Ronak Kothari

GST stands for “Goods and Services Tax”, the biggest reform in India’s indirect tax structure since the economy began to be opened up 25 years ago

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as services at the national and state level. It will replace majority of indirect taxes levied on goods and services by the Indian Central and State governments.

With GST being an indirect tax it will affect the stakeholders majorly being the common man doing business in day to day affair. The Government is trying to simplify the process as much as possible for easiness of the whole process. Various state departments were having different application requirement of Assessee. Thus availability of uniform details was difficult. So the concept of provisional basis certification was developed.

As per the Model GST Law Assessee falling under the following categories can get themselves registered :

A) Mandatory Registration

B) Voluntary Basis Registration

Mandatory Registration Reason

1. Due to crossing the threshold prescribed.

2. Due to Inter-State Supply

3. Due to liability to pay as recipient of services (Reverse Charge)

4. Due to transfer of business which includes change in the ownership of business (if transferee is not a registered entity)

5. Due to death of the Proprietor (if the successor is not a registered entity)

6. Due to de-merger behalf of other registered taxable persons

7. Due to change in constitution of business

8. Due to Merger /Amalgamation of two or more registered taxpayers

9. Role of an Aggregator

10. E-Commerce operator (other than facilitator to supply goods and/or services of other suppliers)

11. Taxpayer selling through e-Commerce portal

12. Input Service Distributor only

13. Persons supplying goods and/or services on

14. Other as Specified by the Government (Not covered above)

Now for the Registration process government has divided the whole process under 2 major parts:

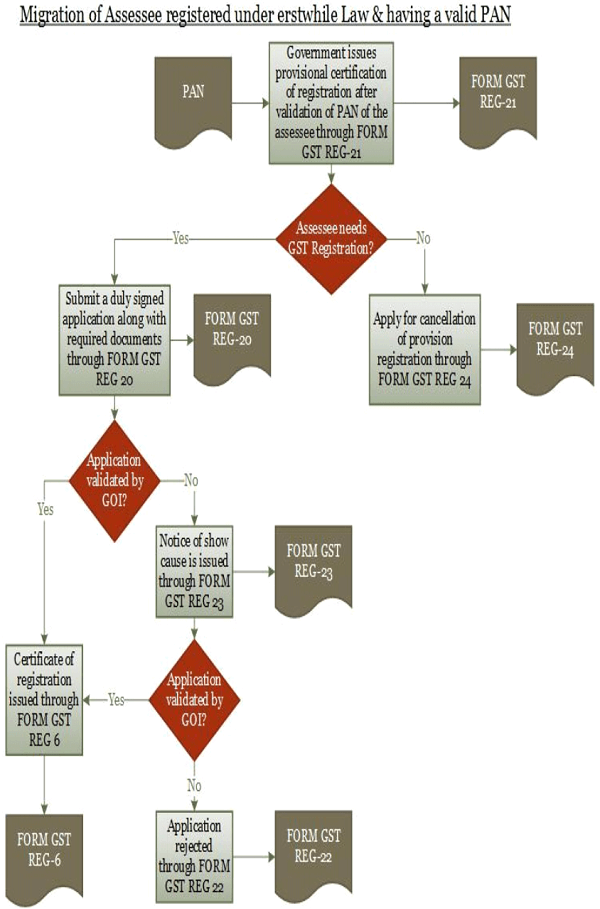

A) Every person registered under an earlier law and having a Permanent Account Number (PAN) issued under the Income Tax Act, 1961.

B) Other Assessee not falling under “Clause A” above.

Every person registered under an earlier law and having a Permanent Account Number

(PAN) issued under the Income Tax Act, 1961.

Other Assessee not falling under “Clause A”above –Fresh Application

Other Assessee not falling under “Clause A”above –Fresh Application

Above are the draft GST rules for registration. There may or may not be any changes on the final act.

Above are the draft GST rules for registration. There may or may not be any changes on the final act.

Thanks for your process to get clear, in current synario AC in Central Excise issuing the new RC, the same will continue or we need to approach Commissioner to get the new RC for GST. Where to apply & when to apply?. pl. clarify