The introduction of the Goods and Services Tax (GST) in India was held as one of the most significant tax reforms in the country. It has ensured rationalization of the economy and reinforced mop-up, producing consistent convergence under the “One nation one tax” idea. Supply under GST has been defined under Section 7 of CGST Act, 2017; which includes in its ambit “rental”. Our discussion in this article inclines towards understanding Taxability of renting of motor vehicle Services under GST Regime.

Renting of Motor vehicle service industry is a booming one in India, further it is very crucial to note that every business entity avails such renting of motor vehicle services and utilizes for frequent day to day operations viz. transportation of employees, guests etc. This article will help you in understanding and decoding taxability of rent of motor vehicle service from 360-degree view, which would include

Following points for discussion as enumerated below: –

1. Analysis of term “Rent of Motor Vehicle”

2. Backdrop of Taxability of Renting of Motor Vehicle Service in Pre-GST Regime i.e. Service Tax Regime

3. Analysis of Taxability of Renting of Motor Vehicle Service under GST Regime

4. Input Tax Credit on Renting of Motor Vehicle Services

5. Other provision relating to renting of motor vehicle services

6. Concluding remarks

In view of aforementioned brief introduction of topic let us elaborate each and every aspect in its entirety.

1. Analysis of term ” Renting of Motor Vehicle”

Renting of Motor vehicle has not been defined under GST. However, we can break the words and interpret the meaning of the term. “Motor Vehicle” has been assigned definition under Motor Vehicles Act, 1988; which is reproduced here for kind reference, “means any mechanically propelled vehicle adapted for use upon roads whether the power of propulsion is transmitted thereto from an external or internal source and includes a chassis to which a body has not been attached and a trailer; but does not include a vehicle running upon fixed rails or a vehicle of a special type adapted for use only in a factory or in any other enclosed premises or a vehicle having less than four wheels fitted with engine capacity of not exceeding 1[thirty-five cubic centimetres]”

It is pertinent to note the following take away from analysis of definition of Motor-vehicle: –

Cabs i.e. Motor Cab, Meter Cab falls under definition of Motor vehicle

Dumper, Tipper, and other such vehicles are not in purview of Motor vehicles

It is quite relevant at this stage to understand the difference between “Renting of Motor Vehicle” &

“Transportation of Passenger”. The following tabular presentation would highlight key difference among these terms.

| Sr no | Particular | Transportation of passenger | Renting of motor vehicle |

| 1 | Classification | 9964 | 9966 |

| 2 | Recipient | Recipient of the service is a passenger | Recipient of the service is not a passenger |

| 3 | Biling basis | Billing will be done to passenger on the basis of distance travelled | Billing will be done to passenger irrespective of distance travelled |

It is renting of motor vehicle which has been critically analysed in this article.

2. Backdrop of Taxability of Rent a Cab Service in Pre-GST Regime i.e. Service Tax (ST) Regime

In erstwhile, service tax regime; Rent a cab service was covered under Reverse charge mechanism followed by abatements thereon. The Central Government has issued Notification No. 30/2012-ST dated 20-06-2012 and reverse charge mechanism (RCM) was applicable on such services.

To summarise, earlier renting of motor vehicle services had been under partial reverse charge mechanism i.e. based on the option selected by service providers with regard to Abatement provisions, % of service tax to be borne by service providers and service receivers used to get decided.

If the service providers were not availing abatement, then 50% of service tax was borne by the service provider and remaining 50% of service tax needs to be payable by service receiver under RCM. However, if Service provider is availing abatement option, then service receiver is liable to pay 100% of service tax payable on abated value under RCM.

This can be easily understood with the help of below table.

| Sr No | Description of services | % of Service tax payable by Service provider | % of Service tax payable by Service receiver |

| 1 | 2 | 3 | 4 |

| 7 | (a) On abated value | NIL | 100%` |

| (b) On non-abated value | 50% | 50 % |

Let us understand tax treatment on renting of motor vehicle services in GST regime.

