CA Kinjesh Thakkar

1. Introduction

1. Introduction

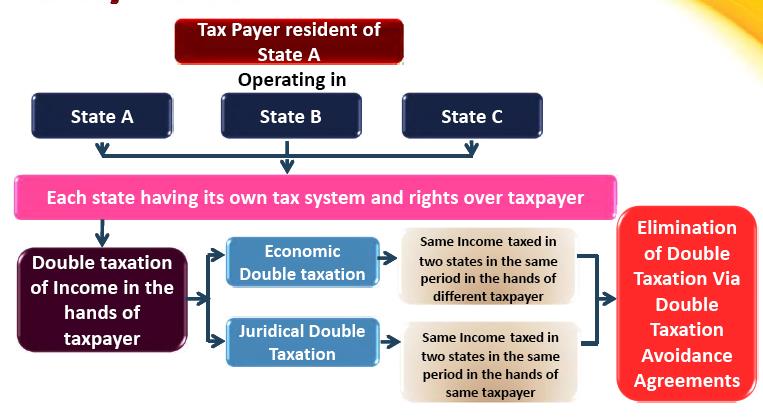

The world economies have moved forward and have come closer to each other making the borders invisible across the globe for economic purposes in recent past. Due to increasing liberaliasation and globalization there are many cross border economic transactions which are carried over across many nations. The world has become a global village. Integration between countries is increasing. In such a scenario earnings of person is not restricted to national boundaries and there are opportunities to make money internationally.

Due to this, there are issues of international taxation due to income earned in foreign state and its taxation in resident state (Taxation of global income) as well as foreign state (Source based taxation). This is the main reason for which a DTAA has come into existence to play its role in avoiding the double taxation.

Now, for understanding DTAA we first need to understand international taxation.

Technically speaking there is no concept such as International taxation. But for our convenience we say, the international aspects of income tax laws of a particular nation as international taxation.

3. Why DTAA?

Every country has its own international tax laws which are divided into two broad dimensions:

I. Taxation of Resident Individuals and corporations on income arising in foreign countries-Taxation of foreign Income

II. Taxation of Non residents on income arising domestically-Taxation of Non-Resident

From above one can understand what taxation of foreign income is for one country (Resident country) is the taxation of Non-resident for another country (Source country).

Thus, there is dual taxation, one in resident country taxing the income and other in source country which levies taxes on same Income.

Therefore, there is a need for agreement between the countries for avoiding this kind of double taxation. This Agreement is known as Agreement for Avoidance of Double Tax or Double Tax Avoidance Agreement – “DTAA”.

The example below illustrates the exact need for DTAA.

Example:

R, Resident of country A, earns 100 of Income from country B.

Tax rate of Country B – 40%

Tax rate of Country A – 50%

Taxability of Assessee R, without DTAA is as under:

| Particulars | Amount |

| Foreign Source Income | 100 |

| Foreign Tax (40%) – Source Based Taxation | 40 |

| Domestic Tax – Global Income Taxable (50%) | 50 |

| Total Taxes Paid | 90 |

| Balance Income after Tax (100-90) | 10 |

| Effective Tax Rate | 90% |

From Above example one can conclude that if double taxation is not avoided then a huge portion of income will flow from the person carrying on economic activity to the Governments of two countries. This will discourage trade and commerce heavily. Hence, avoidance of double taxation is must because if same income is taxed twice then the income left for the taxpayer will be too low to make any economic activity viable to be carried on.

The below chart exactly answers to the question as to why DTAA?

4. What is DTAA?

DTAA is also known as treaty and Treaty is explained in Vienna convention on law of tax treaties 1969 as under:

“An international Taxation Agreement concluded between states in written form and governed by international law, whether embodied in a single instrument and whatever its particular designation”

A treaty is not a taxing statue, although it is an agreement about how taxes are to be imposed.

It is an act between two sovereign states and terms and conditions mentioned therein have to be strictly followed.

5. Purpose of DTAA

DTAA is an Agreement between two or more countries for resolving the issues of taxability of income and increased transparency to avoid tax evasion. The purpose of DTAA is highlighted below.

