Manual on Transition Form GST TRAN – 1

How can I file transition form GST TRAN – 1?

Every registered person who is eligible to take credit of eligible duties and taxes paid under existing laws in respect of input or input services or capital goods in his/her Electronic Credit Ledger, needs to file a declaration in Form GST TRAN – 1 within the specified period i.e. 01.10.2022 to 30.11.2022 as per the judgement made by the honorable Supreme court.

To file transition form GST TRAN – 1, perform the following steps:

1. Login and Navigate to Transitions Forms > TRAN – 1 page

1.1. Access the www.gst.gov.in. The GST Home page is displayed.

1.2. Login to the GST Portal with valid credentials.

1.3. Click the Services > Returns > Transition Forms command.

1.4. The Transition Forms page is displayed. The tabs of transition forms TRAN 1/ TRAN – 2/ Upload Documents are visible in the top band. Tiles of Form TRAN – 1 will be visible by default.

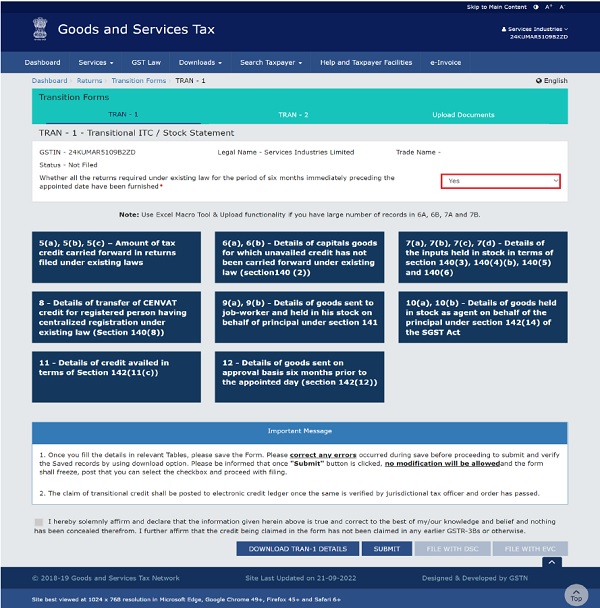

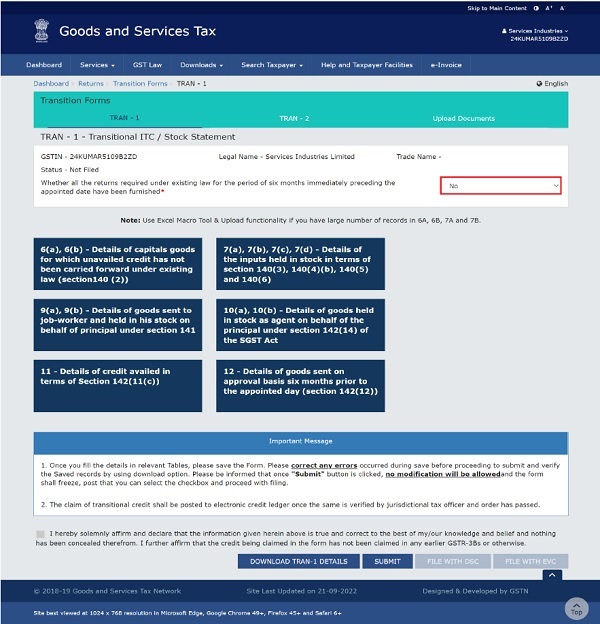

For the question Whether all the returns required under existing law for the period of six months immediately preceding the appointed date have been furnished, select the Yes or No option.

1.4. (a) When the taxpayer selects Yes option,

1.4. (b) When the taxpayer selects No option, then table/tile number 5 and 8 will be disabled.

2. Enter details in various tiles

There are a number of tiles representing different Tables to enter relevant details. Click on the tile names to know and enter related details:

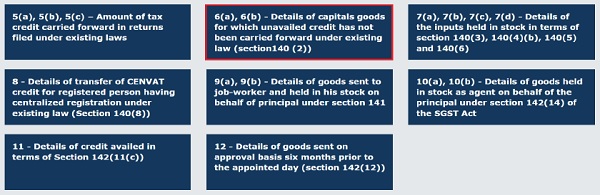

- 5(a), 5(b), 5(c) – Amount of tax credit carried forward: To provide details of tax credit to be carried forward from the last return under existing laws to GST regime.

- 6(a), 6(b) – Details of capitals goods for which un-availed credit has not been carried forward: To provide details of capital goods for which unavailed credit is to be carried forward.

- 7(a), 7(b), 7(c), 7(d) – Details of the inputs held in stock: To provide summary details of the inputs held in stock and input contained in semi-finished goods or finished goods held in stock on the appointment date. For 7(b) – To provide details of eligible duties or taxes paid in respect of inputs or input services received on or after appointment date but duty or tax has been paid under existing law

- 8 – Details of transfer of CENVAT credit for registered person having centralized registration: To provide summary details to transfer CENVAT credit admissible as CGST credit to any of the newly registered persons under GST having same PAN for which the centralized registration was obtained under the existing law.

