Implications on Works contract and Job work – Journey from old regime to GST

Works contract has been a mystery for almost half a century and yet it fancies every avid leaner of Indirect tax. It is a composite contract involving both transfer of property and provision of labour. We shall examine the implications of Goods and Services Tax Law (“GST law”) on Works contract in this paper.

Page Contents

1. Works contract and VAT

This charge started by State of Madras v. Gannon Dunkerley & Co. (Madras) Ltd., 1959 SCR 379 is still in its never ending journey. The Constitution Bench of Apex Court held that in a building contract which was one and entirely indivisible, there was no sale of goods and it was not within the competence of the State Legislature to impose a tax on the supply of materials used in such a contract, treating it as a sale.

The Hon’ble Apex Court held that a works contract is a composite contract which is inseparable and indivisible, and consists of transfer of property in goods but labour and service elements as well. The Court held that what was within the purview of state legislature was to levy tax on sale of goods chattel qua chattel. Hon’ble Court, after considering a large number of judgments, ultimately came to the following conclusion :-

“To sum up, the expression “sale of goods” in Entry 48 is a nomen juris, its essential ingredients being an agreement to sell movables for a price and property passing therein pursuant to that agreement. In a building contract which is, as in the present case, one, entire and indivisible — and that is its norm, there is no sale of goods, and it is not within the competence of the Provincial Legislature under Entry 48 to impose a tax on the supply of the materials used in such a contract treating it as a sale.” (at page 425)

Thereafter a battery of other decisions holding similar decisions were upheld by courts. Accordingly, government came out with a solution viz., by introducing provision of deeming Sale in the Constitution of India

Constitutional Amendment –

The Constitution was amended by 46th Amendment and clause (29-A) was inserted in Article 366, clause (29A) of Article 366 is in the following terms.

“(29-A) tax on the sale or purchase of goods includes-

“(a) ………………..

(b) a tax on the transfer of property in goods (whether as goods or in some other form) involved in the execution of a works contract;

(c) ………”

The Constitutional amendment so passed was the subject matter of a challenge in Builders’ Assn. of India v. Union of India, (1989) 2 SCC 645. This challenge was ultimately repelled and Apex Court stated:-

“… After the 46th Amendment, it has become possible for the States to levy sales tax on the value of goods involved in a works contract in the same way in which the sales tax was leviable on the price of the goods and materials supplied in a building contract which had been entered into in two distinct and separate parts as stated above.” (at para 36)

Works contract in VAT Laws

VAT Acts have defined works contract in more or less similar manner. Definition as provided in VAT Acts are as under:

– Delhi

“works contract” includes any agreement for carrying out for cash or for deferred payment or for valuable consideration, the building construction, manufacture, processing, fabrication, erection, installation, fitting out, improvement, repair or commissioning of any moveable or immovable property.

– Haryana

“works contract” includes any agreement for carrying out for cash, deferred payment or other valuable consideration, the assembling, construction, building, altering, manufacturing, processing, fabrication, installation, fitting out, improvement, repair or commissioning of any movable or immovable property

– Tamil Nadu

“works contract” includes any agreement for carrying out for cash, deferred payment or other valuable consideration, building construction, manufacture, processing, fabrication, erection, installation, fitting out, improvement, modification, repair or commissioning, of any movable or immovable property

– Uttar Pradesh

“works contract” includes any agreement for carrying out, for cash, deferred payment or other valuable consideration, the building construction, manufacture, processing, fabrication, erection, installation, fitting out, improvement, modification, repair or commissioning of any movable or immovable property

Thus, it is pertinent to note that specific transaction are included in works contract under State VAT Acts.

Valuations Settled – Gannon Drunkley II

Apex Court again upheld the levy of Sales Tax (now VAT) on works contract pursuant to Constitutional amendment, however, laid down the guidelines for determination of value. Apex Court held that tax on transfer of property in goods (whether as goods or in some other form) involved in the execution of a works contract falling within the ambit of article 366 (29A) (b) is leviable is on the goods involved in the execution of a works contract and the value of the goods which are involved in the execution of works contract would constitute the measure for imposition of the tax.

