Section 49 of CGST provides for three kind of ledger:

– Electronic cash ledger

– Electronic credit ledger

– Electronic liability ledger

A] Electronic cash ledger

– Every deposit made for tax, interest, penalty and fees shall be credited to Electronic Cash Ledger in Form- GST PMT-5.

– Taxes, Interest, Fees and Penalty shall be paid by taxable person in any of the following mode.

√ Internet banking

√ Debit or credit card

√ NEFT or RTGS

√ Over the counter payment in authorized banks for deposit up to Rs. 10000 per challan per tax period by cash, cheque or demand draft.

– Registered Person will create challan on GST PMT-6 on the common portal and enter the detail of amount to be deposited by him towards tax, fees, penalty and interest.

– Challan created above shall be valid for 15 days

– On success credit to the Government account, CIN shall be created. If the CIN is not generated then registered person may filed GST PMT -07to bank through the common portal.

B] Electronic credit ledger

B] Electronic credit ledger

– The input tax credit of registered person on self assessed basis in the return of taxable person shall be credited to his Electronic Credit Ledger on the common portal in Form –GST PMT-2.

– The electronic credit ledger may include the following: –

√ ITC from inward supply from registered person.

√ ITC from ISD

√ ITC on stock immediately preceding the day when registered person is liable for payment of tax.

√ ITC available on payment made on reverse charge.

– Registered Person upon noticing any problem can apply on GST PMT-04on common portal.

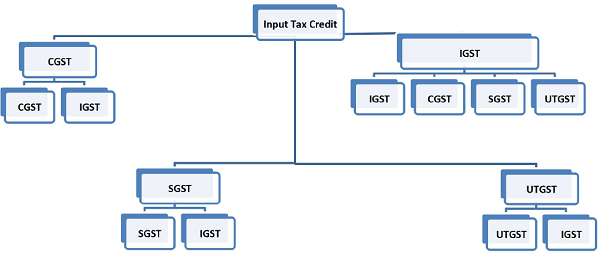

– Manner of Utilization of ITC

Amount of input tax credit in IGST, CGST, SGST or UTGST shall be utilized in the following sequence as shown below

C] Tax Liability Ledger

– Tax, Interest, Penalty & Fine payable by taxable person shall be debited in Electronic Liability Register in Form- ‘GST PMT-01.

– Payment of every liability by registered taxable person shall be by debiting the electronic credit ledger and crediting the electronic liability register.

D] Interest on delayed payment of Tax [Section 50]

– Every person liable to pay tax and fails to pay the same on due date, shall pay interest on unpaid amount at the rate of 18% from the due date of payment of tax to the date of payment. Interest shall be paid to the account of central or State Government.

– Interest shall be paid from the first day on which such tax was due.

– In case taxable person claim excess input credit and or reduction in output tax liability, shall be liable to pay interest at the rate of 24% on such amount excess claimed or reduction in output tax liability.

E] For Your Information: Situation when interest is payable

– Delay in payment of Tax – Interest rate@18%

– Undue or excess claim of ITC- Interest rate@24%

– Excess reduction in Output tax liability- Interest rate@24%.

– Tax return u/s 39 shall be valid only if the tax payable as per the return is paid in full.

– Section 73[5] and 73[6] provide that if the interest is paid, adjudicating authority shall not serve any show cause notice.

– Section 78 provides that where show cause notice has been issued but the interest is paid within 30 days of issue of notice , no penalty in this case shall be payable and case shall be concluded there only