◊ BACKGROUND OF REVERSE CHARGE MECHANISM

♦ Reverse Charge Mechanism was first introduced in Service Tax Law.

♦ Now, the Government has incorporated RCM in GST.

♦ Government has notified not only supply of certain services but also supply of certain goods under RCM.

◊ OBJECTIVE OF REVERSE CHARGE MECHANISM

♦ Safeguard the interest of Revenue

♦ Administrative convenience of Government

Page Contents

Statutory Provision

◊ Section 2(98) of the CGST Act,2017

> “reverse charge” means the liability to pay tax by the recipient of supply of goods or services or both instead of the supplier of such goods or services or both under sub-section (3) or sub-section (4) of Section 9, or under sub-section (3) or sub-section (4) of Section 5 of the Integrated Goods and Services Tax Act.

◊ Section 9(3) of the CGST Act,2017

- The Government may, on the recommendations of the Council, by notification, specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis by the recipient of such goods or services or both and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

◊ Section 5(3) of the IGST Act,2017

- The Government may, on the recommendations of the Council, by notification,specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis by the recipient of such goods or services or both and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

Comprehend two types of reverse charge scenarios in GST

|

|

Specified categories of supply of Goods under Reverse Charge i.e. 9(3) of CGST Act, 2017/5(3) of IGST Act, 2017

| Tariff item, sub-heading, heading or Chapter | Description of supply of Goods | Supplier of goods | Recipient of supply |

| 0801 | Cashew nuts, not shelled or peeled | Agriculturist | Any registered person |

| 1404 90 10 | Bidi wrapper leaves (tendu) | Agriculturist | Any registered person |

| 2401 | Tobacco leaves | Agriculturist | Any registered person |

| 5004 to 5006 | Silk yarn | Any person who manufactures silk yarn from raw silk or silk worm cocoons for supply of silk yarn | Any registered person |

–

| Tariff item, sub-heading, heading or Chapter | Description of supply of Goods | Supplier of goods | Recipient of supply |

| 5201 | Raw cotton (Effective from 15-11-2017) | Agriculturist | Any registered person |

| – | Supply of lottery | State Government, Union Territory or any local authority | Lottery distributor or selling agent. |

| Any Chapter (Effective from 13-10-2017) | Used vehicles seized and confiscated goods, old and used goods, waste and scrap | Central Government, State Government, Union territory or a Local authority. | Any registered person |

| Any Chapter (Effective from 28-5-2018) | Priority Sector Lending Certificate | Any registered person | Any registered person |

Reverse Charge on specified services i.e. 9(3) of CGST Act, 2017/5(3) of IGST Act, 2017

1. Category Of Supply Of Services: GTA Services

Supply of Services by a Goods Transport Agency (GTA) who has not paid central tax @ 6% in respect of transportation of goods by road to –

(a) any factory registered under or governed by the Factories Act, 1948;or

(b) any society registered under the Societies Registration Act, 1860 or under any other law for the time being in force in any part of India;or

(c) any co-operative society established by or under any law;or

(d) any person registered under CGST/IGST/SGST/or UTGST Act;or

(e) anybody corporate established, by or under any law;or

(f) any partnership firm whether registered or not under any law including association of persons;or

(g) any casual taxable person located in the taxable territory.

Provided that nothing contained in this entry shall apply to services provided by a goods transport agency, by way of transport of goods in a goods carriage by road, to, –

(a) a Department or Establishment of the Central Government or State Government or Union territory;or

(b) local authority;or

(c) Governmental agencies, which has taken registration under the Central Goods and Services Tax Act, 2017 (12 of 2017) only for the purpose of deducting tax under Section 51 and not for making a taxable supply of goods or services.

Supplier of service Goods Transport Agency (GTA)

Recipient of service :

(a) any factory registered under or governed by the Factories Act, 1948;or

(b) any society registered under the Societies Registration Act, 1860 or under any other law for the time being in force in any part of India;or

(c) any cooperative society established by or under anylaw;

(d) any person registered under CGST/IGST/SGST/UTGST Act;or

(e) anybody corporate established, by or under any law;or

(f) any partnership firm whether registered or not under any law including association of persons;or

(g) any casual taxable person located in the taxable territory.