Hon’ble Court held that the value of the goods involved in the execution of a works contract will, therefore, have to be determined by taking into account the value of the entire works contract and deducting therefrom the charges towards labour and services which would cover:

a) Labour charges for execution of the works;

b) amount paid to a sub-contractor for labour and services;

c) charges for planning, designing and architect’s fees;

d) charges for obtaining on hire or otherwise machinery and tools used for the execution of the works contract;

e) cost of consumables such as water, electricity, fuel etc. used in the execution of the works contract the property in which is not transferred in the course of execution of a works contract; and

f) cost of establishment of the contractor to the extent it is relatable to supply of labour and services;

g) other similar expenses relatable to supply of labour and services;

h) profit earned by the contractor to the extent it is relatable to supply of labour and services.

Thus, this was the first time when the Circle for taxability of works contract under Sales tax (VAT) got complete and the state governments got their right to tax such transactions.

Valuation provision is also almost similar in all VAT Acts. VAT law usually provide for three methods of computation of value for the levy of VAT:

a. Actual Value

This method requires calculation of actual value of goods whose property is transferred via the executed works contract. The formulae for this as provided in Gannon Drunclety II has been replicated in most of the VAT laws. It is provided that to arrive at the taxable Turnover arising from the execution of a works contract, from the total consideration paid or payable to the dealer under the contract one has to exclude the charges towards labour, services and other like charges (nature provided in case above).

b. Deemed Value

If a dealer does not want to or cannot make calculation on actual basis, a choice has been given to him in terms of prescribed percentages of value towards labour, services and other like charges. For eg.

| Sl. No. | Type of contract | Labour, service and other like charges are percentage of total value of the contract |

| 1 | Fabrication and installation of plant and machinery. | Twenty five percent |

| 2 | Fabrication and erection of structural works of iron and steel including fabrication, supply and erection of iron trusses, purloins and the like. | Fifteen percent |

| 3 | Fabrication and installation of cranes and hoists. | Fifteen percent |

c. Composition Scheme

In a Composition scheme, government provides for payment of VAT a predefined rate on the entire consideration of the contract say 5%. Such composition schemes are usually restrictive in terms of inter state purchase and sale and input credits.

Dominant intention would determine nature – initial understanding

The Hon’ble Supreme Court in Rainbow Colour Lab Vs. State of Madhya Pradesh (2000) 118 STC 9 (SC) held that unless there is a sale and purchase of goods, either in fact or deemed, and such sale is primarily intended and not incidental to the contract, the State cannot impose sale tax on a work contract simply on the basis of the expanded definition found in article 366 (29-A)(b) of the Constitution.

In Hindustan Aeronautics Limited v. State of Orissa – (1984) 2 SCC 16, the Court, while emphasizing that there is no rigid or inflexible rule applicable alike to all transactions which can indicate distinction between a contract for sale and a contract for work and labour, opined that basically and primarily, whether a particular contract was one of sale or for work and labour depended upon the main object of the parties in the circumstances of the transaction.

Associated Cement Co. Limited – the Game Changer

A three – Judge Bench of the Supreme Court in Associated Cement Co. Ltd. Vs. Commission of Custom. (2001)124 STC 59(SC) overturned the Dominant nature theory and held as under:

“The 46th Amendment was made precisely with a view to empower the State to bifurcate the contract and to levy sales tax on the value of the material involved in the execution of the works contract, notwithstanding that the value may represent a small percentage of the amount paid for the execution of the works contract. Even if the dominant intention of the works contract is the rendering of services which amounts to a works contract, after the 46th Amendment the state would now be empowered to levy sales tax on the material used in such contract. The conclusion arrived at in Rainbow Colour Lab case (2000) 118 STC 9 (SC), (2000) 2 SFC 385, in our opinion, runs counter to the express provision contained in article 366 (29A) as also of the Constitution Bench decision of Apex Court in Builders’ Association of India V. Union of India (1989) 73 STC 370: (1989) 2 SCC 645.”

In Bharat Sanchar Nigam Ltd., a three-Judge Bench agreed with the position adopted in above case.