- Avoidance of Double Taxation of Income.

- For recovery of Income Tax in both the countries.

- Allocate rationally, Equitable and fairly the taxing rights over a Taxpayer’s Income between two states.

- Encourage free flow of international Trade & Investment and Technology.

- Increased transparency.

6. Nature of DTAA

DTAA can be either comprehensive or limited.

I. Comprehensive:

Provides for Taxes on Income, Capital Gains, and Capital. It Ensures that taxpayer in both the states would be treated equally in respect of taxation.

II. Limited:

Provides for Taxes on income from shipping and Air Transport or estate, inheritance or gift. Limited nature DTAA are limited to certain issues of taxability of income.

7. Types of DTAA

There are two types of DTAA as listed Below:

I. Bilateral Treaties:Agreement of DTAA between Two States.

II. Multilateral Treaties: Agreement between two or more States.

8. Relief Mechanism:

Double Taxation Occurs when there:

ü Global+ Source Based Taxation

ü Residency in Two States

The Double Taxation in such Case can be eliminated by various relief mechanisms. These are as under:

I. Deduction Method:

The resident country allows its Taxpayer to claim a deduction for taxes, including income taxes, paid to a foreign government in respect of foreign source income.

It is like providing DEDUCTION as EXPENSES.

II. Exemption Method:

The resident country provides its taxpayer with an exemption for foreign source Income. It is like EXEMPTION of INCOME.

III. Credit Method:

A. Ordinary Credit :

Resident country gives either full/Partial credit of taxes paid in foreign country. This means Tax payer will be taxed on same source income and tax is to be determined accordingly but tax payer will pay lower amount of taxes to the extent credit available.

B. Underlying Credit:

Credit for corporate tax is available when dividends are paid by resident of one state to another. This is in addition to tax paid on dividends.

The Example Below shows the benefit available in all of these methods.

Example:

R, Resident of country A, earns 100 of Income from country B.

Tax rate of Country B – 40%

Tax rate of Country A – 50%

| Particulars | DeductionMethod | Exemption Method | Credit Method |

| Foreign Source Income | 100 | 100 | 100 |

| Foreign Tax (40%) | 40 | 40 | 40 |

| Deduction of foreign Tax | 40 | Nil | Nil |

| Net Domestic Income | 60 | Nil | 100 |

| Domestic Tax Before credit | 30 | Nil | 50 |

| Less: Tax Credit (Assuming full Credit is available) | 0 | 0 | 40 |

| Final Domestic Tax | 30 | Nil | 10 |

| Total Domestic and Foreign Taxes | 70 | 40 | 50 |

From the Above example and computation one can conclude that

- Deduction method does not fully avoid the double taxation. It just saves tax by the amount of –Foreign Tax Paid x Domestic Tax rate.

- Exemption method is more favorable if tax rate in Domestic country are higher than that of in Source Country.

- Credit Method is preferable as the assessee gets taxed at domestic tax rate without any double tax and country also gets its eligible amount of Tax.

IV. Tax Sparing:

Sometimes as an Incentive to economic activities, there are various tax exemptions given. There won’t be any payment of tax by the assessee due to these incentives. For example: Deduction under section 80IB of Income Tax Act, 1961. Now, when the assessee is liable to taxation in his domestic country then credit will be allowed for taxes paid in foreign country, but due to tax exemption in such foreign state there won’t be tax payment and no credit to balance of taxpayer. Now, in such a case if the taxpayer is taxed on credit method basis then he will end up paying taxes on income which was exempt in foreign state. In such a case, there won’t be any incentive to assessee to take up such specified activities on which exemption is granted because if foreign country is not taxing than domestic country will collect tax.

Hence, to avoid such situation Tax Sparing comes to help. Under this method, the domestic country will deem such exempt income as tax paid and credit of such taxes which are deemed to be paid in foreign country will be allowed as credit in Domestic country. Hence, the benefit of exemption is not hindered or wiped out due to this method.

This type of relief mechanism is known as Tax Sparing.

V. Unilateral Relief:

Some countries provide relief of Taxes paid in source country without any treaty between those two countries. This kind of relief is known as unilateral relief.

