An opportunity to put rest to age old Pre-GST Litigation

Recently, the Maharashtra Government introduced an Amnesty Scheme to settle all open tax disputes pertaining to pre-GST era. This was introduced by passing an ordinance, namely, Maharashtra Settlement of Arrears of Tax, Interest, Penalty or Late Fee Ordinance, 2019.

The intention behind the introduction of the said scheme is to put an end to the age old litigations under the Pre-GST era by way of settlement between the tax payer and Government. Also to enable to government departments to effectively contribute towards effective GST implementation and its challenges.

The amnesty scheme essentially provides for settlement of Pre-GST tax disputes by way of waiver of certain percentage of Tax demand, Interest & penalty in relation to these tax disputes.

Scope of Legislations Covered under the Amnesty Scheme

Tax Disputes covered under the following legislations inter-alia can be looked at for the purposes of availing this scheme.

- Central Sales Tax Act, 1956

- Bombay Sales Tax Act, 1959

- Maharashtra Value Added Tax, 2002

- Maharashtra Tax on Entry of Goods into Local Areas Act, 1987

- Maharashtra Tax on Luxuries Act, 1987

- Maharashtra Purchase Tax on Sugarcane Act, 1962

- Maharashtra State Tax on professions, Trades, Callings and Employees Act, 1975

- Maharashtra Sales Tax Act on the transfer of right to use any goods for purposes Act, 1985

- The Bombay Sales of Motor Spirit Taxation Act, 1958

Tax Disputes Period Covered

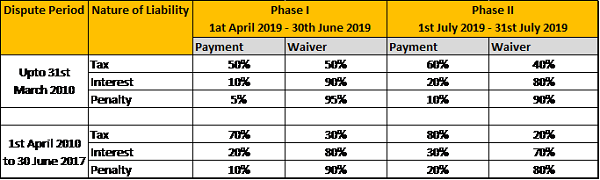

The amnesty scheme provides for coverage of all open tax disputes upto 30th June 2017. However, the period of coverage is split into two categories:

Category 1 – Prior to 1st April 2010

Tax disputes falling under this category are eligible for higher percentage of waiver of tax demand, Interest & Penalty in comparison to Category 2.

Category 2 –1st April 2010 to 30th June 2017

Tax disputes falling under this category are eligible for lower percentage of waiver of tax demand, Interest & Penalty in comparison to Category 1.

Time Line for submitting the Applications

Further, the Amnesty scheme provides two time frames for submission of applications seeking settlement under this scheme.

Application from 1st April 2019 to 30th June 2019

Applications submitted within 30Th June 2019 would be entitled to higher waiver in comparison to applications submitted after 30th June 2019.

Application from 1st July 2019 to 31st July 2019

Applications submitted after 30Th June 2019 would be entitled to lower waiver in comparison to applications submitted before 30th June 2019.

Thus, from above, it is clear that the waiver is dependent on both the timeframe when the application is submitted as well as the tax dispute period.

Snapshot on waiver percentage envisaged in Amnesty Scheme

| Pros | Cons |

| An opportunity to settle prior GST Tax disputes at once | Applicant is required to give unconditional withdrawal of appeals before any appellate authority, Tribunal or Court. |

| Waiver of not just the tax demand but also Interest & penalty | Applicant would be required to immediately pay the tax demand arising on Settlement on or before making the application. |

| Time savings and carrying cost of continuing age old litigations reduced. | In case the credit of Input Tax have been transitioned to GST, then applicant is required to reverse the credit equivalent to the amount for which settlement is desired. |

| Application can be submitted online | Remand back cases where orders not passed on or before 15th July 2019 will not be considered for the purposes of this Scheme. |

Conclusion

This is indeed a great opportunity to resolve age old litigations. However, one needs really evaluate the cost benefit that one may achieve by availing this scheme or are they better off not availing. In my view, where the probability of winning such litigations are not very likely then one should look at availing this scheme. It is possible in certain cases, especially in case of age old litigations, the interest and penalty cost are so huge that sometimes, its even more than the tax demand amount itself. In such cases, it beneficial for tax payers to avail such scheme.

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the policy or position of any other agency, organization, employer or Company.