Kone Elevator – the Settler

In Kone Elevator India Pvt. Ltd. [2014 (34) S.T.R. 641 (S.C.)], five member bench, by majority, of Supreme Court held that supply and installation of lifts is a works contract overruling its ealier decision in the same case. The Court observed that no single formula could have been stated to be made applicable for the determination of the nature of the contract, for it depended on the facts and circumstances of each case. Upholding the contract as works contract, it was held as under:

“The installation requires considerable skill and experience. The labour and service element is obvious. What has been taken note of in Kone Elevators (supra) is that the company had brochures for various types of lifts and one is required to place order, regard being had to the building, and also make certain preparatory work. But it is not in dispute that the preparatory work has to be done taking into consideration as to how the lift is going to be attached to the building. The nature of the contracts clearly exposit that they are contracts for supply and installation of the lift where labour and service element is involved. Individually manufactured goods such as lift car, motors, ropes, rails, etc. are the components of the lift which are eventually installed at the site for the lift to operate in the building. In constitutional terms, it is transfer either in goods or some other form. In fact, after the goods are assembled and installed with skill and labour at the site, it becomes a permanent fixture of the building. Involvement of the skill has been elaborately dealt with by the High Court of Bombay in Otis Elevator (supra) and the factual position is undisputable and irrespective of whether installation is regulated by statutory law or not, the result would be the same. We may hasten to add that this position is stated in respect of a composite contract which requires the contractor to install a lift in a building. It is necessary to state here that if there are two contracts, namely, purchase of the components of the lift from a dealer, it would be a contract for sale and similarly, if separate contract is entered into for installation, that would be a contract for labour and service. But, a pregnant one, once there is a composite contract for supply and installation, it has to be treated as a works contract, for it is not a sale of goods/chattel simpliciter. It is not chattel sold as chattel or, for that matter, a chattel being attached to another chattel. Therefore, it would not be appropriate to term it as a contract for sale on the bedrock that the components are brought to the site, i.e., building, and prepared for delivery. The conclusion, as has been reached in Kone Elevators (supra), is based on the bedrock of incidental service for delivery. It would not be legally correct to make such a distinction in respect of lift, for the contract itself profoundly speaks of obligation to supply goods and materials as well as installation of the lift which obviously conveys performance of labour and service. Hence, the fundamental characteristics of works contract are satisfied. Thus analysed, we conclude and hold that the decision rendered in Kone Elevators (supra) does not correctly lay down the law and it is, accordingly, overruled.”

Thus, the nature of works contract was now settled and its valuation shall be what has been settled by Gannon Drunkley II and adopted as part of their Rules by most of the state VAT Laws.

2. Works contract and Service Tax

Works contract has been defined in Service Tax vide Section 65B(54) as under:

“works contract” means a contract wherein transfer of property in goods involved in the execution of such contract is leviable to tax as sale of goods and such contract is for the purpose of carrying out construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation, alteration of any movable or immovable property or for carrying out any other similar activity or a part thereof in relation to such property;

Thus, the definition is wider in terms of understanding but has been again restricted to 10 activities.

Valuation

Rule 2A of Service tax (Determination of Value) Rules, 2006 deals with valuation provision in case of works contract. The Rule provides for two options for determination of value of services in a Works contract. The two options are not a choice, but when the first option is not possible, only then the second option is to be resorted to.

♥ Option I : When value of value added tax has been paid on the actual value of transfer of property in goods

This option is available in cases where the contractor knows the exact portion of goods as is used in works contract and property in which has been transferred to the contractee on actual value. No proportion or abatement as provided under the state VAT laws is sued to determine the VAT to be paid and the calculation towards goods is made at actuals.

