Practical Implication of amendment relating to MSME (Section 43B deduction only on payment basis)

What changed in Budget 2023 relating to MSME from a tax perspective??

What is the PRACTICAL WAY OUT for Assessees and Auditors / Consultants??

Want to know?? Then read the entire article!!

Before we deep dive into amendment brought by the government under Income Tax relating to MSME, let’s first understand what is MSME?

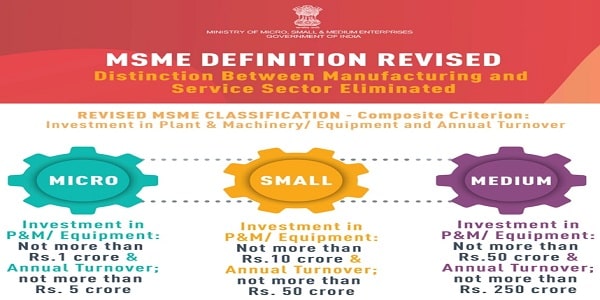

MSME means Micro, Small and Medium Enterprises. It has been governed by MSMED Act, 2006. Based on the Investment made by the enterprise in the P&M / Equipment and their turnover they have been classified into Micro, Small and Medium Enterprises. Below is the Revised MSME Classification.

Just to give you the idea about why MSME sector is too important for the government as well as for India, I’ll share some statastics relating to that. At present, there are 63 million MSMEs are running in India which almost contributes approximately 30% of the GDP. Further, it has contributed to nearly 50% of its exports and in 2022. It has grown by 37% year-on-year (YoY). They nearly employ around 110 million people in India. Therefore, you can easily say that they are the backbone of the Indian Economy. As a result, the government is promoting / incentivizing this sector by every means possible. So, in order to,

i. Safeguard micro/small businesses,

ii. Promote timely payments and

iii. Boost the liquidity,

The government has come up with a very good measure. It has been proposed by the government that w.e.f. FY 2023-24 buyers can claim deduction in income tax only on payments made to a micro and small (not medium) supplier. In short, a company can’t claim the expense under the act until the payment has actually been made to the seller. The proposal was made to resolve the long-standing delayed payments’ problem of MSMEs and provide them a much-needed liquidity boost.

So, if buyers take an invoice from a micro and small enterprise, they will have to actually make the payment to them in order to take a deduction in the income tax for that particular expenditure. Otherwise, it will be added to their income. This is a very dangerous provision for defaulters.

Let’s read in detail about the practical implications of this provision.

The government has proposed that buyers will be able to claim the deduction of expenses only if the payment has been made to a MSME supplier.

1. So, the first question that comes to the mind is, how can you find out that the goods or services you acquired from is micro or small enterprise and also registered as MSME?

Practical Solutions for assessee: At the time of purchase only, the buyer must obtain a declaration from the company stating whether they are registered micro or small enterprise or not. If yes, then take the certificate from them for your records. Additionally, assessee must incorporate this information in their accounting software so that an auditor / tax consultant can easily verify the details at the time of Audit or finalization of books of account. Alternately, they can also keep a master list of all the vendors having MSME registration, which can be helpful at the time of audit or filing an ITR.

Practical Solution for Auditor / consultant: The auditor will have to take the representation letter from the assessee specifying the amount outstanding to MSMEs and other as on year end similar to what they have been doing in case of companies. This will be a cumbersome process because now auditor has to take the representation letter even from an individual.

2. Now that you know that the party is registered micro or small enterprise, but the second question is by when buyer needs to make the payment in order to claim the deduction?

As per Section 15 of MSMED Act, 2006, the buyer will require to make payment;

i. In case of written agreement: within time limit as specified in the agreement but cannot exceed 45 days;

ii. In case of no written agreement: within 15 days

So, in order to claim the deduction you will have to make the payment within the above period. So, let’s understand this in 3 parts:

i. If you pay the amount within due date or after due date but before the end of the year: Deduction is allowed in the same year i.e. in the year of accrual/payment.

ii. If you pay the amount after the end of the year but within the due date: Deduction is allowed in the same yeare. in the year of accrual.

iii. If you pay the amount after the end of the year and after the due date: Deduction is allowed in the next yeare. in the year of payment

Practical Solution for assessee: Assessee must review the list of outstanding dues before the end of the year and bifurcate them into MSME vendors and others. Identify the bill date and due date for payment relating to outstanding dues and prioritize the payment to MSME vendors over others in order to claim the deduction in that year itself.

Practical Solution for Auditor / consultant: At the time of finalization or audit check the list of outstanding dues as on 31/03 and divide that into MSME vendors and others. Then you must check the bill date which was outstanding and determine when was it paid. So, once you have the bill date and payment date, you will be able to determine when the deduction is available.

3. Important Points relating this amendment:

i. The supplier needs to be registered in the MSME Act, 2006 to avail the benefit of 15 days/45 days. (Take MSME registration if you’re eligible)

ii. The above provisions are only applicable to Micro or Small Enterprises. It is not applicable to Medium Enterprises.

iii. In case of Capital expenditure or in case where expense has not been claimed as expenditure then disallowance u/s. 43B of the Act shall not be attracted.

iv. The above provisions are not applicable if you are a presumptive business or profession making payments to a business as no specific expense is disallowed and Income is deemed at a certain percentage.

v. As per O.M. 5/2(2)/2021-E/P & G/Policy dated 02-07-2021, wholesale and retail trader are entitled for Udyam registration only for the benefit of Priority Sector Lending only. So, purchase from traders would be outside the purview of these amendments.

vi. It should be noted that, the proviso to Section 43B regarding payment of allowability of expenditure if paid before the due date of furnishing the return of Income shall not applicable to this.

4. Consequences:

i. The proposed amendment by the government would ensure timely payments to the micro and small enterprises, leading to better working capital management.

ii. However, on the flipside, the amendment may also pose a negative consequence for assessees who are making contractual payments to these entities, as the proposed amendment necessitates a robust mechanism to monitor various due dates while making payments to multiple micro and small enterprises to avoid the disallowance of huge amounts. This would lead to a cumbersome exercise of closely tracking the disallowances and allowances in subsequent year(s) to comply with the provisions of the Act thereby saddling the assesses with higher operational costs.

iii. There is also a possibility that businesses wants to cut back or minimize their commercial relationships with MSMEs since they will have to worry about the deduction at the year end. Normally, the credit duration in many business lines is 90 days but the limit of 15 days (in the absence of agreement) and 45 days (in case of agreement) would discourage them from doing any business with MSME. So, it will largely impact the sector having credit period more than 45 days.

Let’s wait and watch how this plays out in the real world. Only after the implementation of this provision, we will be able to determine if it will in fact boost or deter the MSME sector.

#business #msme #tax #taxaudit #taxplanning #directtax #budger2023 #amendments

Author Bio

please update me on income tax rules

nice article sir. very helpful.