FAQs on Utilizing Cash/ ITC for Payment of Demand

Q.1 What is utilization of cash/ ITC for payment of demand or any other amount due about?

Ans: Utilization of cash/ ITC for payment of demand is about payments of non-return related liabilities. These liabilities are created through generation of Demand ID by tax officials, which is a reference number of the order or application, appearing in the Electronic Liability Register (Part-II).

Q.2 From which ledger payments against the liabilities of a particular demand ID be made?

Ans: The payments against the liabilities of a particular demand ID can be made by using the following ledgers:

- Cash balance available in the Electronic Cash Ledger; and/or

- Input tax credit balance available in the Electronic Credit Ledger.

Q.3 How does the taxpayer get to know about outstanding demands?

Ans: The taxpayer can get the information regarding outstanding demands from Electronic Liability Register (Part-II). This is shown in a table after logging in and navigating to Services > Ledgers > Electronic Liability Register > Part – II: Other than return related liabilities link

Q.4 Who can access the functionality of “Utilize cash/ ITC for payment of demand or any other amount due”?

Ans: The following persons can have access for the functionality of Utilizing cash/ITC for payment of demand or any other amount due:

- Registered taxpayer having a valid GSTIN or

- Person having temporary id or

- Taxpayers after cancellation of registration or

- Authorized/ Jurisdictional tax official

Q.5 What are the pre-conditions for utilization of cash /ITC for payment of demand or any other amount due?

Ans: The pre-conditions for utilization of cash /ITC for payment of demand or any other amount due are:

- Demand ID is already generated against which payment is yet to be made.

- User should have valid User ID and password and has necessary access for the same.

Q.6 What are the details displayed to the taxpayer after selecting a Demand ID?

Ans: The following details are displayed after user selects a Demand ID:-

- Outstanding liability towards tax, interest, penalty, fees and Others for IGST/CGST/SGST/UTGST/Cess against the selected Demand ID

- Balance as per Electronic Cash ledger

- Balance as per Electronic Credit Ledger

Q.7 What are the details to be entered by the taxpayer after selecting a Demand ID for payment?

Ans: The following details are to be entered by the taxpayer after selecting a Demand ID for payment:

- Amount intended to be paid

- Amount intended to be paid through Cash

- Amount intended to be paid through ITC

Q.8 How is the relief towards reduced penalty available to the taxpayer, if payment is made within the specified period as per law?

Ans: In case Demand ID is created under section 74 of the CGST/SGST/IGST/Cess Act, then as per law, GST Portal shows reduced payment liability towards penalty, if taxpayer makes payment, as per following conditions:

- If Payment is being made within 30 days from the date of communication of the order and

- taxpayer is making full payment of tax and interest, stated in the order;

The penalty amount displayed is 50% of the amount stated in the order and the balance 50% of the penalty is waived off. A credit entry is passed in the Electronic Liability Register – Part II accordingly.

Q.9 Can a user make part payment or multiple payments against a particular Demand ID?

Ans: Yes, GST Portal allows user for making part payment at multiple occasions, against a particular demand ID, till the outstanding balance becomes zero.

Q.10 Are there any conditions for a taxpayer to be eligible for waiver of penalty against a Demand ID?

Ans: Only if the payment is made against a Demand ID, created under Section 74 of the Act, within the specified period of 30 days from the date of communication of the order, the taxpayer is eligible for waiver of 50% of the penalty levied in the order.

Following conditions must also be fulfilled:

- The amount of penalty waiver will be considered if the demands included in the order, is paid off completely, across the Acts.

- If the taxpayer doesn’t pay off the reduced penalty along with tax and interest in full, within 30 days, no entries of reduced penalty will be posted in the Liability Register – Part II.

- Non-payment of any amount included in the demand towards “others” or Fees” won’t be considered towards eligibility of waiver of 50% of the penalty amount.

- This convention will hold for each demand created under the aforesaid section.

- Such entry of waiver of penalty will be tagged against the same demand only for which the payment is being made.

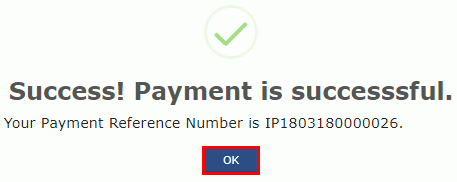

Q.11 How would the taxpayer know that the utilization of cash/ITC has been successful?

Ans: On click of “Set-Off” button, if payment is successful, a success message is displayed along with PRN (Payment Reference Number) and all the relevant ledgers get updated.

Q.12 What is Payment Reference Number?

Ans: Payment Reference Number is a unique reference number for any payment transaction done on the GST Portal which gets posted to Electronic Liability Register Part-II.

Q.13 Which ledgers of the taxpayer gets updated on utilization of cash/ITC?