3. Analysis of Taxability of Renting of Motor Vehicle Service under GST Regime

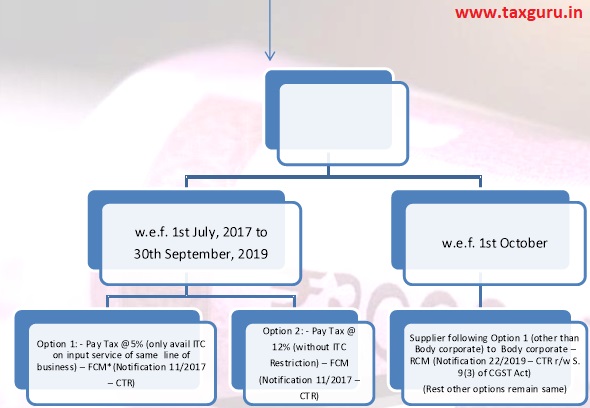

Renting of Motor Vehicle service can be very well categorized into 2 phases in GST Regime viz.

*Forward charge mechanism

3.1 Taxability of Renting of Motor vehicle from 1st July, 2017 to 30th September, 2019

In GST Regime i.e. w.e.f. 1st July, 2017 to 30th September, 2019 as per Sr. No. 10 of Notification 11/2017 -CTR dated 28th June, 2017 any supplier (including body corporates), providing “Renting of Motor Vehicle services’ (where the cost of fuel forms part of the consideration received) were given two option to pay GST which are as below:

(i) 5% GST (i.e. 2.5% CGST & SGST each or 5% IGST) with restriction on availment of input tax credit on goods or services used in supplying the said service, except where input tax credit paid on services availed in the same line of business (hereinafter referred to “Option ̓1″(i.e. only ITC on input service of same line of business is allowed)

(ii) 12% GST with no restriction of ITC [hereinafter referred to “Option 2”]

The aforesaid services were earlier taxable under Forward Charge.

3.2 Taxability of Renting of Motor vehicle w.e.f. 1st October, 2019

GST Council in its meeting held on 20th September, 2019 at Goa, recommended that where the supplier (other than body corporate) is following Option 1 (as mentioned in Para 3.1) prior to 1st October, 2019 and supplying such services to body corporate on or after 1st October, 2019; such transaction would be brought to tax net under reverse charge mechanism. Thus, in such a case body corporate would be liable to pay tax under reverse charge mechanism.

It would be considerable to note here that other mechanism to pay tax as available to supplier prior to 1st October, 2019 would remain unchanged.

In order to give effect to this recommendation, the Central government issued Notification No. 22/2019-CT (R) dated 30th September, 2019 thereby inserting Entry Number 15 in the RCM principal notification (Notification No. 13/2017-CT (R) dated 28.06.2017). The said entry is reproduced below for ready reference:

| Sr no | Nature of service | Service provider | Person liable to pay tax |

| 1 | 2 | 3 | 4 |

| 15 | Services of renting of a motor vehicle provided to a body corporate | Any person other than a body corporate, paying central tax at the rate of 2.5% on renting of motor vehicles with input tax credit only of input service in the same line of business. | Any Body corporate located in the taxable territory. |

Thus, it is very clear that if supplier (other than Body corporate) had opted for option 1, and supplying services to body corporate; body corporate would be liable to pay GST @ 5% as a recipient of such services.

However, he can continue to charge 5% GST on services supplied to non-corporate clients.

It would be worth-while to analyse the term body corporate. The term Body Corporate is not defined in GST Act. But as per section 2(11) of Companies Act, ‘Body Corporate ‘or ‘corporation’ includes a company incorporated outside India, but does NOT INCLUDE-

♦ A co-operative society registered under any law relating to co-operative societies; and

♦ Any other body corporate (not being a company as defined in this Act), which the Central

Government may, by notification, specify in this behalf.

In pursuance to Notification No. 22/2017- Central Tax (Rate), CBIC has removed confusion and made it very clear that LLP shall be considered as Partnership Firm and not body corporate.

The language of the Notification 22/2019 -CT (R) was ambiguous and was being misread by trade and industry due to the usage of the words “Any person other than a body corporate, paying central tax at the rate of 2.5%”

Such doubts arising thereof, is a result of incorrect interpretation of law, which made it difficult for the assesses to follow the aforesaid amendment, thus rendering the above notification unworkable. However, trade & industry failed to give a thought to nature of services rendered under RCM. RCM is only attracted where services are provided to corporate entities. Supplier would be still liable to discharge 5% tax (FCM) on supply of such services to non-corporate entities. Nonetheless, CBIC came up with circulars to explain this point and ensure smooth implementation of this entry.

