Seeks to clarify the extension in time under sub-section (1) of section 30 of the Act to provide a one time opportunity to apply for revocation of cancellation of GST registration on or before the 22nd July, 2019 for the specified class of persons for whom cancellation order has been passed up to 31st March, 2019. Refer vide Circular No. 99/18/2019-GST dated 23rd April 2019.

Revocation of cancellation of registration

- One time opportunity to apply for revocation of cancellation given up to 22nd July, 2019 ( ROD Order issued)

For cancellation without retrospective effect:

- All returns due till the date of such cancellation are required to be furnished before the application for revocation can be filed

- All returns due for the period from the date of the order of cancellation of registration till the date of the order of revocation of cancellation of registration shall be furnished by the said person within a period of 30 days from the date of order of revocation of cancellation of registration.

For cancellation of registration with retrospective effect:

- The common portal does not allow furnishing of returns after the effective date of cancellation

- A third proviso has been added to rule 23(1) of the said Rules enabling filing of application for revocation of cancellation of registration, subject to the condition that all returns relating to the period from the effective date of cancellation of registration till the date of order of revocation of cancellation of registration shall be filed within a period of thirty days from the date of order of such revocation of cancellation of registration.

Circular No. 99/18/2019-GST

F.No. CBEC–20/16/04/2018– GST

Government of India

Ministry of Finance

Department of Revenue

Central Board of Indirect Taxes and Customs

GST Policy Wing

New Delhi, Dated the 23rd April 2019

To,

The Principal Chief Commissioners/ Chief Commissioners/ Principal Commissioners/ Commissioners of Central Tax (All)

The Principal Director Generals/ Director Generals (All)

Madam/Sir,

Subject: Clarification regarding filing of application for revocation of cancellation of registration in terms of Removal of Difficulty Order (RoD) number 05/2019-Central Tax dated 23.04.2019 – Req.

Registration of several persons was cancelled under sub-section (2) of section 29 of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as “the said Act”) due to non-furnishing of returns in FORM GSTR-3B or FORM GSTR-4. Sub-section (2) of section 29 of the said Act empowers the proper officer to cancel the registration, including from a retrospective date. Thus registration have been cancelled either from the date of order of cancellation of registration or from a retrospective date.

2. Representations have been received that large number of persons whose registration were cancelled could not apply for revocation of the said cancellation of registration within the period of 30 days as provided in sub-section (1) of section 30 of the said Act. Accordingly, a Removal of Difficulty Order (RoD) number 05/2019-Central Tax dated the 23rd April, 2019 has been issued wherein persons whose registrations have been cancelled under sub-section (2) of section 29 of the said Act after they were served notice in the manner provided in section clause (c) and clause (d) of sub-section (1) of section 169 of the said Act and who could not reply to the said notice and for whom cancellation order has been passed up to 31st March, 2019, have been given one time opportunity to apply for revocation of cancellation of registration on or before the 22nd July, 2019. Further, vide notification No. 20/2019-Central Tax, dated the 23rd April, 2019, two provisos have been inserted in sub-rule (1) of rule 23 of the Central Goods and Services Tax Rules, 2017 (hereinafter referred to as “the said Rules”). In the light of these changes and in order to ensure uniformity in the implementation of the provisions of the law, the Board, in exercise of its powers conferred by section 168 (1) of the said Act, hereby clarifies the issues relating to the procedure for filing of application for revocation of cancellation of registration.

