CA. Mandar Telang and CA. Jayesh Gogri

With the passage of the Constitution (122nd Amendment) Bill, 2014, (popularly known as GST Bill) in Parliament, a uniform indirect tax regime across India is one step closer to the reality. The amendments to the GST Bill as passed by Rajya Sabha have also been adopted by the Lower House on 8th August 2016. Before that, the model GST laws (SGST, CGST and IGST) were placed in public domain on 14th June 2016. Although this is not a final piece of legislation, the broad framework of the law is clearly outlined by the said model law. The focus of this write up is on valuation provisions and hence provisions dealing with exemptions are not dealt with fully. Read on to know more…

Te concepts of ‘service’, ‘manufacture’ and ‘sale’ have their own chgoaracteristics, similarities and distinctions. For instance, ‘service’ is generally regarded as broader in scope than ‘manufacture’ and ‘sale’ as it includes any activity carried out for consideration, whereas ‘manufacture’ means only those activities which result into change in the form of commodity and ‘sale’ means those activities which result into change in the ownership of the commodity. Concept of sale and service, however, presupposes existence of two persons, whereas the manufacture can be on one’s own account and existence of two persons is not a pre-requisite. Ordinarily, sale takes place after the manufacture is complete. However, in certain transactions, the manufacturing and sale can take place the same time (for instance works contract).

From constitutional and taxation aspects, concepts of ‘manufacture’, ‘sale’ and ‘service’ are further expanded by incorporating various deeming fictions under the respective tax laws. Presently, activity of ‘manufacture’ is identified with levy of excise duty and is limited to manufacture of goods; whereas the ‘sale’ is restricted to sale of goods and is characterised by levy of VAT or Central sales tax. The service, on the other hand, constitutes a residuary set of activities, whether in relation to goods or otherwise (but excluding ‘manufacture’ and ‘sale’, or as the case may be ‘deemed manufacture’ or ‘deemed sale’) and is liable to service tax. GST now proposes to combine these different taxation aspects contained in the Constitution of India, into a one broader ‘all inclusive concept’ called ‘supply’.

Concept of Job Work

Job-work industry constitutes a significant sector in Indian economy. It’s an indispensable arm of our industrial sector. “Job work” basically includes outsourced activities which may or may not result into manufacture. The person undertaking the job work is called job worker. The job worker always works under the instructions of the principal manufacturer and exercises his labour over the inputs or material belonging to his principal. Where exercise of labour results in manufacture of goods, excise duty becomes applicable and in other cases, service tax comes into play. Some job works involve transfer of material from job-worker to principal manufacturer in the course of execution of the work in which case VAT/CST may get attracted. In some cases, a job worker provides pure labour and entire inputs/raw materials are provided by the principal manufacturer.

The impact of GST on Job work transactions can be better understood, only if the existing taxation aspects qua such transactions as mentioned above are first noted. Hence, in this article, Authors thought it fit to first explain the existing valuation provisions governing job work transactions in brief and will then attempt to throw some light on valuation provision under the proposed GST regime and related issues. This will enable to understand whether there is any deviation in GST vis-a-vis past laws.