Ans:

i. On utilization of ITC, Debit entry number is generated and posting is done against that demand ID in Electronic Liability Register Part-II as well as in the Electronic Credit Ledger.

ii. On utilization of Cash, Debit entry number is generated and posting is done against that demand ID in Electronic Liability Register Part-II as well as in the Electronic Cash Ledger.

iii. In case of full payment is made under Demand order raised under Section 74 of CGST/SGST Act read with section 20 of IGST Act or Section 21 of UTGST Act, an entry would be posted in the Electronic Liability Register – Part II for the 50% penalty waiver.

Manual on Utilizing Cash/ ITC for Payment of Demand

How can I make payment towards outstanding demand appearing in Electronic Liability Register (Part-II) at the GST portal?

To make payment towards outstanding demand appearing in Electronic Liability Register (Part-II) at the GST portal, perform following steps:

1. Access the https://www.gst.gov.in/ URL. The GST Home page is displayed.

2. Login to the GST Portal with valid credentials.

3. Click the Services > Ledgers > Payment towards Demand command.

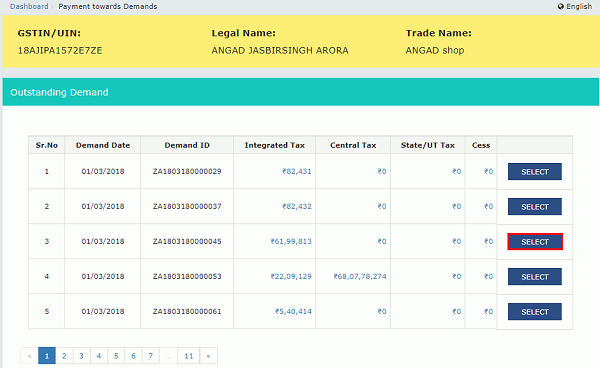

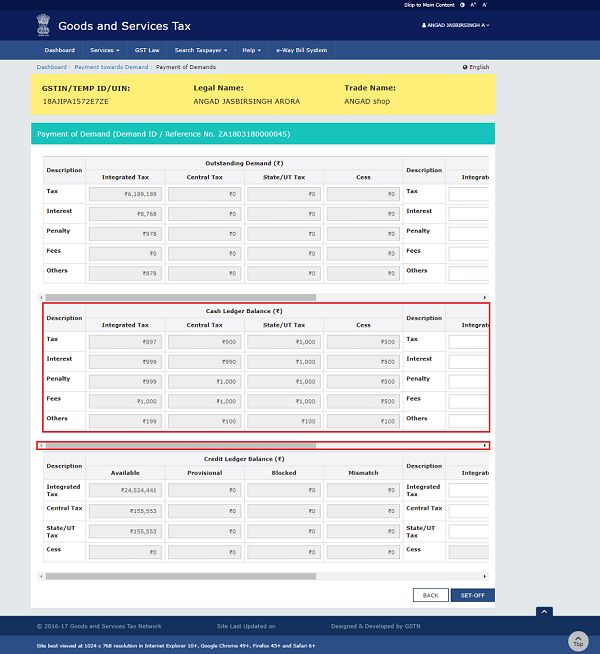

4. The Outstanding Demand page is displayed. You can see the all the Demand IDs against which demand is outstanding. Click the link under Integrated Tax, Central Tax, State Tax and Cess to view further details.

Note: The Minor Heads include: Tax, Interest, Penalty, Fee and Others. The Minor Head wise balance is displayed for the selected Major Head.

