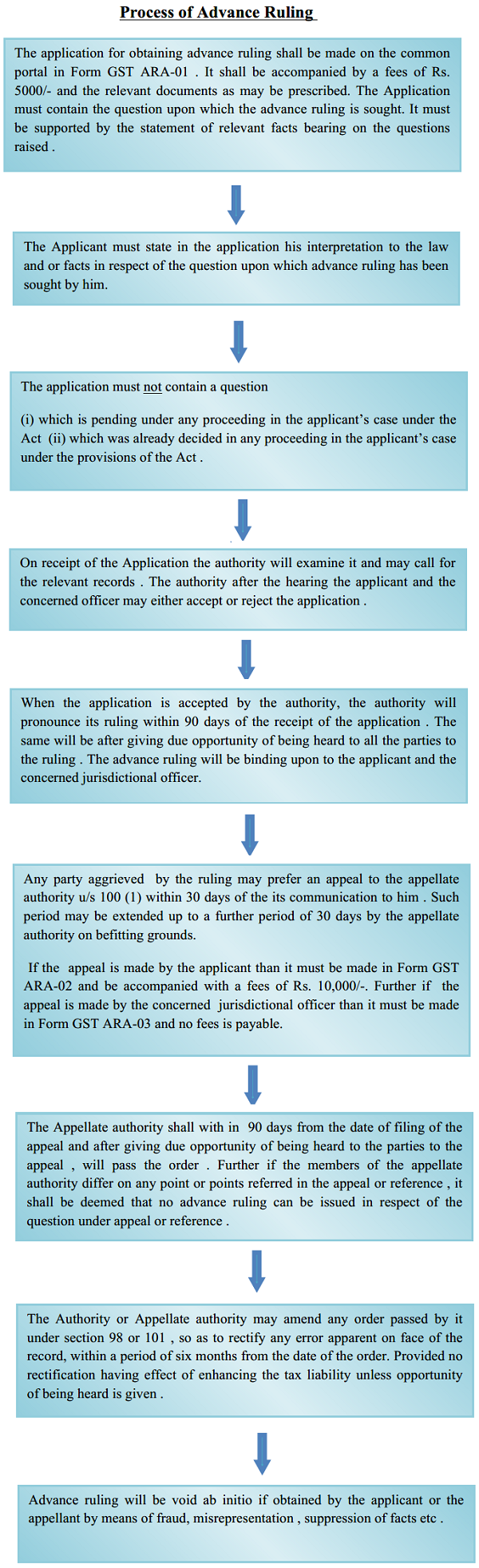

Meaning and Necessity of Advance Ruling under GST:

An advance ruling may be defined as an determination of certain matters and question as specified by the law , regarding interpretation of the law specifically in those cases where there is an ambiguity in the law itself and assessee wishes to avoid any type of litigation on the basis of such ambiguity. This also reduce valuable time and cost of the applicant and enhances the overall compliance of the law. By this applicant is in better position to take the right decision at right time .

The government had appointed authority for advance ruling and appellate authority for each state . However due to the some stances of the conflicting decisions on the some or more related issues by the advance ruling authorities of various states , the GST council in its 31st meeting held on 22 December 2018 had mooted the proposal of creation of Centralised Appellate Authority for Advance Ruling for the solutions of GST litigations from across the country. This will pave the way of uniformity on a particular matter and greater compliance of the law.

Provisions under the CGST Act, 2017 and CGST Rules,2017

The Chapter XVII of the CGST Act, 2017 contains the provisions regarding the Advance Ruling . It consists of the 12 sections starting from the sec 95 to 106. The procedures regarding the advance ruling is given in the chapter XII of CGST Rules, 2017 which consists of 6 rules ( Rule 103 to 107A).

Situations where Advance Ruling under the GST can be obtained under the Provisions of the CGST Act,2017:

Sec. 97(2) of the CGST Act , 2017 has prescribed the situations where advance ruling can be obtained

(i) Classification of any goods or services or both;

(ii) Applicability of a notification issued under the provisions of this Act;

(iii) Determination of time and value of supply of goods or services or both;

(iv) Admissibility of input tax credit of tax paid or deemed to have been paid;

(v) Determination of the liability to pay tax on any goods or services or both;

(vi) Whether applicant is required to be registered;

(vii) Whether any particular thing done by the applicant with respect to any goods or services or both amounts to or results in a supply of goods or services or both, within the meaning of that term.

Few more important points relating to the advance ruling

(i) We have to kept in mind that while applying for advance ruling that the our statement of the fact and the interpretation of the law must be clearly spelt out and must be supported by the actual facts and must not be based on the imaginary situations .

(ii) One more important point to remember that the advance ruling will always have prospective effects only.

(iii) If the law and/or the facts of the original advance ruling changes than the advance ruling will not be applicable .

(About the author – The author is a member of ICAI and can be reached at Email: nikhilkumarca@gmail.com , Mobile: 09936424523, Office: Flat No. 102, First Floor , Vasundhra Complex, Ring Road, Sector-16, Indira Nagar, Lucknow-226016 , U.P., India )

Author Bio