Summary of conditions for availing ITC under GST

(Reference GST Acts and Final Rules)

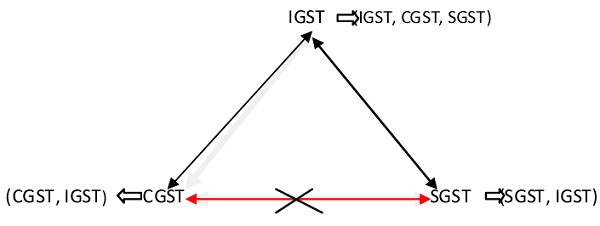

1. Manner of GST ITC utilization:

(Cross credit between CGST & SGST is not allowed)

2. Goods/ services are received

3. Invoice for the goods/ Services received

4. GST is actually paid by the supplier.

5. Return showing Supply is furnished by the Supplier

6. If goods are received in lots – Full ITC shall be allowed only when last lot is received

7. Goods/Services bill is paid along with Tax within 180 days of invoice- otherwise ITC will be reversed (unpaid bill detail need to be filed in return)

8. If part payment of bill is made –Proportionate Credit shall be allowed

9. Document for ITC-Invoice/DN/CN/BoE/Revised Inv./ISD Inv.

10. NO ITC beyond September of the following Financial Year or Annual return (earlier)

11. ISD to distribute in the same month through invoice issued under Invoice Rule 9(1)

12. ITC on opening stock is allowed in following cases:

(i) If registered within 30 days of becoming liable -(only input goods)

(ii) If voluntarily registered u/s 23(3) -(only input goods)

(iii) Shifting from composition scheme to normal scheme -(ITC Inputs & Capital Goods also)

(iv) If Exempt supply becomes taxable (ITC of Inputs & Capital Goods used exclusively for exempt)

13. ITC in case of clause 12 above can be claimed within 1 Year from the date of Invoice issued by supplier.

14. Unutilised ITC transfer allowed in case of sale/merger/demerger of business

15. ITC on input stock & Capital Goods will be paid if

(i) Taxable supply becomes exempt

(ii) Opt to shift from normal scheme to composition scheme

16. Capital Goods/P&M sale: ITC taken reduced by 5% for each qtr and balance shall be paid

17. ITC of following expenses are not allowed

(i) Motor Vehicle and other conveyance except used for further supply/transportation/training on driving, flying & navigating

(ii) Goods/Services in relation to:

| Food & Beverages* | Health Services* | Rent a Cab* |

| Outdoor Catering* | Club Membership | Life/Health Insurance* (except under law) |

| Beauty Treatment, Cosmetic & Plastic Surgery* | Health & Fitness Center

|

Leave Travel/Home Travel to Employees |

*except when inward supply is used for outward supply same category or as an element

(iii) Works Contract for construction of immoveable property unless for supply work contract. (ITC on Works Contract for Plant & Machinery allowed)

(iv) Goods/Services for construction of immoveable property on own account even for business use (self office use or renting). (However ITC on Goods/Services for Plant & Machinery allowed)

(Note: For point no. (iii) & (iv) above ‘construction’ includes reconstruction, renovation, addition or alterations or repair capitalised)

(v) Goods/Services on which tax paid under Composition scheme

(vi) Goods/Services for personal/private consumption-actually consumed

(vii) Goods lost/stolen/destroyed/written off/gifted/free samples (it seems ITC on inputs shortage due to evaporation is allowed)

(viii) ITC of Any tax paid due to demand for Fraud/Suppression/Mis-declaration/Seizure/detention

(Author is a GST Consultant and can be reached at ca.gauravagrawal@gmail.com)

Disclaimer: The views expressed herein above are solely author’s personal views/opinion. This is an informational article and should not be considered as legal opinion. The possibility of any errors and omissions in the article cannot be ruled out.

Author Bio

Is ITC allowable on goods transport vehicles belonging to manufacturing company?

Is ITC allowable on insurance, servicing, repairing of goods transport vehicles belonging to manufacturing company?