INTORDUCTION

The e-Way bill system is for GST-registered persons / enrolled transporter for generating the waybill (a document to be carried by the person in charge of conveyance) electronically on commencement of movement of goods exceeding the value of Rs. 50,000 in relation to the supply or for reasons other than supply or due to inward supply from an unregistered person.

The e-way bill has been made mandatory for inter-state supplies from April 1, 2018, and for intra-state supplies from April 25, 2018, in certain states (Arunachal Pradesh, Madhya Pradesh, Meghalaya, Sikkim, and Pondicherry).

An e-way bill must be generated before the goods are shipped and it should include details of the goods, their consignor, recipient, and transporter.

An e-way bill is generated for:

- Supply of goods

- Non-supply transactions like export/import, return of goods, job work, line sales, sale on an approval basis, semi or completely-knocked-down supply, supply of goods for exhibition or fair, and goods used for personal consumption.

Page Contents

RESPONSIBILITY TO GENERATE E WAY BILL

Every registered person who may be a consignor, consignee, recipient, or transporter should generate an e-way bill if the transportation is being done through their own or hired means of transport (air/rail/road).

An unregistered person who is supplying to a registered recipient. Here, the recipient will need to follow the compliance procedure since the supplier is not registered.

The transporter should generate an e-way bill, if both the consignor and the consignee fail to generate an e-way bill despite having handed over the goods to the transporter, for conveyance by road.

Note: The consignor can authorize the transporter/courier agency/e-commerce operator to fill PART-A of the e-way bill on their behalf.

DOCURMENT REQUIRED DURING TRANSPORTATION OF GOODS

The invoice, bill of supply, or delivery challan. For transportation by road, the transporter should carry their transporter ID.

For transportation by rail/air/ship, the transporter should carry their transporter ID, and transport document number along with the date of transportation.

A copy of the e-way bill or the e-way bill number (EBN). The transporter can either carry a physical paper copy of the EBN or map it to a Radio Frequency Identification Device (RFID).

EXEMPTIONS IS ISSUE E WAY BILLS

An e-way bill is not required in the following cases:

- If the value of the consignment is less than Rs. 50,000.

- When the goods being shipped are exempt from GST.

Note: If the consignment contains both – exempt and taxable goods, the value of exempt goods is excluded from the value of the consignment.

If goods are transported by non-motorized conveyances (for example railways). Though an e-way bill is not required, an invoice or a challan should be carried during the transportation of goods.

If goods are transported from a port, airport, air cargo complex, or land customs station to an inland container depot or a container freight station for clearance by the Customs Department.

Transport of goods as specified in Annexure to Rule 138(14) of the CGST Rules, 2017.

“BILL TO SHIP TO” TRANSACTION

The Goods and Services Tax (GST) is an indirect tax based on the consumption destination. Hence it is very important for the taxpayers to correctly determine the place of supply, especially in transactions where the billing address and the actual shipping address are different.

Bill-to-ship-to transactions are a common practice in daily business. These transactions involve supplies where the goods are delivered to the recipient on the instruction of a third party. These types of transactions involve three parties,

Place of supply for “Bill to Ship to” transactions is defined under GST under Section 10 (b) of IGST;

(b) where the goods are delivered by the supplier to a recipient or any other person on the direction of a third person, whether acting as an agent or otherwise, before or during the movement of goods, either by way of transfer of documents of title to the goods or otherwise, it shall be deemed that the said third person has received the goods and the place of supply of such goods shall be the principal place of business of such person;

In GST Regime, the place of supply of goods is an important factor to determine whether the transaction is interstate or intrastate, and accordingly, the applicable taxes can be levied.

if the goods are supplied by the supplier to the recipient at the direction of a third person, it will be deemed that the third person has received the goods, and the place of supply will be the principal place of business of the such third person.

In both cases, CGST, SGST/UTGST, or IGST is levied to the respective recipients of both supplies depending on their places of business. The following examples show how the place of business can be determined for various scenarios.