Who is GTA – Goods Transport Agency ?

- Goods transport agency means any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called.

- To qualify as services of GTA, the GTA should be necessarily issuing a consignment note.

- Only services provided by a GTA are taxable under GST.

Q: Are intermediary and ancillary services(loading/unloading, packing/unpacking, transshipment etc.) provided in relation to transportation of goods by road to be treated as part of GTA service, being a composite supply, or these services are to be treated as separate supplies ?

A: GTA provides service to a person in relation to transportation of goods by road in a goods carriage, which is a composite service. The composite service may include various intermediary and ancillary services, such as, loading/unloading, packing/unpacking, transshipment and temporary warehousing, which are provided in the course of transport of goods by road. These services are not provided as independent services but as ancillary to the principal service, namely, transportation of goods by road. The invoice issued by the GTA for providing the service includes the value of intermediary and ancillary services.

In view of this, such ancillary services would form part of part of GTA service and would not be treated as a separate supply. Any service provided along with the GTA service that is part of the composite service of GTA shall be taxed along with GTA service and not as separate supplies.

However, if such incidental services are provided as separate services and charged separately, whether in the same invoice or separate invoices, they shall be treated as separate supplies.

2. Category Of Supply Of Services: Legal Services

Services provide by an individual advocate including a senior advocate or firm of advocates by way of legal services, directly or indirectly.

Explanation – ‘Legal service’ means any service provided in relation to advice, consultancy or assistance in any branch of law,in any manner and includes representational services before any Court, Tribunal or Authority.

Supplier of service : An individual advocate including a senior advocate or firm of advocates

Recipient of service : Any business entity located in the taxable territory

Relevant Exemptions – Notification No. 9/2017-Integrated Tax(Rate) or Notification No. 12/2017- Central Tax (Rate)

Services provided by :

(a)……………………….

(b) a partnership firm of advocates or an individual as an advocate other than a senior advocate, by way of legal services to

(i) an advocate or partnership firm of advocates providing legal services;

(ii) any person other than a business entity;or

(iii) a business entity with an aggregate turnover up to such amount in the preceding financial year as makes it eligible for exemption from registration under the Central Goods and Services Tax Act, 2017;or

(iv) The Central Government, State Government, Union Territory, local authority, Government Authority or Government Entity.

Relevant Exemptions – Notification No. 9/2017-Integrated Tax(Rate) or Notification No. 12/2017- Central Tax (Rate)

Services provided by :

(c) a senior advocate by way of legal services to

(i) Any person other than a business entity; or

(ii) a business entity with an aggregate turnover up to such amount in the preceding financial year as makes it eligible for exemption from registration under the Central Goods and Services Tax Act, 2017; or

(iii) The Central Government, State Government, Union Territory, local authority, Government Authority or Government Entity.

3. Category Of Supply Of Services: Arbitral Services

Services supplied by an arbitral Tribunal to a business entity.

Supplier of service : An arbitral Tribunal

Recipient of service : Any business entity located in the taxable territory

Relevant Exemptions – Notification No. 9/2017-Integrated Tax(Rate) or Notification No. 12/2017- Central Tax (Rate)

Services provided by :

(a) An arbitral tribunal to–

(i) Any person other than a business entity; or

(ii) a business entity with an aggregate turnover up to such amount in the preceding financial year as makes it eligible for exemption from registration under the Central Goods and Services Tax Act, 2017; or

(iii) The Central Government, State Government, Union Territory, local authority, Government Authority or Government Entity.

4. Category Of Supply Of Services: Sponsorship Services

Service provided by way of Sponsorship Service to anybody corporate or partnership firm.

Supplier of service : Any person

Recipient of service : Anybody corporate or partnership firm located in the taxable territory.

