Procedure regarding procurement of supplies of goods from DTA by Export Oriented Unit (EOU) / Electronic Hardware Technology Park (EHTP) Unit / Software Technology Park (STP) Unit / Bio-Technology Parks (BTP) Unit under deemed export benefits under section 147 of CGST Act, 2017 is described vide Circular No. 14/14 /2017-GST, 6th November, 2017

Let us discuss & decode the provisions in this article

Deemed Exports

As per Sec 2(39) “deemed exports” means such supplies of goods as may be notified under section 147;

Sec 147 of CGST Act: The Government may, on the recommendations of the Council, notify certain supplies of goods as deemed exports, where goods supplied do not leave India, and payment for such supplies is received either in Indian rupees or in convertible foreign exchange, if such goods are manufactured in India.

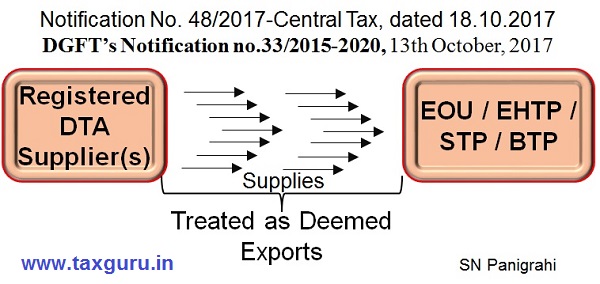

Supplies to EOU Treated as Deemed Exports

Government vide Notification No. 48/2017-Central Tax, dated 18.10.2017, specified certain categories of supplies as Deemed Exports.

In Sr. Number 3 of the Table in said notification supply of goods by a registered person to Export Oriented Unit is treated as Deemed Exports. Further in the explanation to the notification, clarified that “Export Oriented Unit” means an Export Oriented Unit or Electronic Hardware Technology Park Unit or Software Technology Park Unit or Bio-Technology Park Unit approved in accordance with the provisions of Chapter 6 of the Foreign Trade Policy 2015-20.

In similar lines DGFT’s Notification No. 33/2015-2020, 13th October, 2017

was issued. Accordingly Para 6.01(d) of FTP is amended to read as under

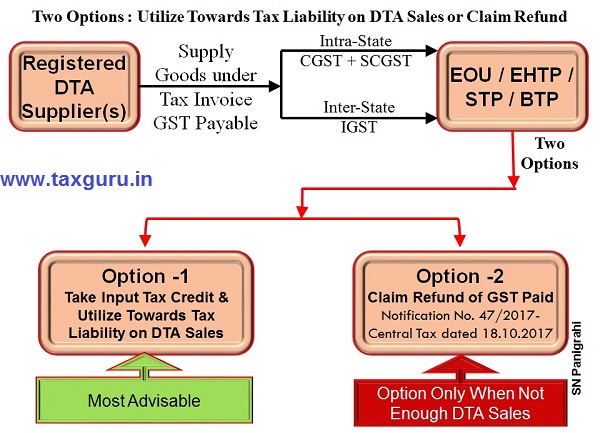

(iii) The procurement of GST goods from DTA would be on payment of applicable GST taxes. The EOUs can procure excisable goods, falling in Fourth Schedule of Central Excise Act, from DTA without payment of applicable excise duty. The refund of GST taxes for supply from DTA to EOU would be available to supplier as provided under GST rules subject to such conditions and documentations as specified there in under GST rules.“

Supply of Goods by DTA Supplier to EOU / EHTP/ STP /BTP Procedure :

Circular No. 14/14 /2017- GST, 6th November, 2017, was issued describing the detailed procedure to be followed as below :

1. The recipient EOU / EHTP / STP / BTP unit shall give prior intimation in a prescribed proforma in “Form–A” bearing a running serial number containing the goods to be procured, as pre- approved by the Development Commissioner and the details of the supplier before such deemed export supplies are made. The said intimation shall be given to –

(a) the registered supplier;

(b) the jurisdictional GST officer in charge of such registered supplier; and

(c) its jurisdictional GST officer.

2. The registered supplier thereafter will supply goods under tax invoice to the recipient EOU / EHTP / STP / BTP unit.

3. On receipt of such supplies, the EOU / EHTP / STP / BTP unit shall endorse the tax invoice and send a copy of the endorsed tax invoice to –

(a) the registered supplier;

(b) the jurisdictional GST officer in charge of such registered supplier; and

(c) its jurisdictional GST officer.

4. The endorsed tax invoice will be considered as proof of deemed export supplies by the registered person to EOU / EHTP / STP / BTP unit.

5. The recipient EOU / EHTP / STP / BTP unit shall maintain records of such deemed export supplies in digital form, based upon data elements contained in “Form-B” (appended herewith). The software for maintenance of digital records shall incorporate the feature of audit trail. While the data elements contained in the Form-B are mandatory, the recipient units will be free to add or continue with any additional data fields, as per their commercial requirements.

6. All recipient units are required to enter data accurately and immediately upon the goods being received in, utilized by or removed from the said unit. The digital records should be kept updated, accurate, complete and available at the said unit at all times for verification by the proper officer, whenever required. A digital copy of Form – B containing transactions for the month, shall be provided to the jurisdictional GST officer, each month (by the 10th of month) in a CD or Pen drive, as convenient to the said unit.

7. The above procedure and safeguards are in addition to the terms and conditions to be adhered to by an EOU / EHTP / STP / BTP unit in terms of the Foreign Trade Policy, 2015-20 and the duty exemption notification being availed by such unit.