WHO WILL ISSUE E WAY BILL IN “BILL TO SHIP TO” CASE

The department in its “press issue* released on 23rd April 2018 addressed the issues regarding the “Bill To Ship To” for e-Way Bill and clarified that as per the CGST Rules, 2017 either of the party can generate the e-Way Bill and that only one e-Way Bill is required to be generated. The person generating the e-way bill will mention the details of his tax invoice

A number of representations have been received seeking clarifications in relation to the requirement of an e-Way Bill for the “Bill To Ship To” model of supplies.

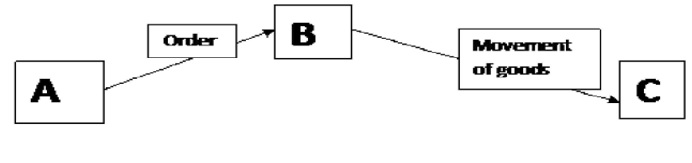

1. In a typical “Bill to Ship To” model of supply, there are three persons involved in a transaction, namely:

‘A’ is the person who has ordered ‘B’ to send goods directly to ‘C’.

‘B’ is the person who is sending goods directly to ‘C’ on behalf of ‘A’

‘C’ is the recipient of goods.

2. In this complete scenario two supplies are involved and accordingly two tax invoices are required to be issued:

Invoice -1 which would be issued by ‘B’ to ‘A’.

Invoice -2 which would be issued by ‘A’ to ‘C’.

3. Queries have been raised as to who would generate the e-Way Bill for the movement of goods which is taking place from ‘B’ to ‘C’ on behalf of ‘A’. It is clarified that as per the CGST Rules, 2017 either ‘A’ or ‘B’ can generate the e-Way Bill but it may be noted that only one e-Way Bill is required to be generated.

ELIGIBILITY OF ITC IN CASE OF “BILL TO SHIP TO”

There are three parties involved in BILL TO SHIP TO Transaction. One is Supplier (Consignor). Second Consignee and third the Receiver of goods. Supplier issued to tax invoice to Consignee and Consignee will eligible for ITC on Tax invoice from Supplier. In the case of a third party (Receiver) is eligible for ITC on the invoice issued to them by Consignee.

In the case of Umax Packaging (A unit of Uma Polymers Ltd.), In re [2018] (AAR- RAJASTHAN) cleared by the department that consignee under whose instructions goods are supplied to the recipient can take ITC of GST charged by the supplier and in turn charge, GST to final recipient in the “bill to ship to” the transaction under section 10(1)(b) of IGST Act.

CONCLUSION

As an understanding of e-way bills, it is clear that they should be issued by the supplier only because he is responsible for the supply of goods. In the case of “BILL TO SHIP TO” the government already cleared that the supplier e-way bill is sufficient for the movement of goods and a copy of the Tax invoice of the Supplier is sufficient for this. Transaction between Consignee and Third Party only sending of Tax Invoice. After issuing of Press release government cleared the most important doubt of the field Inspector of GST as they seize the vehicle based on the difference in values or differences in address. Now the picture is cleared by the department only one e-way bill from Supplier will be issued in case of “BILL TO SHIP TO” Transactions.

These are author’s personal views and cannot be construed to be the views of the ICAI. It shall not be used for any legal advice/opinion and shall not be used to render any professional opinion/advice. The information contained in the article is for the purpose of spreading information / knowledge/ awareness and shall not be treated as solicitation in any manner or for any other purpose.

*****

CA (Dr) Piyush Kapoor | Mob: 9993844411 | Email: capiyushkapoor@yahoo.com

Disclaimer : These are author’s personal views and cannot be construed to be the views of the ICAI. It shall not be used for any legal advice/opinion and shall not be used to render any professional opinion/advice. The information contained in the article is for the purpose of spreading information / knowledge/ awareness and shall not be treated as solicitation in any manner or for any other purpose.

Do we need to carry both invoices, means our invoice to customer and customer’s invoice to third party during goods transit in case of Bill to ship to transaction?