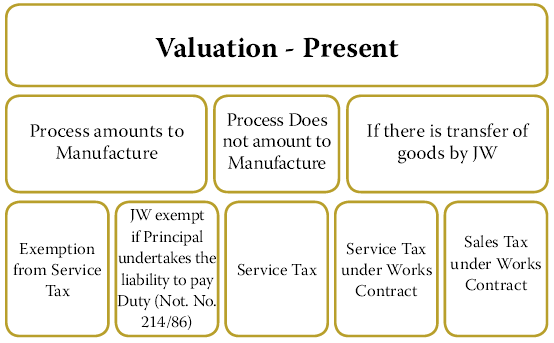

Valuation Provisions under Central Excise Act

When activities undertaken by the job-worker result into manufacture of goods, the levy of central excise duty becomes applicable. In Ujagar Prints, etc. vs. UOI 1988 (38) ELT 535, Hon’ble Supreme Court held that, the assessable value of the goods in the hands of job-worker, would include value of the goods supplied to the job-worker for processing plus the value of the job-work done plus manufacturing profits and manufacturing expenses whatever would be included in the price at the factory gate but not any other subsequent profit or expenses. The Court reiterated that the value for the assessment under Section 4 of the Act will not be the processing charge alone but the intrinsic value of the processed goods which is the price at which the goods are sold for the first time in the wholesale market. Subsequently with regard to the same assessee, in 1989 (39) ELT 493, Supreme Court also clarified that, trader’s profit (i.e. Customers’ profit who got the goods processed) is not to be included because those would be post manufacturing profits.

Subsequently Rule 10A was inserted in the Central Excise Valuation (Determination of Price of Excisable Goods) Rules, 2000 w.e.f.01.04.2007 to deal with cases of excisable goods produced or manufactured by a job worker. Rule 10A is founded on the principle that, the valuation has to be done by taking into consideration the value of excisable goods so produced as a result of job-work and that would be the transaction value of the goods sold by the principal manufacturer (at the time of removal of goods from the factory). The vires of Rule 10A were challenged before Hon’ble Bombay High Court in the case of Hyva (India) Pvt Ltd vs UOI 2015(327) ELT 41. Upholding the validity of the said rule the High Court held as under:

“If the job worker means a person engaged in the manufacture or production of goods on behalf of the principal manufacturer from any inputs or goods supplied by the said principal manufacturer or by any person authorised by him, then, it is clear

The job work operations not amounting to manufacture would be regarded as service. If the ultimate value of job-work is included in the value of final product on which principal manufacturer is liable to pay excise duty, in such case, the said job work operations are exempted from levy of service tax.

that the job work or the effort which has been taken by the job worker for and on behalf of the principal manufacturer enables the principal manufacturer to sell the completed product or finished goods. It cannot be, therefore, that the Legislature must only take the price which parties like the petitioners charge for the job work to M/s. Tata Motors Limited (sic principal manufacturer). For the purpose of computation or calculation of the duty liability of the parties like the petitioners there is nothing erroneous if the Legislature takes into consideration and account the price at which the principal manufacturer sells the product or goods to the buyer. That is nothing but a measure of the tax. In other words, that is how the tax has to be computed and measured. Such a provision does not alter or change the character or nature of the duty or tax. The tax or duty remains a tax or duty on production or manufacture of goods. Insofar as its measure is concerned, the Legislature thought it fit and in its wisdom to quantify the duty liability of parties like the petitioners on the price which the finished product or goods command in the market. That would be the true measure of the tax according to the Legislature.”

Presently, under Notification No.214/86 dtd.25- 03-1986, job-workers are exempted from payment of duty on goods manufactured in a factory as job work and used in relation to manufacture of final products on which duty of excise leviable whether in whole or in part, if the principal manufacturer gives an undertaking that, the said goods will be used in or in relation to the manufacture of the final products and also undertakes the responsibilities of discharging the liabilities in respect of Central Excise duty leviable on such final products.

Valuation for the Purposes of Service Tax

The job work operations not amounting to manufacture would be regarded as service. If the ultimate value of job-work is included in the value of final product on which principal manufacturer is liable to pay excise duty, in such case, the said job work operations are exempted from levy of service tax. This exemption is granted in the same lines as Notification No.214/86 mentioned above. However, if the job-work processing does not amount to manufacture and the final product is exempted from duty/liable to nil duty, then job worker would become liable to pay service tax on his services. There are no special provisions governing valuation of job-work activities. If the job-work transactions are in the nature of pure services, there will be no difficulty in valuation as the entire job work charges would be treated as assessable value for the purpose of levy of service tax. However, in some cases, the job-worker may use own material to process the goods received from the principal manufacturer. It’s now a settled position of law that addition or application of minor items by job worker would not detract it being a job work [Prestige Engineering (India) Ltd. v. CCE, Meerut 1994 (73) ELT 497 (SC)]. In such cases, the job-work may be regarded as a ‘works contract’ and shall be valued accordingly.