Relevant Exemptions – Notification No. 9/2017-Integrated Tax (Rate) or Notification No. 12/2017- Central Tax (Rate)

Services provided by way of sponsorship of sporting events organized:

(a) By a national sports federation, or its affiliated federations, where the participating teams or individuals represent any district, State, zone or country;

(b) By Association of Indian Universities, Inter-University Sports Board, School Games Federation of India, All India Sports Council for the Deaf, Paralympics Committee of India or Special Olympics Bharat;

(c) By Central Civil Services Cultural and Sports Board;

(d) As part of national games, by Indian Olympic Association;or

(e) Under Panchayat Yuva Kreeda Aur Khel Abhiyaan (PYKKA) Scheme 21

5. Category Of Supply Of Services: Government Services

Services supplied by the Central Government, State Government, Union territory or local authority to a business entity excluding the following:

(A) renting of immovable property service,and

(B) services specified below:-

(i) services by the Department of posts by way of speed post, life insurance, express parcel post and agency services provided to a person other than Central Government, State Government or Union territory orlocal authority;

(ii) services in relation to an aircraft or a vessel, inside or outside the precincts of a port or anairport;

5. Category Of Supply Of Services: Government Services

(iii) transport of goods or passengers

Supplier of Service:

Central Government, State Government, Union territory or Local Authority.

Recipient of service:

Any person registered under the Central Goods and Services Tax Act,2017

5A. Category Of Supply Of Services: Services by the Government

Services supplied by the Central Government, State Government, Union territory or local authority by way of renting of immovable property.

(with effect from 25-1-2018)

Supplier of Service:

Central Government, State Government, Union territory or Local Authority

Recipient of service:

Any person registered under the Central Goods and Services Tax Act, 2017

For the period 01.07.2017 to 24.01.2018, these services were subject to Forward Charge

5B. Category Of Supply Of Services

Services supplied by any person by way of transfer of development rights or Floor Space Index (FSI) (including additional FSI) for construction of a project by a promoter. (w.e.f.01.04.2019)

Supplier of Service:

Any Person

Recipient of service:

Promoter

Floor Space Index (FSI) shall mean the ratio of a building’s total area (gross floor area) to the size of the piece of a land upon which it is built.

Project shall mean a Real Estate Project (REP) or a Residential Real Estate Project (RREP).

Real Estate Project (REP) shall have the same meaning as assigned to it in in clause (zn) of section 2 of the Real Estate (Regulation and Development) Act, 2016 (16 of 2016).

Residential Real Estate Project (RREP) shall mean a REP in which the carpet area of the commercial apartments is not more than 15 per cent. of the total carpet area of all the apartments in the REP

Promoter shall have the same meaning as assigned to it in clause (zk) under section 2 of the Real Estate (Regulation and Development) Act, 2016 (16 of 2017).

Source of Explanation : N. No. 05/2019 Central Tax (R) dated 29.03.2019

5C. Category Of Supply Of Services

Long term lease of land (30 years or more) by any person against consideration in the form of upfront amount (called as premium, salami, cost, price, development charges or by any other name) and/or periodic rent for construction of a project by a promoter. W.e.f. 01.04.2019

Supplier of Service:

Any Person

Recipient of service:

Promoter

6. Category Of Supply Of Services: Services by the Director

Services supplied by a director of a company or a body corporate to the said company or the body corporate.

Supplier of Service

A director of a company or a body corporate

Recipient of Service

A company or a body corporate located in the taxable territory

Clarification in respect of levy of GST on Director’s remuneration

(Circular No: 140/10/2020 – GST – dated 10.06.2020)

Director’s remuneration which are declared as Salaries in the books of a company and subjected to TDS under Section 192 of the IT Act, are not taxable in terms of Schedule III of the CGST Act, 2017.

Employee Director’s remuneration which is declared separately other than “salaries” in the Company’s accounts and subjected to TDS under Section 194J of the IT Act as Fees for professional or Technical Services shall be treated as consideration for providing services which are outside the scope of Schedule III of the CGST Act, and is therefore, taxable.

