♦ INTRODUCTION

Assessment means determination of tax liability. There are several types of assessments in the GST regime i.e., self-assessment, provisional assessment, summary assessment and best judgment assessment. Under GST, an assessee is first required to self- assess his tax liability and furnish returns for declaring the taxable turnover, tax payable or refundable, input tax credit availed etc. (i.e., self-assessment). At this stage, there is no intervention by the tax officials.

Since the tax regime relies on self-assessment, there is a need to put in place a robust ‘audit’ mechanism in order to measure and ensure proper compliances of the provisions of law by the taxable person.

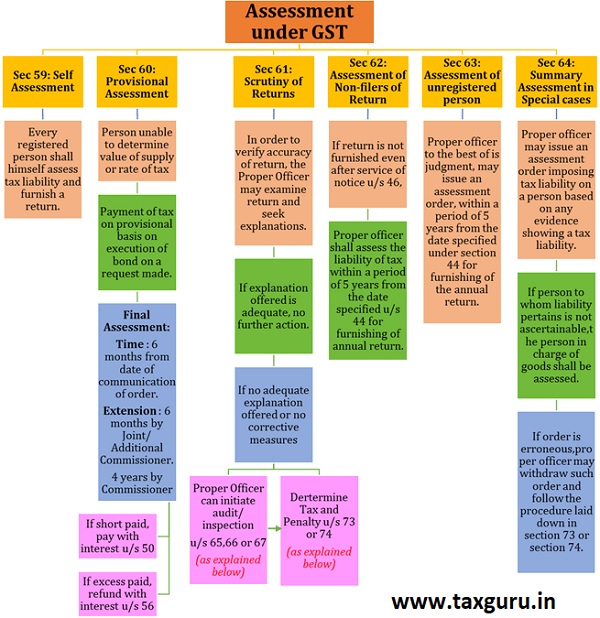

♦ SECTION 59 TO 64: DIFFERENT TYPES OF ASSESSMENT UNDER GST

♦ SECTION 65 TO 66: AUDITS UNDER GST

| Audits | |

| Sec 65: Audit by Tax Authorities | Sec 66: Special Audit |

| Commissioner or any officer authorized by him may undertake audit of any registered person | At any stage of scrutiny, inquiry or investigation |

| Audit may be conducted at the place of business or in their office | Assistant Commissioner is of the opinion that the value has not been correctly declared or the credit availed is not within the normal limits |

| At least 15 days prior notice should be given | May nominate a Chartered Accountant or Cost Accountant |

| Time Period: 3 months from the date of conduct of audit | Time period: 90 days |

| Extension: not exceeding six months | Extension: 90 days |

| On conclusion, registered person shall be informed about findings, rights and obligations | Audit will be conducted even if accounts have already been audited |

| If result in demand of tax, proceedings may be initiated under section 73 or 74 | If result in demand of tax, proceedings may be initiated under section 73 or 74 |

♦ SECTION 73 & SECTION 74: DETERMINATION OF TAX NOT PAID/ SHORT PAID / ERRONEOUSLY REFUNDED/ ITC WRONGLY AVAILED/ UTILISED

| S.No | Action by tax payer | Amount of penalty payable | Remarks | |

| Normal Cases | Fraud Cases | |||

| 1 | Tax amount, along with the interest*, paid before issuance of notice | No penalty and no notice shall be issued | 15% of the tax amount payable as penalty and no notice shall be not be issued | The penalty shall also be not chargeable in cases where the self-assessed |

| 2 | Tax amount, along with the interest, paid within 30 Days of issuance of notice | No penalty. All proceedings deemed to be concluded | 25% of the tax amount payable as penalty. All proceedings deemed to be concluded. | Tax or any amount collected as tax is paid (with interest) within 30 days from the due date of payment. |

| 3 | Tax amount, along with the interest paid within 30 days of communication of order | 10% of the tax amount or Rs. 10,000/-, whichever is higher | 50% of the tax amount payable as penalty. All proceedings deemed to be concluded. | |

| 4 | Tax amount, along with the interest paid after 30 days of communication of order | 10% of the tax amount or Rs. 10,000/-, whichever is higher | 100% of the tax amount | |

*Interest shall be applicable as per section 50 at rate of 18%/24% respectively.

♦ TIME LIMIT FOR ISSUANCE OF NOTICE AND ORDER

| S. No | Nature of case | Time for issuance of notice | Time for issuance of order |

| 1 | Normal case | Within 2 years and 9 months from the due date of filing Annual Return for the Financial year to which the demand pertains or from the date of erroneous refund | Within 3 years from the due date of filing of Annual Return for the Financial Year to which the demand pertains or from the date of erroneous refund |

| 2 | Fraud Cases | Within 4 years and 6 months from the due date of filing of Annual Return for the Financial Year to which the demand pertains or from the date of erroneous refund | Within 5 years from the due date of filing of Annual return for the Financial Year to which the demand pertains or from the date of erroneous refund |

| 3 | Any amount collected as tax but not paid | No time limit | Within 1 year from the date of issuance of notice |

| 4 | Non-payment of self-assessed tax | No need to issue a SCN | Recovery proceedings can be started directly |

CONCLUSION:

Assessments have been initiated by the GST department for the previous years. It is thus required for the assessee to understand the nature of assessment and be prepared for responses. As a proactive measure, an Assessee shall maintain proper documentation of all required records, sales reco, ITC reco and be prepared for scrutiny from department.

Authors:

CA Shreyans Dedhia | Partner |shreyans.dedhia@masd.co.in

Meet Faria | Associate Consultant |meet.faria@masd.co.in

Author Bio

THE SID TAX GURU SIDTE NOT AT PROPERLY DISPLAED FORM LAST WEEK PLEASE BE OPENNED THE TAX GURU SITE

Kindly clear your web history and retry