In India, U/s 91 unilateral relief is provided. Section 91 provides for relief from double taxation to the Indian Residents. Relief is available of lower of Indian Tax and Foreign Tax paid on the income so doubly taxed. It is Applicable only if the said income does not accrue or arise in India as provided in Section 9 of the Act.

The above are all methods of providing Relief from double taxation.

9. Models of Tax Treaty:

There are major two models of Tax Treaty.

A. Organisation for Economic Co-operation and Development (OECD Model).

B. United Nations Model (UN) Model.

C. US Model

The agreement between two nations may be formed based on acceptance of these models or two contracting states may even include certain articles and clause not specified. These are just a model which provides convince in daft of DTAA.

India in its treaties with different nations have accepted some of the items of these models, even included new clause and articles which are not defined in the model and are altogether different between the contracting states. So, treaty is not compulsorily to be made as per model. The above Specified are just models and not treaty.

v Structure of a typical tax treaty

| Parts of Treaty | Articles |

| Scope of the convention | 1 & 2 |

| Definitions | 3 to 5 |

| Taxation of Income | 6 to 21 |

| Taxation of Capital | 22 |

| Provisions for elimination of double taxation | 23A, 23B |

| Special Provisions (Non-Discrimination) | 24 to 29 |

| Final Provisions | 30 |

| Termination | 31 |

| Protocols | These are like amendments |

| Commentaries | Explains the provisions |

The Above structure represents OECD Model Tax Convention.

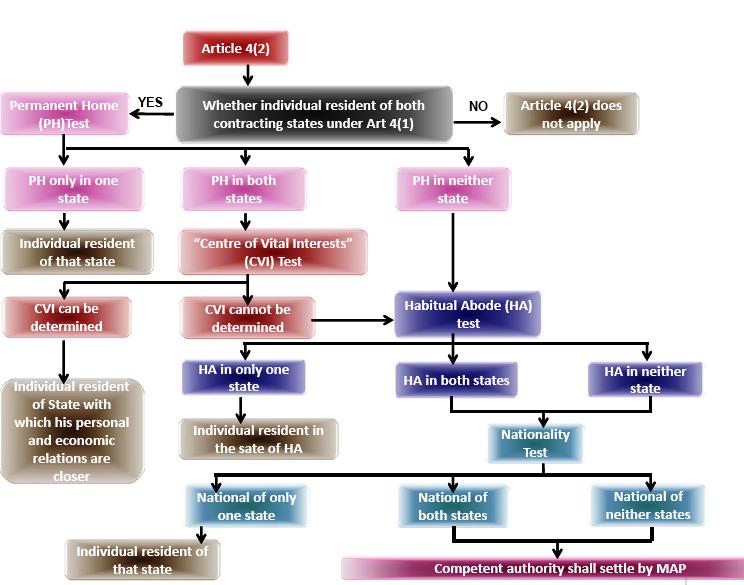

10. Applicability of DTAA:

A Tax Treaty is applicable to persons who are residents of one or both the contracting states. Thus, for applicability of DTAA we need to understand the concept of residence.

– Concept of Residence:

Concept o residence can be classified into 2 parts:

I. For Individuals:

An Individual is liable to tax by virtue of his domicile, residence, Place of incorporation, Place of management etc but excludes one who is liable to tax in respect only of income from source in that state.

By applying above principle one can conclude a person to be resident of one of the contracting states and provisions of treaty will apply accordingly.

But sometimes a person becomes resident of two or more state. This creates confusion as to who will tax the global income and various issues arise to its taxability.

A person who is resident of two states by virtue of law is known as Dual Resident. The residency of such dual resident is known as Dual Residency.

This dual residency needs to be broken and the individual needs to assign residency of one of the states.

Hence, to determine residency the Tie – Breaker test needs to be applied. This is explained in below mentioned chart:

Chart for Determination of Residency of Dual Resident by Tie Breaker Rules

This is how the residence of individual is established and provisions of DTAA apply accordingly.

II. For Legal Entities/Corporations:

For Legal entities the test applied for its residency is place of its Incorporation or Place of effective management.

