Page Contents

- 1. What is Reverse Charge?

- 2. Why Reverse Charge Mechanism under GST?

- 3. When is Reverse Charge Mechanism Applicable?

- 4. Reverse Charge on Goods

- 5. Reverse Charge on Services

- 6. Conditions/ Requirements under the Reverse Charge Mechanism

- 7. GST Registration under Reverse Charge Mechanism

- 8. Time of Supply in case of Reverse Charge under GST

- 9. Manner of payment of GST under Reverse Charge

- 10. Input Tax Credit on Reverse Charge

- 11. Self-Invoicing Under reverse charge mechanism

- 12. Exemptions under Reverse Charge

- 13. Composition Scheme

- 14. Other Relevant Points

- 15. Difference between Forward Charge and Reverse Charge

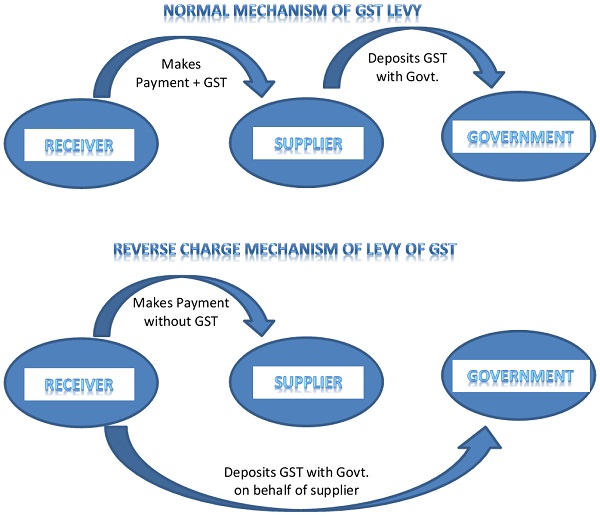

1. What is Reverse Charge?

- Normally, the supplier of goods or services pays the tax on supply.

- In the case of Reverse Charge, the receiver becomes liable to pay the tax, i.e., the chargeability gets reversed.

2. Why Reverse Charge Mechanism under GST?

Motive of Reverse Charge Mechanism is mainly more tax compliance and increased tax revenues. Government was unable to collect service tax from various unorganised sectors but through Reverse charge mechanism compliance has gone up thus on certain services because of this reason RCM has been brought under GST regime as well.

3. When is Reverse Charge Mechanism Applicable?

A. Supply from an Unregistered dealer to a Registered dealer

- If a vendor who is not registered under GST, supplies goods to a person who is registered under GST, then Reverse Charge would apply.

- This means that the GST will have to be paid directly by the receiver to the Government instead of the supplier.

- The registered dealer who has to pay GST under reverse charge has to do self-invoicing for the purchases made.

- For Inter-state purchases the buyer has to pay IGST. For Intra-state purchased CGST and SGST has to be paid under RCM by the purchaser.

B. Services through an E-Commerce operator

- If an e-commerce operator supplies services then reverse charge will be applicable to the e-commerce operator. He will be liable to pay GST.

Example:

UrbanClap provides services of electricians, teachers, beauticians etc. UrbanClap is liable to pay GST and collect it from the customers instead of the registered service providers.

- If the e-commerce operator does not have a physical presence in the taxable territory, then a person representing such electronic commerce operator for any purpose will be liable to pay tax. If there is no representative, the operator will appoint a representative who will be held liable to pay GST.

C. Supply of certain goods and services specified by CBEC

CBEC has issued a list of goods and a list of services on which reverse charge is applicable.

The following is the list of goods and services specified by CBEC

4. Reverse Charge on Goods

| S.No | Description of supply of goods | Supplier of goods | Recipient of goods |

| 1. | Cashew nuts, not shelled or peeled | Agriculturist | Any registered person |

| 2. | Bidi wrapper leaves (tendu) | Agriculturist | Any registered person |

| 3. | Tobacco leaves | Agriculturist | Any registered person |

| 4. | Supply of lottery | State Government, Union Territory or any local authority | Lottery distributor or

selling agent |

| 5. | Silk yarn | Any person who manufactures silk yarn from raw silk or silk worm cocoons for supply of silk yarn | Any registered person |

5. Reverse Charge on Services

| S.No | Name of Service | Service Provider | Service Receiver |

| 1. | Import of Service | Foreign party | Indian party |

| 2. | Transport of Goods by Road | Goods Transport Agency | > Any person registered under CGST, SGST, UTGST

> Any Factory > Any Society/ Cooperative society registered in India > Any body corporate (Company) > Any Partnership Firm > Casual Taxable person |

| 3. | Advocate/ Legal service | Advocate/ Firm of Advocates | Any business entity |

| 4. | Arbitrary Tribunal | Advocate/ Firm of Advocates | Any business entity |

| 5. | Sponsorship service | Any person | Any body corporate (Company) or Partnership |

| 6. | Service by Director | Director | Any body corporate (Company) |

| 7. | Insurance Agent Service | Insurance Agent | Insurance company |

| 8. | Recovery Agent Service | Recovery Agent | Bank or Financial Institutions |

| 9. | Ocean Freight (Transport of Goods by Vessel from place outside India to customs clearance in India) | Foreign Party | Importer |

| 10. | Copyright service related to literacy, drama, musical, artistic work | Author, music composer, photographer, artist | Publisher, Music company, Producer |

| 11. | Radio Taxi Service | Taxi Driver | E-Commerce Company |

| 12. | All Services by Government except:

> Renting of Immovable property > Service of Department of Posts > Services in relation to Aircraft or Vessel > Services of Transport of Goods or Passengers |

Government | Business Entity |

6. Conditions/ Requirements under the Reverse Charge Mechanism

- There should be a supply of goods or services

- The supply should be in respect of taxable goods/ services

- Supply must be by an unregistered person

- Supply must be to a registered person

- Supply must be an intra-state supply as compulsory registration is required for inter-state sales

- Every registered business owner should maintain accurate records of supplies that would incur reverse charge

- Wherever reverse charge applies, the supplier must clearly mention on the invoice that the tax payable for that specific transaction is through reverse charge. Similarly, the same should be mentioned on receipt vouchers and refunds vouchers

- Advance paid on supplies that incur reverse charge is taxable under GST. The taxpayer making advance payment should pay tax on reverse charge basis

7. GST Registration under Reverse Charge Mechanism

- Under Normal Charge Mechanism a service provider is required to get himself registered after the limit of Rs. 20 Lakh (10 lakhs in case of special category states) aggregate turnover is crossed.

- However under Reverse Charge Mechanism a person liable to pay GST is required to get himself registered even if the turnover is below the threshold limit as there is a concept of compulsory registration under GST Act.

8. Time of Supply in case of Reverse Charge under GST

The time of supply for a transaction is the date on which taxes are levied upon the supplies.

| Time of Supply of Goods | Time of Supply of Services |

| Earliest of the following dates:

> Date of Receipt of Goods > Date of Payment > The date immediately following 30 days from the date of issue of invoice |

Earliest of the following dates:

> Date of Payment > The date immediately following 60 days from the date of issue of invoice

|

Note: Date of payment shall be earliest of

- The date on which payment has been debited from supplier’s bank account

- When the recipient records payment in his books of accounts.

9. Manner of payment of GST under Reverse Charge

- ITC can be used for payment of output tax only.

- Therefore tax under reverse charge can be paid through cash only without availing the benefit of ITC.

- The supplier must mention in his tax invoice whether the tax is payable on reverse charge.

10. Input Tax Credit on Reverse Charge

- Input tax credit can be claimed by the buyer as long as they use the goods and services they bought on reverse charge basis for business purposes only.

- Also, a supplier cannot claim ITC on the tax paid on goods/services that were used to make supplies that incur reverse charge.

11. Self-Invoicing Under reverse charge mechanism

Under reverse charge mechanism, self-invoicing is done when a business owner purchases supply from an unregistered supplier. This is done, as the unregistered supplier cannot issue an invoice.

12. Exemptions under Reverse Charge

A registered business owner is exempted from paying GST through reverse charge on intra-state purchases from unregistered sellers, as long as the total value of the supply received per day is less than or equal to Rs.5,000/-.

13. Composition Scheme

In general, small taxpayers with the aggregate turnover of INR 1.5 crores in a financial year are eligible to pay tax under composition scheme. But, taxpayers paying tax on the basis of the reverse charge under GST are not eligible for composition scheme.

14. Other Relevant Points

- An ISD cannot make purchases liable to Reverse Charge. If the ISD wants to procure such supplies and take the Reverse Charge paid as credit, the ISD should register as a Normal Taxpayer.

- Under the reverse charge mechanism, the GST applicable must be submitted to the government on every 20th of next month.

- There will be no auto-population of details of the GST paid under the RCM in GSTR 2, but it will be subjected to the manual furnishing of details.

- Payment voucher must be issued by the recipient at that at the time period of suppliers payment.

- The ITC is not available for the reverse charge payment to the authority.

- The reverse charge mechanism is applicable to payments made in advance also.

15. Difference between Forward Charge and Reverse Charge

| S.No | Particulars | Forward Charge | Reverse Charge |

| 1. | Meaning | Forward charge is a mechanism where the supplier of goods/ services is liable to pay tax. | Reverse charge is a mode of collecting GST on supplies of goods and services where the receiver of the goods/ service will be liable to pay GST to the government. |

| 2. | Tax Liability | The tax liability is on the supplier of the goods or services or both. | The tax liability is on the receiver of the goods or services or both. |

| 3. | Registration | Registration is required once a supplier meets the threshold limit. | All the people required to pay tax under reverse charge have to register themselves for GST irrespective of threshold. |

| 4. | Supplier | A supplier can only be a registered supplier. An unregistered supplier cannot collect tax. | A supplier can also be a registered supplier in case of supply of notified goods or services. |

| 5. | Recipient | A recipient can be a registered or an unregistered person. | A recipient should be registered in RCM in case of section 9(3) of CGST Act and section 5(3) of IGST Act. |

as RCM exempted for purchase from unregistered supplier till sep19, plz clarify for self invoice for import purchase and gta

Hi Team,

you have mentioned that

“12. Exemptions under Reverse Charge

A registered business owner is exempted from paying GST through reverse charge on intra-state purchases from unregistered sellers, as long as the total value of the supply received per day is less than or equal to Rs.5,000/-.”

However as per the understanding, this provision has been kept on hold and any payment even above INR 5000 per day to unregistered party do not attract Reverse Charge Mechanism.

Pls clarify