It is further provided that under this option, Gross amount shall not include the value added tax / sales tax paid, if any, on transfer of property in goods involved in the execution of the said works contract. However, it further provides that the Gross Amount shall include the following items:

- labour charges for execution of the works;

- amount paid to a sub-contractor for labour and services;

- charges for planning, designing and architect’s fees;

- charges for obtaining on hire or otherwise, machinery and tools used for the execution of the works contract;

- cost of consumables such as water, electricity, fuel used in the execution of the works contract;

- cost of establishment of the contractor relatable to supply of labour and services;

- other similar expenses relatable to supply of labour and services; and

- profit earned by the service provider relatable to supply of labour and services;

♥ Option II: When value has not been determined under Option I

If Option I is not possible to be followed, service tax shall be paid in the following manner:

| Type of Works Contract | Options | Manner of computation of service tax |

| Original Works

(a) “original works” means- (i) all new constructions; (ii) all types of additions and alterations to abandoned or damaged structures on land that are required to make them workable; (iii) erection, commissioning or installation of plant, machinery or equipment or structures, whether pre-fabricated or otherwise; |

In other cases | Service tax shall be payable on 40% cent of the total amount including such gross amount |

| In case of works contract, not covered under sub-clause (A), including works contract entered into for,—

(i) maintenance or repair or reconditioning or restoration or servicing of any goods; or (ii) maintenance or repair or completion and finishing services such as glazing or plastering or floor and wall tiling or installation of electrical fittings of immovable property, service tax shall be payable on seventy per cent of the total amount charged for the works contract |

Service tax shall be payable on 70% of the total amount charged for the works contract |

3. Works contract and GST

Works contract has been defined in section 2 of the Act as follows:

(107) ”works contract” means an agreement for carrying out for cash, deferred payment or other valuable consideration, building, construction, fabrication, erection, installation, fitting out, improvement, modification, repair, renovation or commissioning of any moveable or immovable property

Thus, the definition as adopted in GST is more influenced from VAT laws than Service tax. Accordingly, the definition does not provide for any generic definition but only includes 12 types of contract as works contract, which are as follows:

- building

- construction,

- fabrication,

- erection,

- installation,

- fitting out,

- improvement,

- modification,

- repair,

- renovation or

- commissioning of any movable or immovable property

Thus, as per the present definition, there is no requirement of any transfer of property, nor any other contract can be classified as works contract.

Works Contract – Services

Model GST Law has classified many types of transactions which involved both supply of goods as well as services as either of them i.e. either supply of goods or of services. Accordingly, Clause 5(f) of Schedule II of Model GST Law classifies works contract including transfer of property in goods (whether as goods or in some other form) involved in the execution of a works contract as supply of services. Thus even when there is transfer of property in goods during execution of any works contract, such contract shall be classified as supply of services and the entire value shall be taxed accordingly and no more bifurcation of such contract is required in future. However, this treatment of works contract and unamended Article 366(29A) in the Constitution leaves us with one thought as to whether the said Article still determines the nature of works contract or not.

Place of supply in case of works contract

a. Place of Supply of goods: Section 5(4) of Integrated GST Law provides that where the goods are assembled or installed at site, the place of supply shall be the place of such installation or assembly. Accordingly, the location of supplier and recipient is not relevant in present case.

b. Place of Supply of services: Section 6(4)(a) of Integrated GST Law provides that the place of supply of services, in relation to an immovable property, shall be the location at which the immovable property or boat or vessel is located or intended to be located.

Point of Taxation of works Contract

Section 12(2) provides for time of supply in case of goods to be originated out of a works contract as earlier of the following:

- the date on which the goods are made available to the recipient

- the date on which the supplier issues the invoice with respect to the supply; or

- the date on which the supplier receives the payment with respect to the supply; or

- the date on which the recipient shows the receipt of the goods in his books of account

Section 13(3) of Model GST Law provides that the time of supply shall be as under for the purpose of determining most of the works contracts (qualifying as continuous supply of services):

- where the due date of payment is ascertainable from the contract, the date on which the payment is liable to be made by the recipient of service, whether or not any invoice has been issued or any payment has been received by the supplier of service;

- where the due date of payment is not ascertainable from the contract, each such time when the supplier of service receives the payment, or issues an invoice, whichever is earlier;

- where the payment is linked to the completion of an event, the time of completion of that event

Section 2(31) of the Model GST Law defines “continuous supply of services” as “supply of services which is provided, or agreed to be provided, continuously or on recurrent basis, under a contract, for a period exceeding three months with periodic payment obligations and includes supply of such service as the Central or a State Government may, whether or not subject to any condition, by notification, specify”

Input tax credit not available for civil works contract

Section 16(9) provides that Input tax credit shall not be available for the following in relation to works contract:

(c) goods and/or services acquired by the principal in the execution of works contract when such contract results in construction of immovable property, other than plant and machinery;

(d) goods acquired by a principal, the property in which is not transferred (whether as goods or in some other form) to any other person, which are used in the construction of immovable property, other than plant and machinery;

Transitions – Certain important provisions

a. Treatment of long term construction / works contracts

Section 159 of the Goods and Service Tax Act, 2016 provides that the goods and/or services supplied on or after the appointed day in pursuance of a contract entered into prior to the appointed day shall be liable to tax under the provisions of this Act.