Eligible to Claim Refund of Tax

Vide Notification No. 47/2017-Central Tax, 18th October, 2017 In the Central Goods and Services Tax Rules, 2017, – (i) in rule 89, in sub-rule (1), for third proviso, the following proviso shall be substituted, namely:-

“Provided also that in respect of supplies regarded as deemed exports, the application may be filed by, –

(a) the recipient of deemed export supplies; or

(b) the supplier of deemed export supplies in cases where the recipient does not avail of input tax credit on such supplies and furnishes an undertaking to the effect that the supplier may claim the refund”;

That means Either the Recipient or Supplier can claim Refund of Tax Paid

Procedure for Claiming Refund & Sanction of Refund:

Following are the steps to be followed :

An application in FORM GST RFD-01 shall be filed – Rule 89(1)

Application may be filed by, –

(a) the recipient of deemed export supplies; or

(b) the supplier of deemed export supplies in cases where the recipient does not avail of input tax credit on such supplies and furnishes an undertaking to the effect that the supplier may claim the refund

Rule 89(1)

The application shall be accompanied by documentary evidences in Annexure 1 in Form GST RFD-01 – a statement containing the number and date of invoices along with such other evidence as may be notified in this behalf, in a case where the refund is on account of deemed exports – Rule 89(2) & Rule 89(2)(g)

The endorsed tax invoice will be considered as proof of deemed export supplies by the registered person to EOU / EHTP / STP / BTP unit – Point (iv) of Circular No. 14/14 /2017 – GST, 6th November, 2017

Proper officer after scrutinize the application for its completeness and where the application is found to be complete issues an acknowledgement in FORM GST RFD-02 within a period of fifteen days of filing of the said application – Rule 90(2)

Where any deficiencies are noticed, the proper officer shall communicate the deficiencies to the applicant in FORM GST RFD-03 through the common portal electronically, requiring him to file a fresh refund application after rectification of such deficiencies. – Rule 90(3)

Order sanctioning refund -Where, upon examination of the application, the proper officer is satisfied that a refund is due and payable to the applicant, he shall make an order in FORM GST RFD-06 sanctioning the amount of refund to which the applicant is entitled.- Rule 92(1)

Comments :

1. Under the earlier Excise regime, through AR – 3A supplies by DTA supplier to EOU are exempted from payment of Excise Duty. However under GST Law, the DTA supplier has to charge GST as applicable for such supplies to EOU.

2. Refund of such GST paid may be claimed either by the Recipient EOU or by the Supplier.

3. There is no provision of Provisional Refund of 90% of the claimed refund amount within 7 days as in the case of Zero Rated supplies (Exports or Supplies to SEZ Dev. / SEZ units). Also there is no times refund provision and no interest payable for delays in refund if any.

4. It is advisable to claim Input Tax Credit (ITC) by the recipient EOU and utilize the same towards GST payable on DTA supplies, rather than claim refund and wait for uncertain time.

5. When DTA Sales are pre-dominantly higher than direct exports, then it is advisable to take Input Tax Credit on receipts and utilize the same towards tax liability on DTA sales.

6. It is observed that there is sharp deviation from Core Concept of Complete Digitalization of GST to Manual Procedures of submissions of Intimation, Endorsed Tax Invoice etc resembles bringing back erstwhile procedures under CT-3 & AR-3A

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner, Corporate Trainer & Author

Can be reached @ snpanigrahi1963@gmail.com

Sir , we can raise the Invoice from DTA to 100%EOU without Duty like CT-3 (as per Central Excise ) it is possible in GST , no need refund .

sir

100% eou units require yearly assessment with CTO or DCTO ? Is it mandatory? if they demand what is the reply to them?

The circular is not at all giving any relief to EOUs, Earlier under Central Excise ab initio exemption from payment of EXcise Duty granted to EOUs for the DTA procurements against issue of CT-3 forms to the suppliers

Majority of EOUs are procuring their inputs against Form H under VAT/CST provisions and they are also getting CST refund for the supplies for which they are unable to issue Form H and in case of VAT paid either they are claiming VAT refund or utilising the same for payment of VAT on DTA sales. Thus their working capital requirement become lesser if compared with present system under GST.

Under present system of GST the EOUs are procuring the materials on payment of GST and availing ITC of the same which is accumulating so far and no refund of the same has not been initiated till now and lakhs of rupees are lying their credit and this might leading for higher working capital requirement and thereby additional financial costs.

The circular 14/4/2017 states the supplies are against tax payment and the refund may be claimed either by the recipient or supplier of goods. The supplier will get refund, if the recipient has not taken input tax credit which is further leading to increase in the cost of production to the EOUs , which plays a main factor in export pricing, This is caused by not eliminating the tax portion from the cost of inputs since the recipient not eligible for neither credit nor refund.

Instead of this they can give advantage of procurement of all the materials by EOUs at concessional rate of 0.1% as per the CGST notification 40/2017,Dt.23-10-2017 so that EOUs can get major relief of paying more taxes on their procurements.

Thanks for simple clarifications regarding deemed export.

In case of within state supplies under deemed export whether IGST to charge or CGST+SGST will be payable. I tried to upload invoice on GST portal when I select invoice type as a deemed export for supply made to EOU within same state, its automatically select supply type as a inter state and not allowing to charge CGST & SGST only IGST allow to be charge. Is that mean all deemed export supplies will be considered as a inter state supplies (There is no such clarification in the GST Act or Rules)

Please share your views