To remove the anomalies, Central Government issued Notification No. 29/2019 Dated 31st December, 2019 which was clarificatory in nature and was effective from 1st October, 2019 itself. In the said notification, in the Table, for Serial Number 15 and the entries relating thereto, the following shall be substituted, namely:-

| Sr No | Nature of service | Service provider | Person liable to pay tax |

| 1 | 2 | 3 | 4 |

| 15 | Services provided by way of renting of any motor vehicle designed to carry passengers where the cost of fuel is included in the consideration charged from the service recipient, provided to a body Corporate. |

Any person, other than a body corporate who supplies the service to a body corporate and does not issue an invoice charging central tax at the rate of 6 per cent to the service Recipient. |

Any Body Corporate located in the taxable territory. |

Department issued circular to delineate wordings mentioned in above two notifications vide Circular No. 130/49/2019-GST dated 31st December, 2019.

Circular stated that RCM shall be applicable on the service by way of renting of any motor vehicle designed to carry passengers where the cost of fuel is included in the consideration charged from the service recipient ONLY IF the SUPPLIER fulfills all the following conditions: –

a) is other than a body-corporate;

b) does not issue an invoice charging GST @12% (6% CGST + 6% SGST) from the service recipient; and

c) supplies the service to a body corporate.

In any other case FCM would be applicable

Following Illustrations would clarify the present position of Renting of Motor Vehicle Services

(Limited ITC -ITC only on Input Services in same line of business)

| Sr no | Supplier | Recipient | GST Rate | Charge |

| Service supply by persons “other than body corporate” | ||||

| 1 | Supplier other than Body corporate (Following Option 1) | Body corporate | 5% | RCM |

| 2 | Supplier other than Body corporate (Following Option 2) | Body corporate | 12% | FCM |

| 3 | Registered Supplier other than Body corporate | Other than Body corporate | 12% with ITC or 5% with limited ITC | FCM |

| 4 | Unregistered Supplier other than Body corporate | Other than Body corporate | Not taxable | N.A |

| 5 | Unregistered Supplier other than Body corporate | Body corporate | 5% | RCM |

| Services supply by body corporates | ||||

| 6 | Body corporate | Body corporate | 12% with ITC or 5% with limited ITC | FCM |

| 5 | Body corporate | Other than body corporate | 12% with ITC or 5% with limited ITC | FCM |

4. Input Tax Credit (ITC) of Renting of Motor Vehicle Services

Chapter V of CGST Act deals with input tax credit. The availment or otherwise of Input Tax Credit forms the cornerstone in a GST regime. GST can be understood as a system of value-added tax on goods and / or services. It is these provisions of Input Tax Credit that make GST a value-added tax i.e., collection of tax at all points in the supply chain after allowing for credit of taxes paid on inputs / input services and capital goods.

However, GST Laws restrict ITC on various procurements as outlined u/s 17(5) of CGST Act, 2017.

One such blocked credit is on Renting of Motor Vehicle services subject to certain conditions (analyzed in detail in later paras of article).

We would be analysing ITC provisions from both supplier’s & recipient’s perspective.

There are following transactions in which ITC treatment is different on renting of motor vehicle.

4.1 ITC to Suppliers providing services taxable under RCM @ 5% (Entry No. 15): –

It would be appropriate to understand the nature of services provided by supplier whose services are taxable under RCM. As per section 17(3) of CGST Act, 2017 “. The value of exempt supply under subsection (2) shall be such as may be prescribed, and shall include supplies on which the recipient is liable to pay tax on reverse charge basis, /… sale of building.”

Accordingly, if a person is supplying services which are taxable under reverse charge, he is deemed to be supplying exempt supplies.

Further, due consideration shall be given to Section 17(2) of CGST Act which is reproduced below for easy reference, “Where the goods or services or both are used by the registered person partly for effecting taxable supplies including zero-rated supplies under this Act or under the Integrated Goods and Services Tax Act and partly for effecting exempt supplies under the said Acts, the amount of credit shall be restricted to so much of the input tax as is attributable to the said taxable supplies including zero-rated supplies”.

As per section 17(2) of CGST Act; if a person is supplying exempt services, he would be liable to reverse input tax credit on common credit as is attributable to such exempt supplies by following Rule 42 of CGST Rules.

Now, let us draw our attention to the impact on phase of transition meaning thereby the registered suppliers following option 1 whose supplies will be covered under reverse charge w.e.f. 1st October, 2019. As per Option 1 prevailing before 1st October, 2019; the supplier was eligible for ITC only on input services procured in same line of business. As per section 18(4) read with Section 17(3), when taxable supply becomes exempt supplies any supplier having ITC in electronic credit ledger shall be liable to be reversed. (after reducing ITC on capital goods & ITC on stock, however, in case of supplier following option 1 credit of inputs & CG does not arise).