Traditionally works contract are the service contracts, however, for taxation purpose, it’s regarded as a transaction involving simultaneous provision of service and sale of goods. Service portion is liable to service tax and value of material transferred is liable for sales tax /VAT. Prior to Negative List, the issue as to whether the value of goods supplied by the principal manufacturer should also be included in the assessable value of works contract service, was put to rest by Larger Bench decision in the case of Bhayana Builders (P) Ltd’s [2013 (32) STR 49]. In this case, while interpreting the Explanation inserted by Notification No.4/2005-ST in Notification No.15/2004-ST (which purports to explain the meaning of expression “gross amount charged”, to include the value of goods and materials supplied or provided or used by the provider of construction service for providing such service), the Larger Bench of Hon’ble Tribunal held that, implicit in this legislative architecture (of Section 67) is the concept that any value to constitute a consideration, whether monetary or otherwise should have flown or should flow from a service recipient to a service provider and should accrue to the benefit of the later; and that this is a precondition of taxability under Section 67. Accordingly, Tribunal held that, goods and materials, supplied/provided/used by the service provider for incorporation in the construction, which belong to the provider and for which the service recipient is charged towards the value of such supply/provision/ use and the corresponding value whereof was received by the service provider, to accrue to his benefit, would alone constitute the gross amount charged and that “Free supplies”, incorporated into construction (cement or steel for instance), even on extravagant inference, would not constitute non-monetary consideration remitted by service recipient to service provider for providing service, particularly since no part of goods and materials so supplied accrues to or is retained by service provider. However, Tribunal also categorically stated that, there is nothing to prevent the inclusion of value of free supplies into the gross amount charged for valuation of the taxable service. If such intention is to be effectuated, the phraseology must be specific and denuded of ambiguity.

Valuation Provisions under Sales Tax/VAT

The levy of Sales Tax/VAT is on ‘sale’ of goods. Hence job work transactions involving pure labour would not attract levy of sales tax/VAT. When materials are supplied by principal manufacturer to job worker for the purposes of job-work, there is no sale of such goods and consequently, levy of sales tax is not attracted. In case of inter-state transfers, principal manufacturer is required to follow certain procedures for the purpose of declaring such transfers as “otherwise than for sale”. Similarly, when job-worker returns the goods to principal manufacturer, after the job work is complete, he is not liable for payment of VAT/sales tax, since such transfers would not be regarded as sale. However, if the job-work results in transfer of material from job-worker to principal manufacturer, value of material so transferred attracts VAT. Every State has its own valuation rules for determining the value of material so transferred in the course of job-work processing.

Under the model GST Law, concept of supply is explained in Section 3. It includes all forms of supply of goods and/or services such as sale, transfer, barter, exchange, license, rental, lease or disposal.

Valuation under GST Model Law

Under the model GST Law, concept of supply is explained in Section 3. It includes all forms of supply of goods and/or services such as sale, transfer, barter, exchange, license, rental, lease or disposal. Ordinarily, ‘supply’ shall become subject matter of levy only when (i) such supply is of goods and/ or services and (ii) is made or agreed to be made in the course of or furtherance of business and (iii) is made for a consideration. However, as per section 3 read with Sr.No.5 of Schedule I, any supply of goods and/or services by a taxable person to another taxable or non-taxable person in the course of or furtherance of business would be regarded as ‘supply’ even if such supply is without any consideration. The supply of goods by a registered taxable person to a job-worker in terms of Section 43A of the Model GST Act is carved out as an exception from Sr.No.5. Section 43A, inter alia, provides a special procedure for removal of goods involved in job-work transactions, without payment of duty. The benefit of section 43A can be granted by the Commissioner only by a special order. Hence, it would be interesting to see whether such special order would be a blanket permission, specifying certain conditions and procedure, upon fulfillment of which all the taxable person are automatically entitled to benefit of section 43A, or this order shall be issued qua every taxable person separately.