- 9(a), 9(b) – Details of goods sent to job-worker and held in his stock on behalf of principal under section 141: To provide summary details of goods sent to job-worker and held in stock by the Job-worker on behalf of principal by the principal and agent.

- 10(a), 10(b) – Details of goods held in stock as agent on behalf of the principal under section 142: To provide summary details of goods held in stock as agent on behalf of the principal under section 142(14) of SGST Act and the admissible credit to the agents on such stock.

- 11 – Details of credit availed in terms of Section 142(11(c)): To provide summary details of tax paid under Existing Act and the allowable credit under GST on supplies which were taxable under both existing VAT and Service tax regime and also taxable in GST regime.

- 12 – Details of goods sent on approval basis six months prior to the appointed day (section 142(12)): To provide summary details of goods sent on approval basis six months prior to the appointed day (section 142(12)).

5(a), 5(b), 5(c) – Amount of tax credit carried forward

To provide summary details of the amount of tax credit carried forward in the returns filed under relevant earlier laws and admissible as GST credits, perform the following steps:

- The Registration Numbers under earlier laws mentioned in any table of TRAN 1 need to be the same as that

declared by the taxpayer in their enrolment/registration form otherwise system will throw validation error. - If the taxpayer has failed to furnish any registration number of earlier laws, he may use the non-core registration amendment facility to declare it in the registration details and subsequently file TRAN 1.

1. Click the 5(a), 5(b), 5(c) – Amount of tax credit carried forward tile.

The 5(a)Credit Carried Forward – Central Tax – Summary page is displayed.

5(a) Central Tax Tab:

1.1. The Central Tax tab is selected by default and in the absence of any previous records the screen will show no records added as can be seen in the screenshot below. Please Click the ADD DETAILS button to add details.

The Credit Carried Forward (Central Tax) – Add page is displayed.

1.1.1. In the Registration no. under existing law (Central Excise and Service Tax) field, enter the registration number under existing law (Central Excise and Service Tax).

1.1.2. In Tax period to which the last return filed under the existing law pertains select tax period from the drop-down list.

1.1.3. In Date of filing of the return select date of filing of last return using the calendar.

1.1.4. In the Balance CENVAT credit carried forward in the said last return field, enter the balance CENVAT credit carried forward in the said last return.

1.1.5. In the CENVAT Credit admissible as ITC of central tax in accordance with transitional provisions field, enter the CENVAT credit admissible as ITC of central tax in accordance with CGST Act provisions.

Please add reclaim of CENVAT reversal as per CGST rule 140 (9).

1.1.6. Click the SAVE button to save the details.

Note: Please ensure that you save the details by clicking the save button in the bottom right corner else the details would be lost

You will be directed to the previous page and a save successful message is displayed.

NOTE 1: Click the pen icon (…) under the Actions column to edit the inputs given in various headers.

NOTE 2: Click the delete icon (…) to erase the inputs given in various headers.

1.1.7. Click the BACK button to go back to the Transition Forms page.

Note: The system will validate the entries and if there is any validation error, system will show status as Processed with Error.

If the entry is processed with error, please click the pen icon (….) to edit the fields. The nature of validation error can be seen on the top portion of screen as depicted below:

Table 5(a) Credit Carried Forward- Central tax is saved successfully.

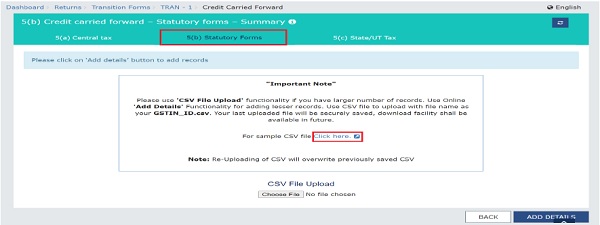

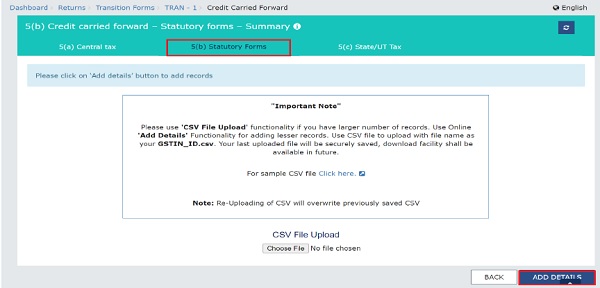

Table 5(b) Statutory Forms Tab:

1.2. Click the 5(b) Statutory Forms tab.

Note: You can use ‘CSV File Upload’ functionality if you have larger number of records. Use Online ‘Add Details’ functionality for adding lesser records.

