As per Notification No. 9 dated 28.6.2017 of integrated Tax Rate, entry no. 13 under SAC 9963 or 9972, Services by way of renting of residential dwelling for use as residence is exempt from GST . Hence no GST is chargeable.

According to Schedule –II , clause -2[b]

(b) any lease or letting out of the building including a commercial, industrial or residential complex for business or commerce, either wholly or partly, is a supply of services.

Accordingly Schedule-II clause -2 [b] say that

Building used commercial, industrial or residential complex used for business or commerce shall be treated as supply will subject GST . Let us take the definition of Business Section -2(17).

Section -2(17) “business” includes––

(a) any trade, commerce, manufacture, profession, vocation, adventure, wager or any other similar activity, whether or not it is for a pecuniary benefit;

(b) any activity or transaction in connection with or incidental or ancillary to sub-clause (a);

(c) any activity or transaction in the nature of sub-clause (a), whether or not there is volume, frequency, continuity or regularity of such transaction;

(d) supply or acquisition of goods including capital goods and services in connection with commencement or closure of business;

(e) provision by a club, association, society, or any such body (for a subscription or any other consideration) of the facilities or benefits to its members;

(f) admission, for a consideration, of persons to any premises;

(g) services supplied by a person as the holder of an office which has been accepted by him in the course or furtherance of his trade, profession or vocation;

(h) services provided by a race club by way of totalisator or a licence to book maker in such club ; and

(i) any activity or transaction undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities;

Certainly this is business or commerce .

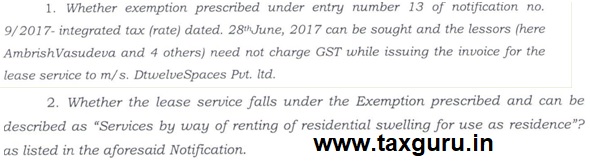

in this case of AAR Karnataka in case Tushar Vasudeva Ambrish in re-[2020] 116 taxmann.com 373

Advance Ruling were sought on the following

Fact of Case

1. Copy of the lease deed between the applicant and company DSPL that lessor [totally five in nos.] have collectively have leased out their premises to company by way of single agreement. Each of the lessor has own a part of the property and they have pooled and given to company. Description of the Property consist of 42 rooms total 2400 sft. area along a terrace . Contract is settle at Per month rental and pool the income and Kept their respective share.

2. Para 12 of the agreement proof that lessee has taken sub-lessee right to the same property .

3. Lessor has not provided any detail of group of partnership or group of individual, hence the taxability of the same were not clear.

4. Regarding the nature of transaction , it is seen from the agreement that lessor are providing the services of leasing / rent of immovable property for a consideration.

4. Regarding the nature of transaction , it is seen from the agreement that lessor are providing the services of leasing / rent of immovable property for a consideration.

A. Lessor has provided to transfer right to use the property without transfer of ownership. For which they are receive as rent for transfer of right to use the property. This is the Course or furtherance of business as the section-7 of CSGT Act 2017 and transaction between company and lessor constitute supply. Further this would be supply of services as per section 7 (1 A) CGST Act,2017 read with Schedule –II ,entry no. 2[b] which as follows:

“any lease or letting out of the building including a commercial, industrial or residential complex for business or commerce, either wholly or partly, is a supply of services”.

B. Hence the lessor , which is applicant is part, is providing a services leasing a building for business or commerce the company . Applicant is not individual providing a services, but as group of person they are providing the service, after pooling the assets.

5. As related to First Question – ‘”Entry no. 13 under SAC 9963 or 9972, Services by way of renting of residential dwelling for use as residence”

As this is related to “renting of residential dwelling “ for use as residential. The contracts with applicant group with the company is verified and found that what is given as immovable property consisting of rooms as attached toilet as per the layout the premises annexed to the leased agreement and does not fit in to the meaning of dwelling which means house. They are like hotel rooms the entire leased premises has 42 rooms , which by no imagination can be termed as residential dwelling. Even if the same is given residential purpose, services provided is not used as residence by the lease. Service by hotel, inn , Camp site club site . by what ever names calls, or other commercial places for residential or for lodging purpose covered are different entries in schedule of this notification or under different Notification.

Hence entry no. 13 does not apply, it has been chargeable in GST.

Disclaimer : The contents of this article are solely for information and knowledge and does not constitute any professional advice or recommendation. Author does not accept any liability for any loss or damage of any kind arising out of this information set out in the article and any action taken based thereon.

About the Author: Author is Sr. Partner of G R A N D M A R K & ASSOCIATES , Chartered Accountants in Gurugram [ Haryana] and Domain Head of GST Department of GMA . He can be reached at sanjeev.singhal@grandmarkca.com. WWW. grandmarkca.com