Following cases are contemplated in section 43A where goods can be permitted to be removed without payment of duty.

(i) goods sent by principal to job-worker for job-work,

(ii) goods sent from one job-worker to another job-worker for further job work

(iii) bringing back the goods from job-worker to any place of business of the principal ( with an intention to supply therefrom)

There are no specific valuation provisions governing the valuation of Job-work under model GST law. “Job-work” is defined in section 2(62) to mean undertaking any treatment or process by a person on goods belonging to another registered person. Under Schedule–II, any treatment or process which is being applied to another person’s goods is regarded as a supply of service. Further, ‘works contract’ including transfer of property in goods (whether as goods or in some other form) involved in the execution of works contract is also regarded as service. Therefore, it appears that, under GST, for taxation purposes, job-work operations will be regarded as ‘supply of service’, even if they involve transfer of property in goods. Consequently, the valuation provisions contained in Section 15 read with Model GST Valuation Rules would equally applicable to job-work transaction as they would apply to provision of other services.

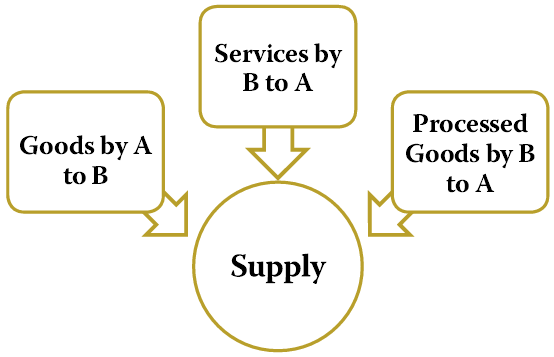

Another significant aspect that may be relevant in determining the valuation is that, in Job work transaction, there will be minimum two supplies from Job-worker to the principal namely (i) supply of services for consideration which will be in the nature of job-work charges and (ii) supply of processed goods for which there will be no consideration (since this would be only return of goods back to the principal).

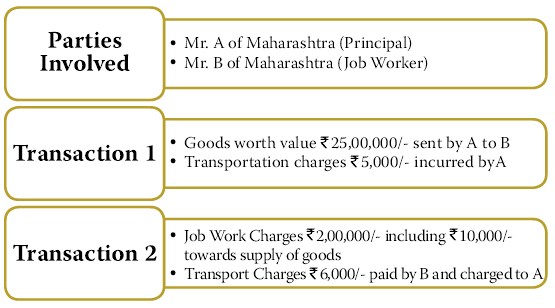

This can be explained by way of an example:

‘A’ of Maharashtra sent goods of Rs. 25,00,000 to ‘B’ of Maharashtra for the purpose of Job-work. ‘A’ incurs transportation expenses of Rs. 5000. ‘B’ of Maharashtra did the Job-work operation on the goods received from ‘A’ and charged Rs. 2,00,000 as his job-work charges. In the said amount of Rs. 2,00,000, there is also included use of material amounting to Rs.10,000 procured by the job-worker and used in the job-work operation. Thereafter he transported goods back to ‘A’ at his another place of business in Gujarat. For transportation ‘B’ also charged Rs. 6000 to ‘A’ as transportation charges.