5. Click the Close button.

6. Click the SELECT button to select the Demand ID.

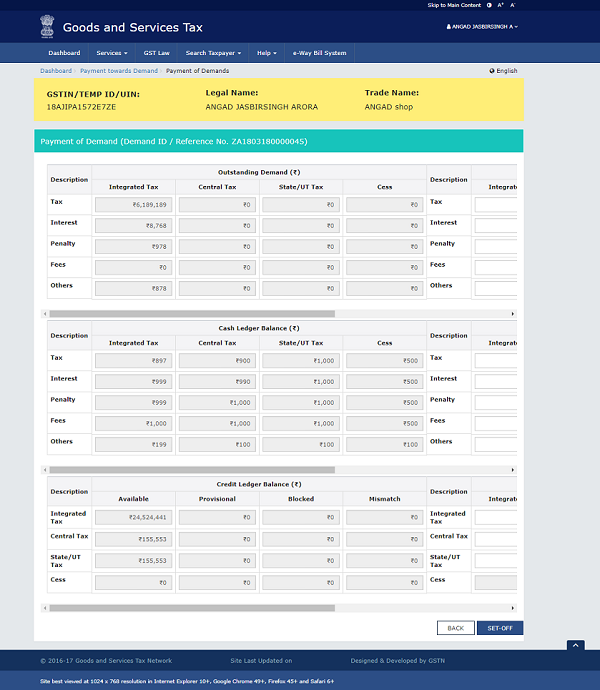

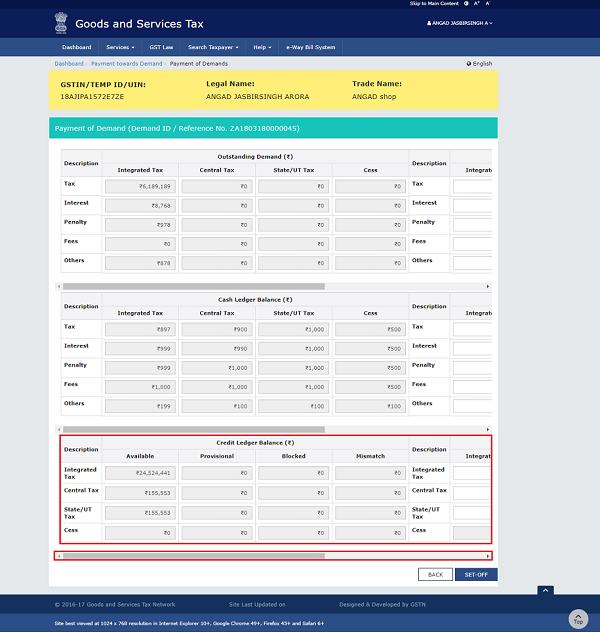

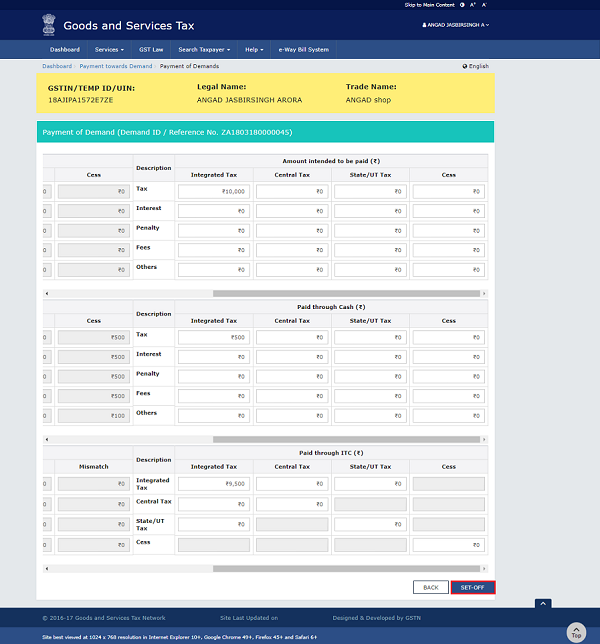

7. Outstanding Demand, Cash Ledger Balance and Credit Ledger Balance details are displayed.

The outstanding demand against the Demand ID as on date are shown in below table.