The term “appointed date” as defined under section 2 means the date on which Goods and Service Tax Act, 2016 comes into force.

b. Treatment of retention payments

Section 161 of the Goods and Service Tax Act, 2016 provides that irrespective of the provisions of section 12 and 13, no tax shall be payable on the supply of goods and/or services made before the appointed day where a part consideration for the said supply is received on or after the appointed day, but the full duty or tax payable on such supply has already been paid under the earlier law.

4. Job Work under GST

Job work has been defined under Section 2(62) of the Model GST Law as “undertaking any treatment or process by a person on goods belonging to another registered taxable person and the expression “job worker” shall be construed accordingly”.

Again, Job work shall constitute any treatment or process on goods belonging to some other person. Thus, unless there is a supply of goods for undertaking any further goods, there cannot be a job work. Also, there cannot be a job work for unregistered person or for non taxable person.

Treatment of Job worker as a separate Taxable Person

For all purpose of GST Law, Job worker, except the Job worker specified in Section 43A shall be construed as a separate taxable person and thus, all supply of goods and / or services between the Principal and the Job worker shall be subjected to GST. Thus, it shall not be limited to levy of services or supply of goods during job work to Principal.

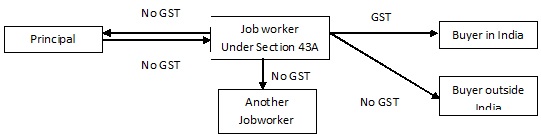

Special case of certain Jobworker

Section 43A(1) of the Goods and Service Tax Act, 2016 is applicable to both the Acts i.e. the CGST Act as well as the SGST Act. The section provides that the Commissioner may permit a registered taxable person (herein referred to in this section as the “principal”), by special order and subject to conditions as may be specified by him, to send taxable goods, without payment of tax, to a job worker for job-work and from there subsequently send to another job worker and likewise, and may, after completion of job-work, allow to-

a) bring back such goods to any of his place of business, without payment of tax, for supply therefrom on payment of tax within India, or with or without payment of tax for export, as the case may be, or

b) supply such goods from the place of business of a job-worker on payment of tax within India, or with or without payment of tax for export, as the case may be.

The above scenario can be captured as under:

The proviso to sub-section (1) of section 43A provides that the goods shall not be permitted to be supplied from the place of business of a job worker in terms of clause (b) unless the “principal” declares the place of business of the job-worker as his additional place of business except in a case-

(i) where the job worker is registered under section 19; or

(ii) where the “principal” is engaged in the supply of such goods as may be notified in this behalf.

Section 43A(2) provides that the responsibility for accountability of the goods including payment of tax thereon shall lie with the “principal”.

Conclusion:

Though with classification of the entire works contract as services, it seems the dispute of valuation between goods and service components of the works contract would not longer pose a problem for the provider, however, the benefit of composition or taxation of many goods at lower rate may not be available to the assessees in future. The benefit is likely to be showed in the benefit of classification and the entire value may be subjected to higher rate as be applicable to services. Also, the consumer shall be at loss in case no abatement to compensate lower rates of taxes in certain contracts like contraction etc is given.

I’m doing a job work for IOCL in panjab. The company was deducting 6% as WCT till June 2017.

Pls clarify that the company will still deduct the same after the implementation of GST from July 2017.

Not Correct. IGST Act is applicable in the case of Inter State Transaction. As such Section 5 of the IGST Act will be applicable wherever the transaction is Inter state.

In my view section 5 of the IGST Act do not apply to Works Contract (WC) as every WC are supply of service under the MGL.