Amit Jindal

Introduction

Audit under GST is the examination of records, returns and other documents maintained by a registered dealer. The aim is to verify the correctness of Turnover declared, Taxes paid, Refund claimed and input Tax Credit availed by an assessed as per provisions under GST along with is to assess the auditee’s compliance with the provision of GST Act and Rules.

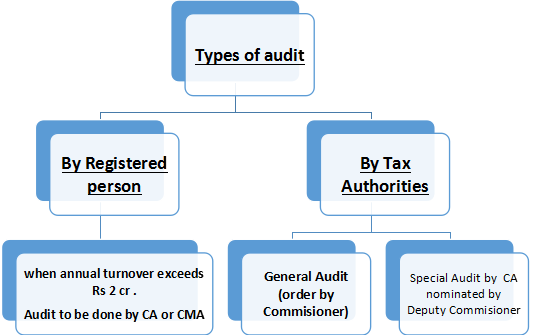

Types of Audit

There are three types of Audit prescribed under GST laws which are graphically presented as below. We will discuss one by one from next page onwards.

Audit by registered dealer

Every registered dealer whose aggregate turnover during a financial year exceeds Rs 2 crore has to get his accounts audited by a CA or a CMA and shall furnish a copy of audited annual account and a reconciliation statement, duly certified in Form GSTR-9C. Due date for filing GSTR-9, GSTR-9A and GSTR-9C which was previously 31st March, 2019 has now been extended till 30th June 2019 by CBIC for FY 2017-18.

The Aggregate Turnover is PAN based and therefore for calculating turnover for the purposes of 2 crore limit, the turnover of all the registered place of business shall be considered. Also, for Financial Year 2017-18, GST was applicable for only 9 months whereas as per GST laws the turnover shall be considered for whole financial year. However, there is no clarification from the government received till date, therefore turnover for the whole financial year should be counted which would also include the first quarter of 2017-18.

To undertake an effective audit under GST, one needs to ensure the periodical review of the records and returns filed by the registered dealer. The period for review may be opted depending upon the size of entity, turnover and volume of transaction. For example, if registered dealer needs to file GSTR-1 on quarter basis, then the periodic review may be undertaken quarterly and if GSTR-1 is filed monthly then monthly review may be undertaken. A periodic review includes,

1. Classification of service or good

2. Correct determination of taxable turnover

3. Review of rates of tax

4. Proper application of relevant notifications or circular

5. Government orders and adherence to the tax compliances

Further, a regular and effective periodic review would assist the registered dealer in the departmental audits and investigation. Naturally, any levy of additional tax due to non-compliance would result in taxes plus consequential interest and penalty.

Audit by Tax Authorities

General Audit: The commissioner or on his order a proper officer may conduct an audit of any registered dealer by giving a notice at least 15 days in advance in ADT-01. The commissioner may require the registered person to make available the necessary information and documents for timely completion of audit. The proper officer verifies the documents on the basis of which books of account and returns and statement has been furnished. Basically the department verify below mentioned area,

1. The correctness of the turnover declared

2. Exemptions and deductions claimed

3. Rate of tax applied on goods or services

4. Input tax credit availed and utilized

5. Refund claimed

6. Other relevant issues

Section 71 of the Act gives power to such proper officer to have the access to any place of business of the registered person and to inspect books of account, documents, computers etc. and the person in charge of place shall provide the required information or documents to the proper officer on demand within 15 days of such demand.

Such audit shall be completed within 3 months from the date of commencement of an audit. However, a commissioner can extend the period of such a GST audit further by six months with valid reasons which must be recorded in writing.

It is pertinent to note that for the period April, 2017 to June, 2017 the Audits are taken up by the department under Service Tax and the Service Tax department along with verification of records of assessee, is also verifying the transitional provisions of GST . Therefore, the department is also verifying the information filed in Form GST Tran-1.