Legal entities are resident of that state in which it has its incorporation. Place of incorporation is certain and preferable test as place of incorporation does not change from time to time and provides simplicity in determination of residency.

Place of effective management is les certain as now a days business is controlled from many countries. This creates confusion and complications.

This is how a person is Determined as resident. And once a person becomes resident of any of the states he can apply the treaty for avoidance of double tax.

11. General interpretations of Principles of DTAA:

- Tax treaty is based on mutual understanding between two states, if more than one language in involved, there must be a common / uniform interpretation which must be applied.

- Tax treaties are primarily relieving in nature and do not impose tax

- Life of a treaty is long to adapt changes in the domestic law while continuing to reflect the original negotiated balance of obligations and concessions – Static Approach vs. Ambulatory Approach of interpretation

- Requires broad and literal interpretation as compared to domestic laws

- Words which are not explained in treaty find their meaning in Domestic Law

- Treaties entered into by a State are a part of its domestic laws and can be applied only to seek relief from taxes imposed by the domestic laws of a state.

- Where there is ambiguity in the provisions of the treaty, the interpretation which is harmonious with the provisions of the IT Act should be adopted.

The above listed are the interpretation basics of treaty. The Provisions of DTAA are applicable as follows:

| The Treaty | The Local Law | Remarks |

| If Treaty is silent about any dispute | But Income Tax law states some Provisions for the same | Refer law in this regard |

| If treaty states some Provisions | But law is silent about any dispute | Refer treaty |

| If Treaty Explains a provision | Law States the same provision differently | Follow Whatever is beneficial for the assessee |

| If Treaty has some provisions | Law Contradicts the verdict of Treaty | Treaty will prevail in that case |

Now having knowledge about how a DTAA works one need to understand Which DTAA to be applied.

12. How to determine Which DTAA is Applicable:

The following Step Needs to be followed to determine which DTAA is applicable.

Steps for Determination of the DTAA to be applied

| Step No | Description |

| 1 | Transaction having Income taxable under IT Act |

| 2 | One of the parties to the transaction is a non-resident (NR)/Foreign Company (FC) |

| 3 | Determine the residential Status of NR/FC |

| 4 | Tax Treaty between India and country in which the NR/FC is a Resident is the DTAA applicable |

13. How to Apply DTAA?

The following steps mentioned below provides for answer as to how to apply DTAA

Steps for Determination as to how to apply DTAA

| Steps | Description |

| 1 | Determine the nature of income arising to the NR / FC according to the articles of DTAA (specific and general) and also under the IT Act. |

| 2 | Determine the tax liability to the NR / FC under the IT Act |

| 3 | If any of the Specific articles for taxation are applicable then the income is taxed according to that article |

| 4 | If the NR / FC has a Permanent Establishment (PE) in India then general articles for taxation would be applicable |

| 5 | Accordingly determine the tax liability under the DTAA |

| 6 | Applying section 90(2), determine whether IT Act / DTAA is more beneficial (Treaty Override) |

| 7 | Final tax liability of the NR / FC as per the provisions more beneficial |

The above steps provide clear idea as to which DTAA will be applied.

14. Issue in application DTAA (Triangular cases):

Let us understand the above triangular case as on issue to DTAA by an example.

There are 3 Companies. They are:

X, India

Y, UK (Z is a permanent Establishment of Y, UK)

Z, Mauritius (Branch of Y, UK)

X takes loan from Z. Z receives interest from X.

Which Treaty is applicable?

1. Indo-Mauritius Treaty

2. UK-Mauritius Treaty

3. Indo-UK Treaty

- Treaty is applicable to the persons resident in one or both the states

- Person other than individual is a resident of state where its place of effective management is situated

v Indo – Mauritius Treaty

- Z is a non resident of Mauritius as well as India. Hence Indo Mauritius Treaty is not applicable

v UK – Mauritius Treaty

- Z is a non resident of Mauritius. It has its place of effective management in UK and hence is a resident of UK.

- However X being a resident of India does not have access to UK – Mauritius Treaty.

v Indo – UK Treaty

- Z having its place of effective management in UK is a resident of UK (though located in Mauritius)

- X being a resident of India will deduct tax of Z under Indo – UK treaty.