In this example, there are various supplies as under:

(a) supply of raw goods from ‘A’ to ‘B’

(b) supply of service from ‘B’ to ‘A’ – ‘Job work’ and/ or ‘Transportation’

(c) supply of processed goods from ‘B’ to ‘A’

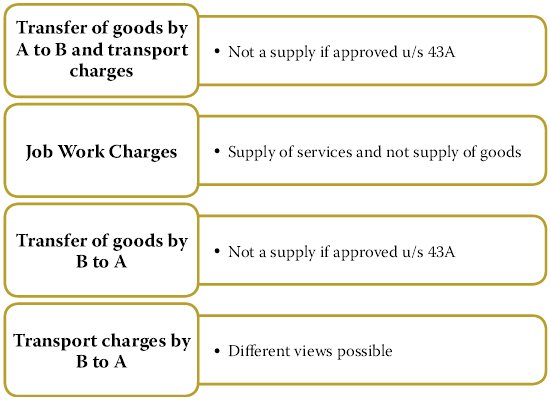

Assuming that transaction is covered within the ambit of section 43A, there will be no liability to pay taxes for supply of raw material from ‘A’ to ‘B’ and supply of processed goods from ‘B’ to ‘A’. However, supply of service i.e. job-work would attract tax. This appears to be a diversion from current service tax and excise provisions, where job-workers are exempted from Central excise duty as well as Service tax on their job-work charges, if the principal manufacturer pays duty on final product, the next question is what would be the value of service for the purpose of levy of tax. As per section 15, the value of supply of goods and/or services shall be the transaction value. “Transaction value” would mean the price actually paid or payable for the said supply services where the supplier and the recipient of supply are not related and the price is the sole consideration for the supply. Hence, in the present case, Rs. 2,00,000 would be treated as value of service. Although, it includes materials worth Rs. 10,000, still the entire supply including value of material would be treated as services. Under section 15 (2)(a), the law provides that, any amount that the supplier is liable to pay in relation to such supply, but which has been incurred by the recipient of the supply and not included in the price actually paid or payable for the goods/services would also be included in the transaction value. Rule 15(2)(e) provides that, the incidental expenses, such as, commission and packing, charged by the supplier to the recipient of a supply, including any amount charged for anything done by the supplier in respect of the supply of goods and/or services at the time of, or before the delivery of the goods or supply of services are also treated as a part of transaction value. Hence the questions arise as to whether, a sum of Rs. 5000 incurred by ‘A’ (but not charged to ‘B’) and a sum of Rs. 6000 incurred by ‘B’ and charged to ‘A’ as transportation charges will also form part of transaction value of job work under Rule 15 (2)(a) and Rule 15(2)(e) respectively?

As regards, sum of Rs. 25,00,000 and Rs. 5000, possible answer could be that, it would not have any implications due to operation of section 43A. However, as a corollary, these items would have an impact where the benefit of section 43A is not available. As regards, inclusion of Rs. 6,000, one view can be that, these expenses are incidental to the supply of job-work service and hence would be included in its transaction value, whereas the other view can be that, these expenses are incidental to supply of processed goods from ‘B’ to ‘A’ and hence would not be liable to tax as per section 43A of the Act. The third view may be that, this value is towards supply of different service from ‘B’ to ‘A’ namely transportation service, and is therefore liable to tax, in accordance with Place of Supply of service as applicable to services relating to transportation of goods, as contained in Section 6(9) of Model IGST Act. As per the said provision, the place of supply of service shall be location of ‘A’. As per section 2(64) where a supply is received at a place of business for which registration has been obtained, the location of recipient of service shall mean the location of such place of business. Therefore, in this case, location of ‘A’ shall be Gujarat. Therefore, in the present case, where supply of job work would be liable to CGST/SGST (being within the same State), the supply of transportation service provided by B to A, may be liable for IGST. This issue may be more complicated when there would be composite supplies. A ‘composite supply’ is defined in section 2(27) to mean a supply consisting of (a) two or more goods, (b) two or more services or (c) a combination of goods and services, provided in the course or furtherance of business, whether or not the same can be segregated. Therefore, a question may arise, as to if, in the present case, Job-work service and transportation service are regarded as one composite service, whether entire value will attract CGST & SGST or not? Another question may also arise, as to if supply of job-work service and supply of goods by Job-worker to Principal is also regarded as a part of composite supply, whether, entire transaction would fall within the operation of section 43A ?