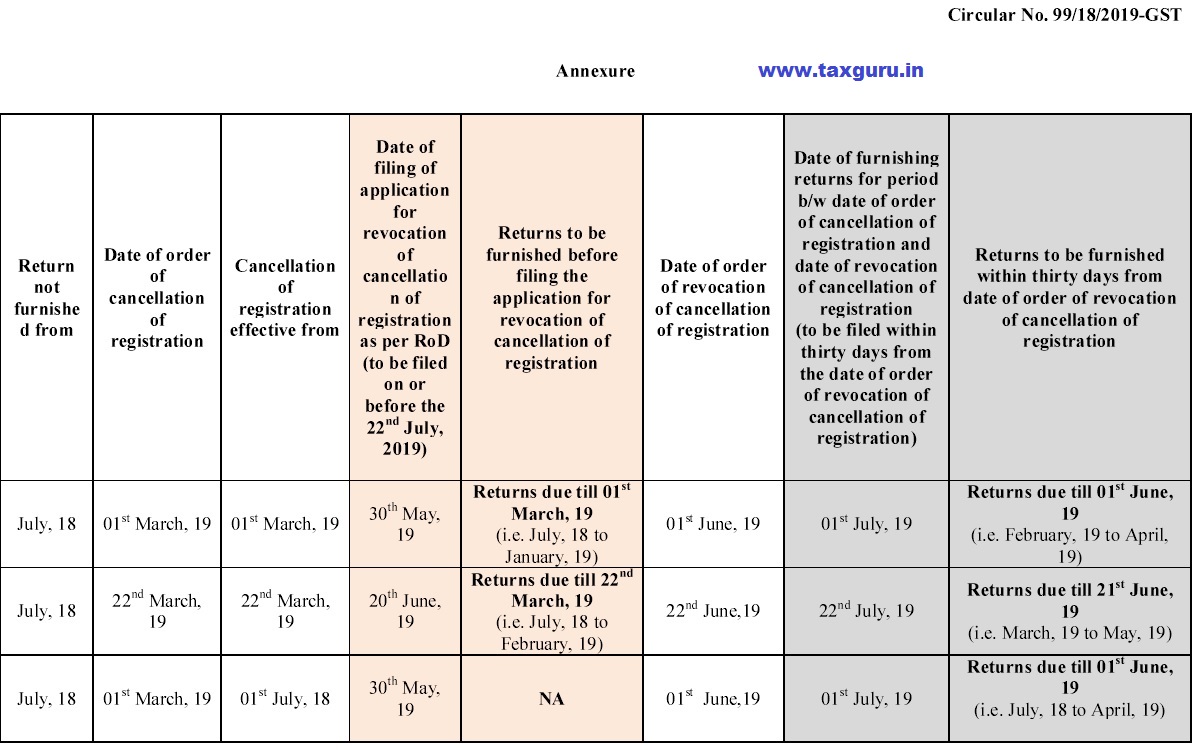

3. First proviso to sub-rule (1) of rule 23 of the said Rules provides that if the registration has been cancelled on account of failure of the registered person to furnish returns, no application for revocation of cancellation of registration shall be filed, unless such returns are furnished and any amount in terms of such returns is paid. Thus, where the registration has been cancelled with effect from the date of order of cancellation of registration, all returns due till the date of such cancellation are required to be furnished before the application for revocation can be filed. Further, in such cases, in terms of the second proviso to sub-rule (1) of rule 23 of the said Rules, all returns required to be furnished in respect of the period from the date of order of cancellation till the date of order of revocation of cancellation of registration have to be furnished within a period of thirty days from the date of the order of revocation.

4. Where the registration has been cancelled with retrospective effect, the common portal does not allow furnishing of returns after the effective date of cancellation. In such cases it was not possible to file the application for revocation of cancellation of registration. Therefore, a third proviso was added to sub-rule (1) of rule 23 of the said Rules enabling filing of application for revocation of cancellation of registration, subject to the condition that all returns relating to the period from the effective date of cancellation of registration till the date of order of revocation of cancellation of registration shall be filed within a period of thirty days from the date of order of such revocation of cancellation of registration. 5 The above provisions are explained, by way of an Illustration in Annexure, for better

5. It is requested that suitable trade notices may be issued to publicize the contents of this circular.

6. Difficulty, if any, in the implementation of this circular may be brought to the notice of the Board immediately. Hindi version follows

(Upender Gupta)

Principal Commissioner (GST)

I have been trying to file applications for revocation through the GST portal but unable to file the same as it is prompting me to file the returns till current date please help me