However, if person is supplying taxable supplies as well as exempt supplies, ITC shall be reversed in accordance with rule 42 of CGST Rules in the ratio of exempt to total turnover.

4.2 ITC to Suppliers providing services taxable under FCM @ 5%: –

Supplier can continue to charge 5% GST (FCM) on services supplied to non-corporate clients as per Option 1 and accordingly they would be eligible to take ITC of input services availed in same line of business.

4.3 ITC to Suppliers providing services taxable under FCM @ 12%: –

Suppliers may opt to pay tax under option 2 i.e. 12% FCM with full ITC. In such a case they would be eligible to take full ITC as per normal provisions of GST. However, it can be noted that as per section 17(5)(a) of CGST Act, 2017 as amended by CGST Amendment Act, 2018,ITC shall not be eligible on Motor vehicles for TRANSPORTATION OF PERSONS which has approved seating capacity of less than or equal to 13 persons (including the driver).

However, credit will be available when they are used for making the following taxable supplies, (accordingly, in below mentioned situations seating capacity need not be checked i.e. even if seating capacity is below 13 in below scenario ITC will still be eligible).

♦ Further supply of such motor vehicles;

♦ Transportation of passengers;

♦ Imparting training on driving such motor vehicles (Driving Schools);

It can be seen from above that renting of motor vehicle does not fits into exception of ineligibility, meaning thereby if a renting of motor vehicle supplier has purchased motor vehicle for renting services and is having sitting capacity of less than or equal to 13 then credit shall not be available.

However, considering principal of natural justice & seamless flow of credit under GST it appears that the denial of ITC would be unjust on the part of supplier. It is interesting to note that if a supplier is engaged in transportation of passenger services and purchases motor vehicle for providing such service, he would be eligible to take ITC as “Transportation of Passengers” is an exception to ineligible ITC but ” Renting of motor vehicle” is not.

In erstwhile Service Tax regime, there were many cases on disallowance of CENVAT Credit on rent-a-cab services, in Judicial pronouncement of Commissioner of Service Tax vs. Vijay Travels it was concluded that “renting” and “hiring” are synonymous and there is no difference. However, High court failed to give consideration to nature of service provided through hiring & renting. “Renting” and “Hiring” may be synonymous in context of motor vehicle however differs from services of transportation of passengers where service provider retains effective control & possession of vehicle. High court declared that even services are rendered through bus or cars it would be a rent a cab and thus ineligible.

However, in GST Regime w.e.f. 1st February, 2019; vide CGST Amendment Act, ITC would be eligible for more than 13-seater capacity vehicle. For instance, if bus has procured to provide renting services then ITC would be eligible, however if car is purchased for providing renting services then ITC would be blocked.

4.4 ITC to recipient of services for tax charged by supplier under FCM or paid by recipient under RCM basis: –

As per section 17(5)(b)(i) recipient availing services of rent-a-cab leasing, renting or hiring of motor vehicles for transportation of persons having approved seating capacity of not more than thirteen persons (including driver) (substituted vide CGST Amendment Act, 2018) would not be eligible to take input tax credit except when used for specified purposes therein.

It is crucial to note that in the following 2 cases credit would be eligible even if the vehicle has seating capacity of less than or equal to 13 passengers.

♦ Inward Supply is used by a registered person for making an outward taxable supply of the same category of goods or services or both or as an element of a taxable composite or mixed supply or, (Example: – Event Management company avails rent a cab service for pick up & drop facility for guests of event. The ITC would be eligible to event management company as the services are availed as composite supply of event management and not a standalone supply)

♦ It is obligatory for an employer to provide the same to its employees under any law

(Example: – If as per certain Law, rent-a-cab facility has to be provided by employer to night shift employees & female employees leaving office after certain time in night, ITC would be eligible to such employer)

5. Other provision relating to renting of motor vehicle services

5.1 Place of Supply of Renting of Motor vehicle Services: –

Further to note that, it is important to determine the place of supply of goods or services to determine the nature of tax to be paid. Section 12 of IGST Act, 2017 deals with the determination of Place of Supply of services where location of service provider and service recipient is in India.

Section 12(2) of IGST Act, 2017 states the general provisions for determining place of supply of services: –

| Different cases | Place of supply of services |

| 1. Supply made to a registered person | Location of recipient |

| 2. Supply made to an unregistered person (Location of recipient available) | Location of recipient |

| 3. Supply made to an unregistered person (Location recipient not available) | Location of recipient |

Section 13 of IGST Act, 2017 deals with the determination of place of supply of services where location of service provider or service recipient is outside India.

