Time is now ripe for conducting GST Audit along with Reconciliation with books of accounts and filing of GST Annual Return. While reconciling the Accounts, it is very important to look into Transactions that attracts Reverse Charge, where the Recipient is Liable for Discharge Taxes and not the Supplier.

In this Posting Let’s Discuss Some Critical Aspects that need attention in case of Reverse Charge Mechanism.

Page Contents

1. What is Reverse Charge Mechanism (RCM)

Normally, the supplier of goods or services pays the tax on supply. In the case of Reverse Charge, the receiver becomes liable to pay the tax, i.e., the chargeability gets reversed.

RCM : Definition :

Sec 2(98) of CGST Act : “reverse charge” means the liability to pay tax by the recipient of supply of goods or services or both instead of the supplier of such goods or services or both under sub-section (3) or sub-section (4) of section 9, or under sub-section (3) or subsection (4) of section 5 of the Integrated Goods and Services Tax Act;

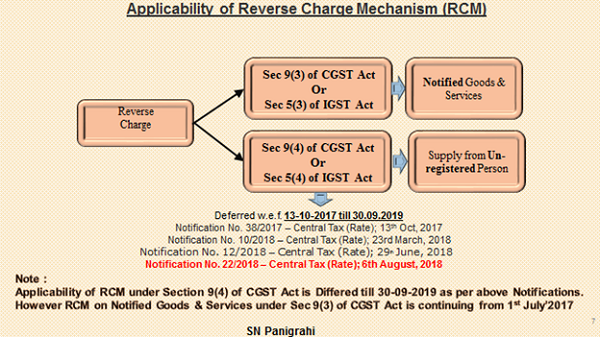

2. Applicability of Reverse Charge Mechanism (RCM)

2. Applicability of Reverse Charge Mechanism (RCM)

Sec 9(3) of CGST Act : The Government may, on the recommendations of the Council, by notification, specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis by the recipient of such goods or services or both and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

Sec 9(4) of CGST Act : The central tax in respect of the supply of taxable goods or services or both by a supplier, who is not registered, to a registered person shall be paid by such person on reverse charge basis as the recipient and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

Note :

Applicability of RCM under Sec 9.4 of CGST Act

> In case of supplies by any Unregistered Person to a registered person the Liability of Payment of RCM Deferred w.e.f. 13-10-2017 till 30.09.2019.

> However, under this Section RCM is Applicable from 1-07-2017 to 12-10-2017

Applicability of RCM under Sec 9.3 of CGST Act

> However, RCM on Notified Goods & Services under Sec 9(3) of CGST Act is continuing from 1st July’2017

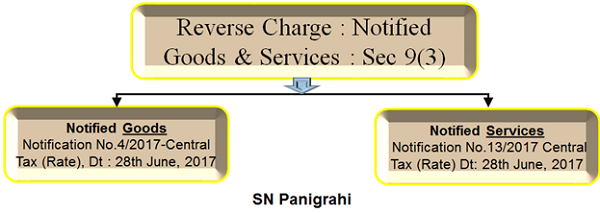

Let us now focus on Reverse charge applicable in case of supply of notified goods or services or both.

3. RCM Related Some Critical Issues:

Let us here discuss Some Critical Issues which the business may not aware or ignorant regarding applicability of RCM.

- Services supplied by the Central Government, State Government, Union territory or local authority to a business entity

- RCM on Ocean Freight

Applicability of RCM on above are depicted below which are self-explanatory.

Some other Critical Aspects to Consider

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Disclaimer : The views and opinions; thoughts and assumptions; analysis and conclusions expressed in this article are those of the authors and do not necessarily reflect any legal standing.

Author : SN Panigrahi, GST Consultant, Practitioner, Corporate Trainer & Author

Member Board of Studies, IIMM; Co-Chairman, Indirect Tax Committee, FTACII

Can be reached @ snpanigrahi1963@gmail.com

Author Bio

RCM on fee paid for Approval from Pollution board is not covered u/s 9(3) as pollution board is not a covered under central government, asper the faq issued by CBEC. Hence it will be covered U/s 9(4)