picture about the taxability of Non-resident.

These five major areas are interlinked, so we will do combined study of these sections

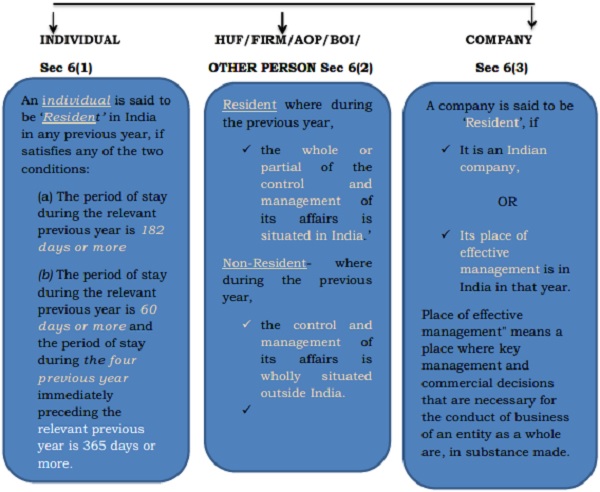

♦ Combined Study of Definition of “Non-Resident” and its “Residential status”

√ Definition of Non-resident- (Sec 2(30) of the Income Tax Act

A non-resident is a person who is not a resident as per Sec 6 of the Income Tax Act.

(currently I am ignoring the non-ordinarily resident here which is covered in the definition of non –resident for the purpose of Sec 92,93 and 168, will discuss the same in next article)

Resident (Sec 6 of the Income Tax Act)

♦ Scope of Income & Income deemed to be received in India/ Income deemed to be accrue/arise in India

√ Scope of Income (as per Sec 5(2) of the Income Tax Act)

The “Total income” of a non-resident shall include the following two:

Explanation 1.—Income accruing or arising outside India shall not be deemed to be received in India within the meaning of this section by reason only of the fact that it is taken into account in a balance sheet prepared in India.

Explanation 2.—For the removal of doubts, it is hereby declared that income which has been included in the total income of a non-resident on the basis that it has accrued or arisen or is deemed to have accrued or arisen to him shall not again be so included on the basis that it is received or deemed to be received by him in India.

√ Income deemed to be received in India (as per Sec 7 of the Income Tax Act)

Income deemed to be received in India mainly includes:

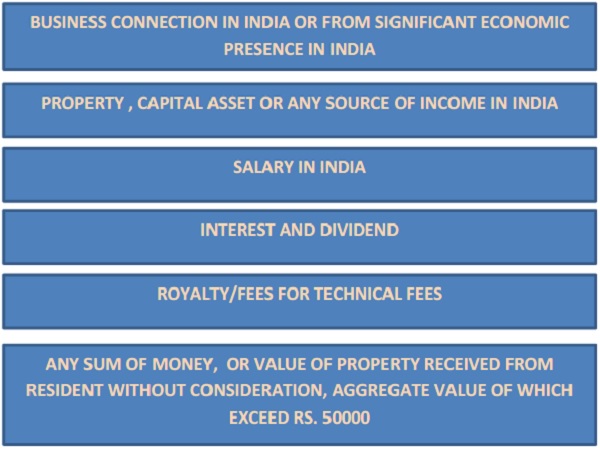

√ Income deemed to accrue/arise in India (as per Sec 9 of the Income Tax Act)

This area is quite complicated and need to be observed and examined carefully while determining the Total income of Non-resident. This income will be considered in the Total income of Non-resident irrespective of whether directly/indirectly.

INCOME ACCRUING OR ARISING FROM

We will discuss all the above income which is tabulated below in detailed form and manner in my Next Article titled “ Income deemed to be accrue/arise In India” to get a clear understanding of all the provisions and concepts considered for determining the Total income taxable in the hands of Non-resident.

Author Bio