7. Category Of Supply Of Services: Insurance Agent Service

Services provided by an insurance agent to person carrying on insurance business.

Supplier of Service An Insurance Agent

Recipient of Service

Any person carrying on insurance business, located in the taxable territory.

8. Category Of Supply Of Services: Recovery Agent Service

Services provided by a recovery agent to a banking company or a financial institution or a non-banking financial company.

Supplier of Service A Recovery Agent

Recipient of Service

Banking company or financial institution or a non-banking financial company, located in the taxable territory.

9. Category Of Supply Of Services: Copyright Service

Supply of Services by a music composer, photographer, artist or the like by way of transfer or permitting the use or enjoyment of a copyright covered under clause

(a) of sub-section (1) of Section 13 of the Copyright Act, 1957 relating to original dramatic, musical or artistic works to a music company, producer or the like.

9. Category Of Supply Of Services: Copyright Service

Supplier of Service

Music composer, photographer, artist, or the like.

Recipient of Service

The music company, producer or the like, located in the taxable territory.

9A. Category Of Supply Of Services: Copyright Service

Supply of services by an author by way of transfer or permitting the use or enjoyment of a copyright covered under clause (a) of subsection (1) of section 13 of the Copyright Act, 1957 relating to original literary works to a publisher.

(with effect from 1st October, 2019)

Supplier of Service Author

9A. Category Of Supply Of Services: Copyright Service

Provided that nothing contained in this entry shall apply where

(i) the author has taken registration under the Central Goods and Services Tax Act,2017 (12 of 2017), and filed a declaration , in form at annexure I, within the time limit prescribed therein, with the jurisdictional CGST or SGST commissioner, as the case may be, that he exercises the option to pay central tax on the service specified in column (2), under forward charge in accordance with Section 9 (1) of the Central Goods and Service Tax Act, 2017 under forward charge, and to comply with all the provisions of Central Goods and Service Tax Act, 2017 (12 of 2017) as they apply to a person liable for paying the tax in relation to the supply of any goods or services or both and that he shall not withdraw the said option within a period of 1 year from the date of exercising suchoption;

(ii) the author makes a declaration, as prescribed in Annexure II on the invoice issued by him in Form GST Inv-I to the publisher.

Recipient of service

Publisher located in the taxable territory

10. Category Of Supply Of Services: Reserve Bank Services

Supply of services by the members of Overseeing Committee to Reserve Bank of India

(Effective from 13-10-2017)

Supplier of Service

Members of Overseeing Committee constituted by the Reserve Bank of India.

Recipient of service

Reserve Bank of India

11. Category Of Supply Of Services: Services by DSAs

Services supplied by individual Direct Selling Agents (DSAs) other than a body corporate partnership or limited liability partnership firm to bank or non-banking financial company (NBFCs) (Effective from 27-7-2018).

Supplier of Service

Individual Direct Selling Agents (DSAs) other than a body corporate, partnership or limited liability partnership firm.

Recipient of service

A banking company or a non-banking financial company, located in the taxable territory.

12. Category Of Supply Of Services

Services provided by Business Facilitator (BF) to a banking company. (w.e.f 01.01.2019)

Supplier of Service

Business facilitator (BF)

Recipient of service

A banking company, located in the taxable territory.

13. Category Of Supply Of Services

Services provided by an agent of Business Correspondent (BC) to Business Correspondent (BC). (w.e.f. 01.01.2019)

Supplier of Service

Anagent of Business Correspondent (BC).

Recipient of service

A business correspondent, located in the taxable territory.

14. Category Of Supply Of Services

Security Services (services provided by way of supply of security personnel) provided to a registered person (w.e.f. 01.01.2019):

Provided that nothing contained in the entry shall apply to,

(i) (a) a Department or Establishment of the Central Government or State Government or Union territory;or

(b) local authority;or

(c) Government agencies;

which has taken registration under the Central Goods and Services Tax Act, 2017 (12 of 2017) only for the purpose of deducting tax under Section 51 of the said Act and not for making a taxable supply of goods or services; or

(ii) a registered person paying tax under Section 10 of the said Act.