Credit of taxes to Y or Z?

- The tax credit will not be available to Z since the tax is not deducted under Indo – Mauritius Treaty. (relief of taxes paid under the relevant treaty only are granted by a particular treaty)

- The tax credit will be available to Y while filing its return of income since the income of Z (PE of Y) will be clubbed with the income of Y.

The above mentioned types of cases are known as triangular cases in DTAA.

15. Special Treaty Issues:

There are several special Treaty issues which are highlighted below-

A. Non-Discrimination

- Applicable to “Nationals” of Contracting States as against “Resident”.

- Foreign national can’t be discriminated from Indian National In respect to any taxation or any other requirement in same Circumstances.

- There are separate rules for PE in case of Corporation for Non-Discrimination.

B. Treaty Shopping:

Treaty shopping is an important tool for Avoidance of tax. It’s not Evasion of Tax but avoidance, by using the law and within the law.

Let us understand this with an example:

Example

Aco, resident of country A, has developed valuable intangible property and intends to license the property for use by manufactures in several other countries. Country A does not have treaties with some of the countries where the potential licensees are resident, and the treaties with the other countries provide for withholding taxes on royalties of 15 percent. Country A provides an exemption for dividends received from a foreign corporation when a corporation resident in country A has substantial participation in it. Aco, transfers its intangible property to a wholly-owned subsidiary, Bco, established in country B. Country B has tax treaties with all of the countries where the potential licensees are resident, and those treaties provide for no withholding taxes on royalties.

The result of the above arrangement is that no tax will be imposed on the royalties by the countries where the royalties arise. Country B may not tax the royalties derived by B co, either because it is a traditional tax haven. When Bco, distributes dividend to Aco, country A will not tax the dividends because of its exemption for dividends. Even if country A treats the transfer of the intangible property by Aco to Bco as a taxable transaction, it may have significant difficulty in taxing the appropriate amount of gain on transfer because of the problem of accurately establishing the fair market value of the property at the time of he transfer.

This example illustrates Treaty Shopping. In effect, Aco has taken advantage of country B’s treaty network by the simple expedient of establishing a corporation in country B. Bco functions as a conduit to flow through the royalties as tax exempt dividends to Aco. The overall effect is that the withholding taxes of the countries in which the royalties arise are avoided.

16. Conclusion:

The increasing cross border economic transaction has increased the role of all the corporate professionals to provide for tax planning issues on such transactions. The complications in this field of International Taxation is increasing day by day but on a positive note towards more or less settling the law and ending up the debate. The future of tax will now be more focused on international tax aspects rather than more settled Domestic Income taxes in India.

Other Article from the Author – Tax planning and managing the House Property

Republished with Amendments

Very well explained

Well explained the basics!! Very nicely drafted.

Hello,

I am a resident of India and would like to register an LLC in the USA. How would I pay taxes with reference to above. Would you be kind to advice on this. All the business activities will be in US and europe.

We would like to connect with you on International Taxing needs for Japan and US>

Appreciate a call +91-9810278839 to understand and take things forward.

Thanks

We would like to connect with you reference to International Taxation for Japan and US to start with.

This requirement is urgent. Appreciate a call +91-9810278839

It is very good article. I only wonder whether KPMG can update us with latest rulings if any in respect of an issue being faced by local steamer agents at Visakhapatnam with regard to DTAA relating to Singapore. The issue is as follows:

In case of freight earned by non-resident shipping company and as per Article-24 of DTAA “Limitation of Relief” clause entered into India with Singapore the tax treaty benefit is available when the amount is remitted/received in Singapore. What is the correct position of law in case where there is a short remittance of freight amount on account of “address commission”, brokerage etc, which are deducted from the freight amount and which are at the standing instructions of the non-resident shipping company itself and for which proof is produced ? Whether any proportionate taxation to be done in India for such short remitted amount in Singapore ? Your valuable comments are solicited since this being a contentious issue between the IT Department and agents acting on behalf of non-resident shipping companies .

Nice article..

Very Nice article…Good read