Section 13(2) of IGST Act, 2017 states the general provisions for determining place of supply of services: –

| Different cases | Place of supply of services |

| 1. Supply made to an unregistered person (Location of recipient available) | Location of recipient |

| 2. Supply made to an unregistered person (Location recipient not available) | Location of recipient |

(Please note that provisions of Section 12(9) of IGST would not be applicable as Section 12(9) is applicable for passenger transportation and not for renting of motor vehicle)

5.2 Time of Supply

a) Renting of Motor Vehicle Services Taxable on RCM basis:

As per section 13(3) of CGST Act, 2017; the time of supply for body corporate paying tax under reverse charge shall be earlier of the following dated;

| 1. Date of payment as entered in the books of account of the recipient or the date on which payment is debited in his bank account whichever is earlier. |

| 2. The Date immediately following 60 days from the date of invoice or any other document issued by the supplier |

| 3. Where it is not possible to determine the time of supply from the above, the time of supply will be the date of entry in the books of accounts of the recipient of supply. |

b) Renting of Motor Vehicle Services Taxable on FCM basis:

As per section 13(2) of CGST Act, 2017; If invoice issued within time limit of 30 days from provision of service; the time of supply shall be date of issue of Tax Invoice or Receipt of payment whichever is earlier.

However, if invoice is not issued within Time Limit the time of supply shall be date of provision of service or receipt of payment whichever is earlier.

5.3 Registration under GST Law:

a) Registration for suppliers supplying services under FCM (S. 22 of CGST Act)

As per section 22 of CGST Act, 2017; every supplier shall be liable to be registered under GST Act in the State or Union territory, from where he makes a taxable supply of goods or services or both, if his aggregate turnover in a financial year exceeds Rs. 20 Lakhs / 10 Lakhs in case of Special Category States (Tripura, Nagaland, Manipur, Mizoram).

b) Registration requirement for suppliers supplying services under reverse charge mechanism (S. 23 of CGST Act)

It is equally important to look upon at provisions of Section 23 of CGST Act, 2017 which states that the persons who are only engaged in making outward taxable supplies, the total tax on which is liable to be paid on reverse charge basis by the recipient under section 9(3) of the said Act, then such category of persons are exempted from obtaining registration under the aforesaid Act. (Section 23 r/w Notification No.5/2017- Central Tax dated 19th June, 2017).

Accordingly, we can very well come to a conclusion that, if supplier of service (other than body corporate) providing services exclusively to a body corporate would not be liable to obtain registration under GST in pursuance to above provisions.

c) Registration requirement for recipient receiving services under reverse charge mechanism (S. 24 of CGST Act)

Section 24 of the CGST Act, states that persons who are required to pay tax under reverse charge i.e. such recipient who is availing services specified in section 9(3) shall be liable to obtain mandatory registration under GST inspite of their turnover being lesser than threshold exemption limit.

Further as per section 49 of CGST Act read with CGST Rules thereon the liability of GST on account of reverse charge shall be payable in cash i.e. ITC cannot be utilised to pay tax under reverse charge.

6. Concluding Remarks

Reverse Charge Mechanism provisions caste statutory obligation on the body corporate to pay tax to government where services are received from supplier other than body corporate paying tax under option 1. Thus, all contracts between suppliers & recipients shall be aligned to applicable legal provisions to avoid legal issues in near future.

Thank you

Compiled By

CA Rohit Aggarwal

B.com, M.com, CA, CS (F)

GST Ki Shiksha

Author Bio

3. Supply made to an unregistered person (Location recipient not available) Location of recipient

Here in case the address of recipient does not exist on record, then place of supply of service would be the location of the supplier

Self driven cars rental – gst rate pls?

I have bought a commercial vehicle in 22 February 2020 for rental services which is a mini truck and I have registered to GST on 26 June 2020 , And my vehicle is working for Rental Services on contract with State Government Corporation Department , Can I claim ITC on my purchase of this vehicle ??

This analysis holds relevance only for Renting of Passenger Vehicles or even for Renting of Goods Carriers?

Very Good and Informative Article.

I have one Question regarding this

Our vendor will providing us Bus (Seating Cpacity more than 13 Person) charging 18% gst on invoice.

Bill Valur inclusive of Driver & Petrol and having SAC Code – 996601. Can we eligable to take ITC.