Supplier of Service

Any person other than a body corporate

Recipient of service

A registered person, located in the taxable territory

15. Category Of Supply Of Services

Services provided by way of renting of any motor vehicle designed to carry passengers where the cost of fuel is included in the consideration charged from the service recipient, provided to a body corporate.

(Notification No. 29/2019-Central Tax (Rate), dated 31.12.2019)

Supplier of Service

Any person, other than a body corporate who supplies the service to a body corporate and does not issue an invoice charging central tax at the rate of 6% to the service recipient.

Recipient of service

Any body corporate located in the taxable territory

16. Category Of Supply Of Services

Services of lending securities of Securities under Lending scheme, 1997 (Scheme). Securities and Exchange Board of India (SEBI), as amended.

(with effect from 1st October, 2019)

Supplier of Service

Lender i.e. a person who deposits the securities registered in his name or in the name of any other person duly authorized on his behalf with an approved intermediary for the purpose of lending under the scheme of SEBI.

Recipient of service

Borrower i.e.

a person who borrows the securities under the Scheme through an approved intermediary of SEBI.

Additional Services on which tax is payable by recipient under IGST Act, 2017 on Reverse charge basis under GST

- Two additional services has been notified by the Central Government vide Notification No. 10/2017-Integrated Tax (Rate) Dated 28-06-2017 wherein whole of the tax shall be payable by the recipient on services under Section 5(3) of IGST Act, 2017 on Reverse charge basis.

1. Category of Supply of Services

Any service supplied by any person who is located in a non-taxable territory to any person other than non-taxable online recipient.

(With effect from 01.07.2017)

Supplier of Service

Any person located in a non-taxable territory.

Recipient of service

Any person located in the taxable territory other than non-taxable online recipient.

2. Category of Supply of Services

Services supplied by a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India up to the Customs Station of clearance in India. W.e.f 01.07.2017

Supplier of Service

A person located in a non-taxable territory.

Recipient of service

Importer, as defined in Sec 2(26) of the Customs Act, 1962, located in the taxable territory.

Supply of goods or services by an unregistered supplier to registered recipient under RCM

Applicable for the period 01.07.2017 to 31.01.2019

◊ Section 9(4) of the CGST Act,2017

> The central tax in respect of the supply of taxable goods or services or both by a supplier, who is not registered, to a registered person shall be paid by such person on reverse charge basis as the recipient and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

◊ Section 5(4) of the IGST Act, 2017

> The integrated tax in respect of the supply of taxable goods or services or both by a supplier, who is not registered, to a registered person shall be paid by such person on reverse charge basis as the recipient and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

Applicable with effect from 01.02.2019

◊ Section 9(4) of the CGST Act, 2017

> The Government may, on the recommendations of the Council, by notification,specify a class of registered persons who shall,in respect of supply of specified categories of goods or services or both received from an unregistered supplier, pay the tax on reverse charge basis as the recipient of such supply of goods or services or both, and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to such supply of goods or services or both.

◊ Section 5(4) of the IGST Act,2017

> The Government may, on the recommendations of the Council, by notification,specify a class of registered persons who shall,in respect of supply of specified categories of goods or services or both received from an unregistered supplier, pay the tax on reverse charge basis as the recipient of such supply of goods or services or both, and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to such supply of goods or services or both.

Supply of Goods and Services subject to reverse charge under section 9(4) of CGST/ section 5(4) of the IGST Act (w.e.f.01.04.2019)

1. Category of Supply of goods and services

Supply of such goods and services or both [other than services by way of grant of development rights, long term lease of land (against upfront payment in the form of premium, salami, development charges etc.) or FSI (including additional FSI)] which constitute the shortfall from the minimum value of goods or services or both required to be purchased by a promoter for construction of project, in a financial year (or part of the financial year till the date of issuance of completion certificate or first occupation, whichever is earlier) as prescribed in notification No. 11/2017- Central Tax (Rate), dated 28th June, 2017, at items (i), (ia), (ib), (ic) and (id) against serial number 3 in the Table, published in Gazette of India vide G.S.R. No. 690, dated 28th June, 2017, as amended.