CSV File Upload:

Download the sample CSV file:

1.2.1. Click the Click here link to download the same CSV file.

1.2.2. Click the Download link.

1.2.3. Once downloaded, open the CSV file, fill the details and save it.

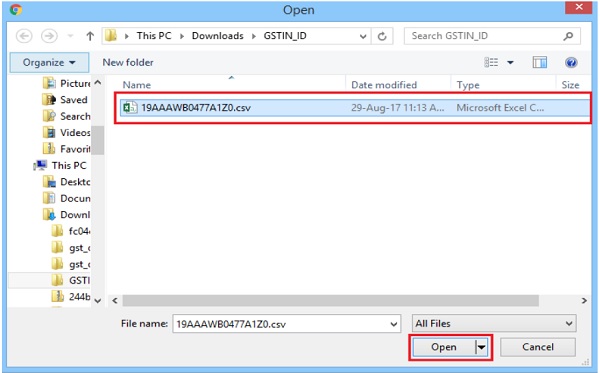

Note: Use CSV file to upload with file name as your GSTIN_ID.csv. Your last uploaded file will be securely saved.

1.2.4. Click the Choose File button.

1.2.5. Select the CSV file and click the Open button.

A success message is displayed that the CSV file is saved successfully.

Add Details:

1.2.6. Click the ADD DETAILS button to add a new invoice.

Note: You can use CSV File Upload’ functionality if you have larger number of records. Use Online ‘Add Details’ functionality for adding lesser records.

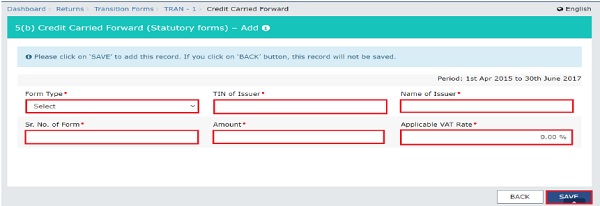

The Central Carried Forward (Statutory Forms) – Add page is displayed.

1.2.7. Select the Form Type from the drop-down list.

1.2.8. In the TIN of Issuer field, enter the TIN number of the issuer of the statutory form.

1.2.9 In the Name of Issuer field, enter the name of the issuer of the statutory form

1.2.10 In the Sr. No. of Form field, enter the serial number of the statutory form issued.

1.2.11 In the Amount field, enter the total amount as declared in that statutory form.

1.2.12 In the Applicable VAT Rate field, enter the applicable VAT rate on those transactions

1.2.13 Click the SAVE button to save the details.

Note: The system will validate the entries and if there is any validation error, system will show status as Processed with Error. On clicking the Edit button against that entry, the nature of validation error can be seen on the top portion of screen.

You will be directed to the previous page and a success message is displayed.

NOTE 1: Click the pen icon (….) under the Actions column to edit the inputs given in various headers.

NOTE 2: Click the delete icon ( ) to erase the inputs given in various headers.

1.2.14. Click the BACK button to go back to the Transition Forms page.

Table – 5(c) State/UT Tax Tab:

1.3. Click the State/UT Tax tab. Click the ADD DETAILS button to add details.

The Credit Carried Forward (State/UT Tax) – Add page is displayed.

1.3.1 In the 1. Registration No. in existing law field, enter the VAT registration No. in the existing law.

1.3.2 In the 2.Balance of ITC of VAT [and Entry Tax] in last return field, enter the balance amount of ITC of VAT and entry tax carried forward in the last return.

1.3.3 In the 3. Turnover for which C Forms Pending field, enter the turnover for which C Forms is pending for the period 1st April 2015 to 30th June 2017.

1.3.4 In the 4. Difference tax payable on pending C-Formsat (3)field, enter the amount for the difference tax payable on pending C-Forms.

1.3.5 In the 5. Turnover for which F-Forms Pending field, enter the turnover for which F-Forms is pending for the period 1st April 2015 to 30th June 2017.

1.3.6 In the 6. Difference tax payable on pending F-Forms at (5) field, enter the amount for difference tax payable on pending F-Forms.

1.3.7 In the 7. ITC reversal relatable to C-Forms at (3) and F-Forms at (5) field, enter the amount for ITC reversal relatable to C-Forms and F-Forms done earlier as per provisions of existing laws while reporting in the related returns.

1.3.8 In the 8. Turnover for which H/I-Forms Pending field, enter the amount of turnover for which H/I-Forms is Pending for the period 1st April 2015 to 30th June 2017.

1.3.9 In the 9. Difference tax payable on pending H/I-Forms at (8) field, enter the amount of differential tax payable on pending H/I-Forms.

1.3.10 In the 10.Transition ITC [2-(4+6+7+9)] field, enter the amount of Transition ITC of State tax admissible as ITC under SGST Act.

1.3.11 Click the SAVE button to save the details.

Note: The system will validate the entries and if there is any validation error, system will show status as Processed with Error. On clicking the Edit button against that entry, the nature of validation error can be seen on the top portion of screen.

NOTE 1: Click the pen icon (….) under the Actions column to edit the inputs given in various headers.

NOTE 2: Click the delete icon (…) to erase the inputs given in various headers.

1.3.12 Click the BACK button to go back to the Transition Forms page.

Table 6(a), 6(b) – Details of capitals goods for which un-availed credit has not been carried forward

To provide summary details of capitals goods for which credit has not been availed under relevant earlier laws and are admissible as credit under GST, perform the following steps:

2. Click the 6A, 6B – Details of capitals goods for which unavailed credit has not been carried forward tile.

The Capital Goods – Summary page is displayed.

Download Full Text of Manual on Transition Form GST TRAN – 1