On audit completion, information is required to be provided to the registered person including the findings during the audit in FORM GST ADT-02 within thirty days of conclusion of the audit.

Special Audit: Any officer not below the rank of Assistant Commissioner may direct any registered person in whose case any scrutiny, inquiry, investigation or any other proceedings pending, in Form ADT-03 to get his account audited by a Chartered Accountant or a Cost Accountant appointed by such officer.

It is worth-noting that the Special Audit would be conducted only when the officer is of opinion that:

– Value has not been correctly declared

– Credit availed is not within the normal limits

Therefore, an Assistant Commissioner who concludes an opinion on the above two aspects, after the commencement and before the completion of any scrutiny, inquiry, investigation or any other proceeding, may direct the registered person to get his account audit by a Chartered Accountant or Cost Accountant appointed by him.

The Chartered Accountant or the Cost Accountant so appointed shall submit the audit report, mentioning the specified particulars therein, within a period of 90 days, to the Assistant Commissioner in FORM GST ADT-04. The period may further be extended by 90 days, if the registered person makes an application to the Assistant Commissioner by providing sufficient reason thereof.

Further, the registered person shall be given a proper opportunity of being heard in case any material on the basis of Special Audit is used in any proceeding against him.

General GST Audit Checklist:

The following are the mandatory GST Audit checklist that requires strict compliance:

1. Checking of GSTR 3B in relation to GSTR 1 & GSTR 2A: –Auditors need to reconcile the GSTR 3B with GSTR 2A to make sure that the organization would not claim extra tax credit. Recipient could claim excessive input tax credit. Therefore, it is compulsory for him to make a payment of interest @ 24% on the excess tax amount. Also, when the GST authorities come to know about the data gaps between GSTR 3B and GSTR 2A and consequently the tax payers might have to pay the interest and penalty.

2. Amendment in GST Return: When the auditor comes to know about any data gaps between GSTR-3B and GSTR-1, he would recommend the management to make amendment of the invoices at summary levels in GSTR-1.

3. Checking particulars of invoice:It is very clear that there are specific rules related to the details in the invoices. If the format of the invoice varies, the auditor shall advise the management to make amendment of the invoice and include the requirements of the GST rules.

4. Reversal of input tax credit for non-payment in 180 days:At this stage the GST auditor has to check the following details:

a) Difference between invoice date and date of payment. And this should not exceed 180 days.

b) The amount of payment needs to remain equal with invoice amount and GST. If the payment amount is less than invoice amount plus GST, the input tax credit to the extent of short payment should get reversed.

5. Review of e-way bill: E –Way is mandatory documents to be filed online before or during the movement of goods worth more than Rs. 50,000/- (If it is inter-state supply). Moving goods without an invoice and E-Way Bill is prone to penalty and confiscation of goods and vehicle carrying such goods as well.

Therefore, an Auditor shall ensure that proper E-Way Bill has been generated before the movement of goods. Also, the value mentioned in E-Way Bill is as per the invoice. During the periodical review, auditors need to ensure that any invoice having value more than Rs. 50,000/- (In case of inter-state supply) are properly supported with valid E-Way Bill.

6. Cross-checking the stock lying with job-workers on 30th June, 2017:A register person may send any inputs or capital goods to a job worker without payment of tax subject to the condition that the Input or Capital Goods so sent shall be brought back to his place of business within one year in case of Input and within three years in case of Capital Goods. In case of goods lying with job workers on 30th June 2017, these need to be brought back within six months i.e. before 31st December, 2017. Therefore, the auditor shall ensure that all the goods which were lying with the job workers on 30th June, 2017 are returned back to the registered place of business of the dealer before 31st December, 2017. Also, goods (other than capital goods) sent for job work after 30th June, 2017 shall be brought back within one year and in case of capital goods, the same shall be brought back within three years.

About the Author

Author is Amit Jindal , ACA working as Manager- Tax Compliances with Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing a business in India.

Thanks

It is really a nice article Mr. Amit.