Recipient of goods and services

Promoter

2. Category of Supply of goods and services

♦ Cement falling in Chapter Heading 2523 in the First Schedule to the Customs Tariff Act, 1975 (51 of 1975)(w.e.f.01.10.2019)

♦ Cement falling in Chapter Heading 2523 in the First Schedule to the Customs Tariff Act, 1975 (51 of 1975) which constitute the shortfall from the minimum value of goods or services or both required to be purchased by a promoter for construction of project, in a financial year (or part of the financial year till the date of issuance of completion certificate or first occupation, whichever is earlier) as prescribed in notification No. 11/2017-Central Tax (Rate), dated 28th June, 2017, at items (i), (ia), (ib), (ic) and (id) against serial number 3 in the Table, published in Gazette of India vide G.S.R. No. 690, dated 28th June, 2017, as amended.

Recipient of goods and services

Promoter

3. Category of Supply of goods and services

Capital goods falling under any Chapter in the First Schedule to the Customs Tariff Act, 1975 (51 of 1975) supplied to a promoter for construction of a project on which tax is payable or paid at the rate prescribed for items (i), (ia), (ib), (ic) and (id) against serial number 3 in the Table, in notification No. 11/2017- Central Tax (Rate), dated 28th June, 2017, published in Gazette of India vide G.S.R. No.690, dated 28th June, 2017, as amended.

Recipient of goods and services

Promoter

REGISTRATION

Section 24(iii) of CGST Act, 2017

Persons who are required to pay tax under reverse charge shall be required to be registered under GST. There is no threshold limit for registration for a recipient of RCM supplies.

Section 25(1) of CGST Act, 2017

Every person who is liable to be registered under section 22 or section 24 shall apply for registration in every such State or Union territory in which he is so liable within thirty days from the date on which he becomes liable to registration.

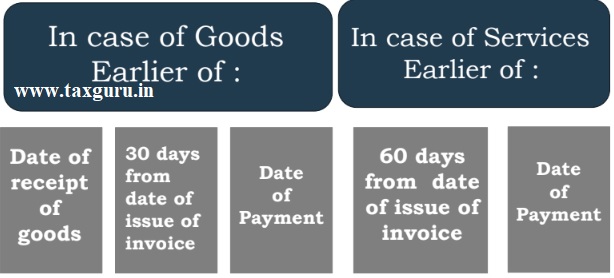

Time of Supply under Reverse Charge Mechanism

In case of Goods:

Section 12(3) of the CGST Act, in case of supplies in respect of which tax is paid or liable to be paid on reverse charge basis, the time of supply shall be the earliest of the following dates,namely

(a) the date of the receipt of goods;or

(b) the date of payment as entered in the books of account of the recipient or the date on which the payment is debited in his bank account, whichever is earlier;or

(c) the date immediately following thirty days from the date of issue of invoice or any other document, by whatever name called, in lieu thereof by the supplier:

Provided that where it is not possible to determine the time of supply under clause (a) or clause (b) or clause (c), the time of supply shall be the date of entry in the books of account of the recipient of supply.

In case of Services:

Section 13(3) of the CGST Act, in case of supplies in respect of which tax is paid or liable to be paid on reverse charge basis, the time of supply shall be the earliest of the following dates, namely

(a) the date of payment as entered in the books of account of the recipient or the date on which the payment is debited in his bank account, whichever is earlier;or

(b) the date immediately following sixty days from the date of issue of invoice or any other document, by whatever name called, in lieu thereof by the supplier.

Provided that where it is not possible to determine the time of supply under clause (a) or clause (b), the time of supply shall be the date of entry in the books of account of the recipient of supply

Provided further that in case of supply by associated enterprises, where the supplier of serviceis located outside India, the time of supply shall be the date of entry in the books of account of the recipient of supply or the date of payment, whichever is earlier.