The impact of place of supply & composite supply becomes relevant in valuation because, if the transportation charge is treated as a part of supply of job-work service, then Maharashtra State Authorities may demand SGST on transportation charges of Rs. 6,000 notwithstanding that IGST has already been paid on such amount. Similarly, on the other hand, if it is regarded as part of supply of goods, then ‘B’ may take a stand that, no tax is payable on it, by virtue of operation of Section 43A of the Act.

The other provisions contained in Rule 15 which are also to be taken into account for the purpose of Valuation of Job-work Transactions are as under:

- Royalties and license fees related to the supply of services (i.e. job–work operations) that, the recipient of supply must pay, either directly or indirectly, as a condition of the said supply is also to be included in transaction value, to the extent that such royalties and fees are not included in the price. Therefore, if ‘A’ paid certain technology transfer fees to ‘C’, so that ‘B’ can use the said technology in the job-work operation that he is performing for ‘A’, the value of such technology transfer fee may also be included in transaction value of job-work services, unless B is in a position to prove that, the impact of such technology transfer fees has already been considered in Rs. 2,00,000.

- Further, any reimbursable expense or cost incurred by or on behalf of the supplier and charged in relation to supply of services would also form a part of transaction value of service. Therefore, for the purpose of job-work, if any material is procured by ‘A’ on behalf of ‘B’, cost of which is recovered separately from ‘B’ , then such cost may also be included in the value of service, unless B is in a position to prove that, the impact of cost of such materials has already been considered in Rs. 2,00,000.

- No deduction from transaction value is allowed for any incentive/discount given by ‘B’ to ‘A’ after the supply has been effected, unless such discount is offered under the established agreement and is known before or at the time of supply and can be traced qua invoice raised for particular supply. Similarly, any discount given prior to supply shall not qualify for deduction from value, unless, such discount is allowed in the normal trade practice and has been duly recorded in invoice.

Besides Rule 15, the other provisions in model GST Act applicable to job-work transaction also throw some light on the valuation of job-work contemplated under GST regime. Section 19 deals with registration under the Act and enlists cases liable for registration in Schedule III. As per the said schedule, every supplier whose aggregate turnover

in a financial year exceeds Rs. 9 lakhs is liable to be registered. However, explanation 2 there under specifically provides that, supply of goods by a registered job-worker shall be treated as supply of goods by the principal referred to in section 43A and the value of such goods shall not be included in the aggregate turnover of such registered job-worker. Section 16A of the Act provides that, credit in respect of inputs sent by principal to job-work shall be available to such principal, if the said inputs/capital goods after completion of job-work are received back by him within a specified period of their being sent out. Credit is also available if such inputs/

The study of implications under GST law on the aspects related to valuation of job-work transactions is very crucial having regard to various issues raised above and wherever there is a scope for ambiguous situation, necessary clarification is required to be engrafted in the GST Act, in order to save the job work industry from possibility of litigation in future.

capital goods are directly sent to job-worker without first bringing the same into the premises of principal. Needless to say that such credit is available subject to fulfillment of certain conditions and procedures that may be prescribed in this regard. Section 43A also provides that, responsibility for accountability of the goods including payment of tax thereon shall lie with the principal. Therefore, scheme of the law appears to be that as regards, tax applicable on the supply of final/processed product, the value is to be assessed in the hands of principal and job-workers will be excluded provided they are registered and follow such procedures as may be prescribed under the law.

To conclude, the study of implications under GST law on the aspects related to valuation of job-work transactions is very crucial having regard to various issues raised above and wherever there is a scope for ambiguous situation, necessary clarification is required to be engrafted in the GST Act, in order to save the job work industry from possibility of litigation in future.

Source:- http://idtc-icai.s3.amazonaws.com/download/knowledgeShare16-17/Valuation-and-Job-Work-under-GST.pdf

Author Bio