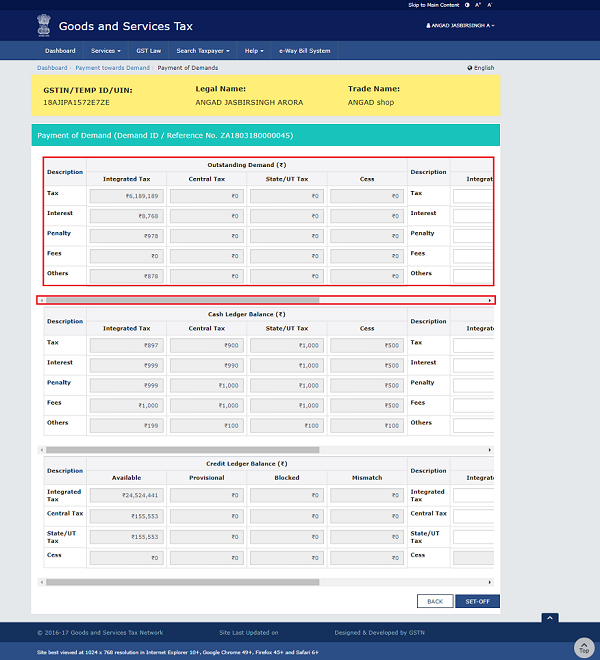

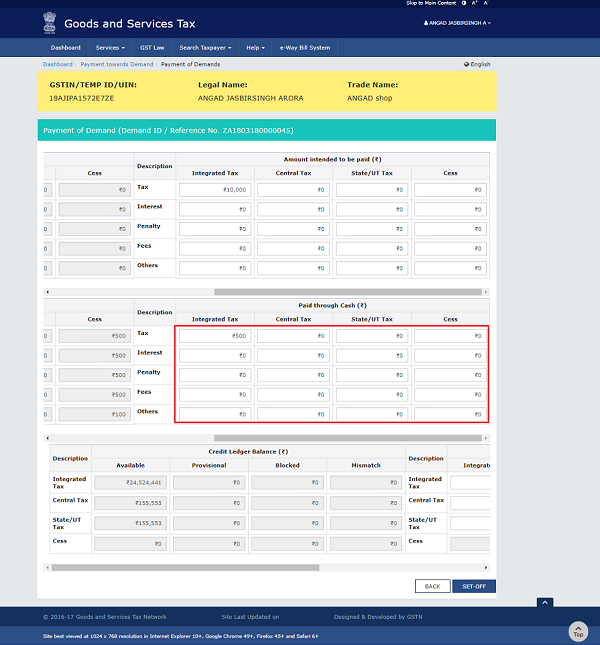

Use the scroll bar to move to the right to enter the amount intended to be paid against that Demand ID.

Cash Ledger Balance

The cash available as on date are shown in below table.

Use the scroll bar to move to the right to enter the amount to be paid through cash against that Demand ID.

Credit Ledger Balance

The ITC available as on date are shown in below table.

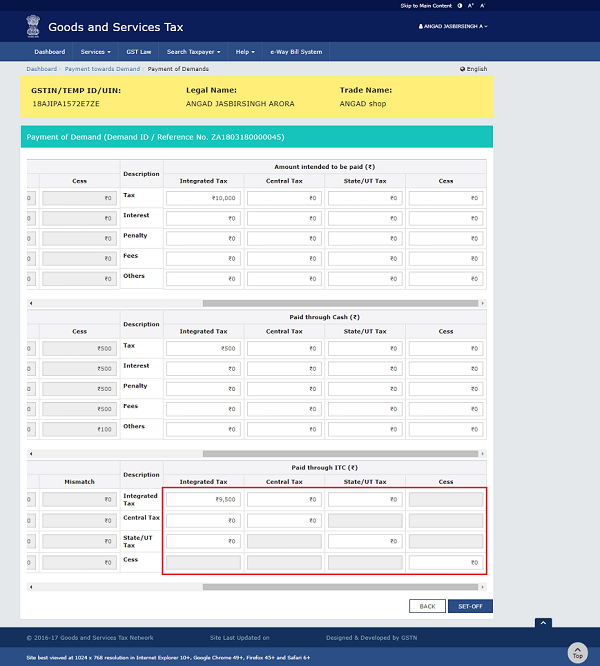

Use the scroll bar to move to the right to enter the amount to be paid through ITC against that Demand ID.

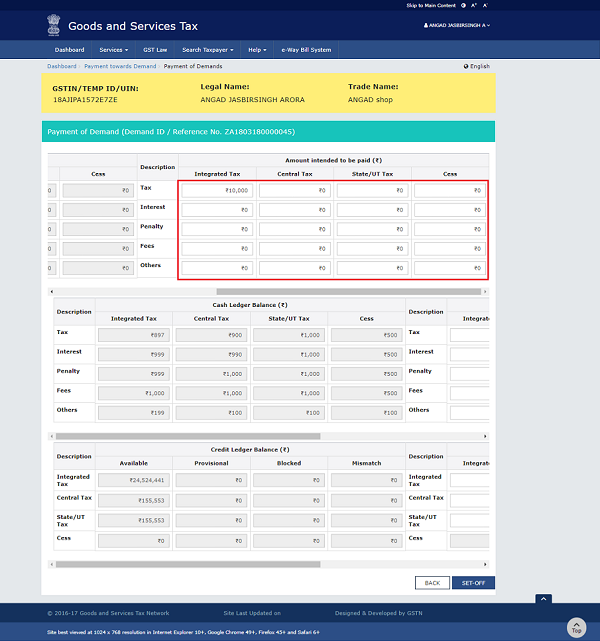

8. Once you have entered the amount, click the SET-OFF button.

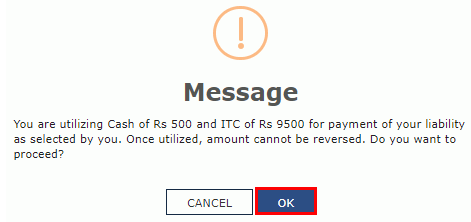

9. A confirmation message is displayed. Click the OK button.

10. A success message is displayed. Payment Reference Number is displayed on the screen. Click the OK button.

Note:

1. On utilization of ITC, Debit entry number will be generated and posting will be done against that demand ID in Electronic Liability Register Part-II as well as in the Electronic Credit Ledger.

2. On utilization of Cash, Debit entry number will be generated and posting will be done against that demand ID in Electronic Liability Register Part-II as well as in the Electronic Cash Ledger.

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Very sorry for this customer. 55 outstanding demands..GST department is making lives of all businesses very hectic. How many demand orders on a single day? Anyway thanks to author of this post