INVOICING

For supplier of notified goods or services

As per Section 31 of the CGST Act read with Rule 46(p) of the Central Goods and Services Tax Rules, 2017 (“the CGST Rules”), a registered person making supply of goods or services notified under Section 9(3) of the CGST Act / Section 5(3) of the IGST Act shall issue tax invoice containing the specified particulars including ‘whether the tax is payable on reverse charge basis’ by the recipient.

Since an unregistered person does not come within the ambit of GST Law, he is not required to issue any document in respect of supply of goods or services notified under Section 9(3) or 9(4) of the CGST Act/ Section 5(3) or 5(4) of the IGST Act.

INVOICING

For recipient of goods or services under RCM

As per section 31(3)(f) of the CGST Act, a registered person who is liable to pay tax under section 9(3) or section 9(4) shall issue an invoice in respect of goods or services or both received by him from the supplier who is not registered on the date of receipt of goods or services or both.

As per section 31(3) (g) of the CGST Act, a registered person who is liable to pay tax under section 9(3) or section 9(4) shall issue a payment voucher at the time of making payment to the supplier.

Accounts and Records

As per Rule 56(1) of the CGST Rules, every registered person shall keep and maintain, in addition to the particulars mentioned in section 35(1), a true and correct account of the goods or services imported or exported or of supplies attracting payment of tax on reverse charge along with the relevant documents, including invoices, bills of supply, delivery challans, credit notes, debit notes, receipt vouchers, payment vouchers and refund vouchers.

Every registered person, other than a person paying tax under section 10, shall keep and maintain an account, containing the details of tax payable (including tax payable in accordance with the provisions of section 9(3) and section 9(4)), tax collected and paid, input tax, input tax credit claimed, together with a register of tax invoice, credit notes, debit notes, delivery challan issued or received during any tax period.

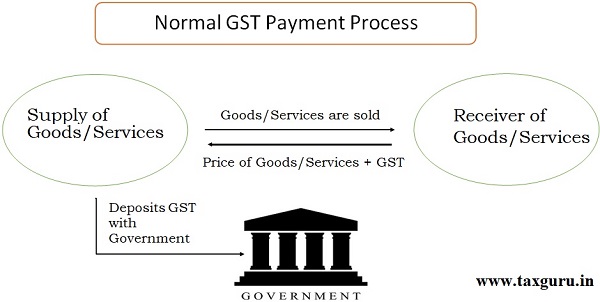

Payment of Tax under RCM

♦ Any liability of tax payable under reverse charge shall be discharged by debiting the electronic cash ledger.

♦ In other words, reverse charge liability cannot be discharged by using input tax credit reflecting in electronic credit ledger.

♦ However, after discharging reverse charge liability, the credit of the same can be claimed by the recipient in the same month itself, if he is other wise eligible.

Input Tax Credit under RCM

♦ In case the supplier is unregistered then the recipient is liable issue a tax invoice under reverse charge towards such receipts and claim ITC against such invoice. However, if the supplier is registered, then he shall issue a tax invoice specifying the supply taxable under reverse charge.

♦ Tax paid on RCM basis shall be available for input tax credit only if such goods and/or services are used, or will be used, in the course or furtherance of business.

Author Bio

Is it allowable to claim exemption even though registration got , if the GST Registration holder’s turnover does not exceed threshold limit? i.e. Just mention service Charges under Exempted without paying any tax

How to declare the Service Charges in GSTR 3B & GSTR 1 while the security Services done by Proprietorship Company ? Since there is no such column available Service Provider how will they declare ? I think it will come under RCM Service Recipient will show the same in their GSTR 3B under Respective columns

DEAR SIR

I HAVE GONE TROUGH THE WRITE UP OF RCM AND IT IS EXPLAINED IN VERY GOOD MANNER. I WOULD LIKE YOU TO GIVE A BRIEF WRITING ON SEC.7(1) AND SCHEDULE I, II AND III. KINDLY EXPLAIN HIGH SEA SALES.