Statutory provision: Section 43A of Central Goods & Services Tax Act, 2017

♣ The section has been passed by the parliament in by January and has been implemented from 1st February 2019.

♣ The implementation notification is not published yet.

♣ It may be published by September 2019.

Section 43A

(1) Notwithstanding anything contained in sub-section (2) of section 16, section 37 or section 38, every registered person shall in the returns furnished under sub-section (1) of section 39 verify, validate, modify or delete the details of supplies furnished by the suppliers.

Download PPT On New GST Return

Sec 16(2)

(2) Notwithstanding anything contained in this section, no registered person shall be entitled to the credit of any input tax in respect of any supply of goods or services or both to him unless,––

(a) he is in possession of a tax invoice or debit note issued by a supplier registered under this Act, or such other taxpaying documents as may be prescribed;

(b) he has received the goods or services or both. Explanation.—For the purposes of this clause, it shall be deemed that the registered person has received the goods where the goods are delivered by the supplier to a recipient or any other person on the direction of such registered person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to goods or otherwise;

(c) subject to the provisions of section 41 or section 43A, the tax charged in respect of such supply has been actually paid to the Government, either in cash or through utilization of input tax credit admissible in

respect of the said supply; and

(d) he has furnished the return under section 39: Provided that where the goods against an invoice are received in lots or installments, the registered person shall be entitled to take credit upon receipt of the

last lot or installment:

Provided further that where a recipient fails to pay to the supplier of goods or services or both, other than the supplies on which tax is payable on reverse charge basis, the amount towards the value of supply along with tax payable thereon within a period of one hundred and eighty days from the date of issue of invoice by the supplier, an amount equal to the input tax credit availed by the recipient shall be added to his output tax liability, along with interest thereon, in such manner as may be prescribed:

Provided also that the recipient shall be entitled to avail of the credit of input tax on payment made by him of the amount towards the value of supply of goods or services or both along with tax payable thereon.

Can Sec 43A Override 16(2) ???

- (Situation otherwise would be that

- M/s Urvish Patel has made a supply to M/s Shantilal Thakkar and issued a valid invoice to him.

- Now by mistake M/s Urvish Patel has given wrong TIN in his Return of M/s Bhavya Popat,

- He being greedy, or lets say in mistake has accepted the said bill, then….

- the eligibility to claim credit would be of M/s Bhavya Popat and not M/s Shantilal Thakkar

- although Tax Invoice is with him, but the ultimate thing now (After insertion of 43 A)the details as shown in the return u/s 43 A!!!!)

Sec 37 & 38

- Furnishing details of Outward Supplies(Sec 37)

- Furnishing Details of Inward Supplies (Sec 38)

- Return u/s 43A shall be deemed to be return U/s 39.

- The new return system shall have no change in filling return for Composition Registered Person, Input Service distributors, Non Resident Taxable Person and persons liable for TDS and TCS.

43A(2) : Sec 43A Has Been Given an Overriding Effect on Sec 41, 42 and 43.

- Notwithstandin anything contained in section 41, section 42 or section 43, the procedure for availing of input tax credit by the recipient and verification thereof shall be such as may be prescribed.

The Most Dangerous 43A(4)

- The procedure for availing input tax credit in respect of outward supplies not furnished under sub-section (3) shall be such as may be prescribed and such procedure may include the maximum amount of the input tax credit which can be so availed, not exceeding twenty per cent of the input tax credit available, on the basis of details furnished by the suppliers under the said sub-section.

What does 43A(4) mean????

- As the rules of the same are not notified, there can only be assumptions regarding this sub section.

- In my view, the credit shall be allowed for mismatch up to the limit of 20%.

- For Example, A Tax Payer is claiming total credit of Rs 100 in a particular return, and if his credit as per GST ANX-02 is 80 Rupees, he shall be eligible to claim full credit of Rs 100/-.

- But if in the same example, if the credit as per GST ANX-02 is Rs 60/- he shall be eligible to claim credit of Rs. 72 (60+20%) at maximum.

Is law above system or system above law?????

- The rules corresponding to Sec 43A are yet not notified. As a law student we were taught that in a legal hierarchy The

- Constitution is the highest law of the Land.

- Then comes a particular Act, Then rules and then forms and system under a particular law.

- But as a advocate practicing under G.S.T. my understanding has changed 360 degrees.

- Under the GST, GSTN is the highest law.

- Then comes rules and notification, then come the law in some situations.

- Constitution is left far away…..

Large tax payers

- Tax payers whose turnover is more then 5 Crores in the previous year.

- Liable to file Monthly Returns.

- Liable to file Normal Returns only.

- No option of Sahaj and Sugam.

Small tax payers

- Tax Payers with turnover of 5 Crore or below in the previous financial year.

- Has option to file quarterly return

- Option to file GST RET-1/RET-2 (Sahaj)/RET-3(SUGAM)

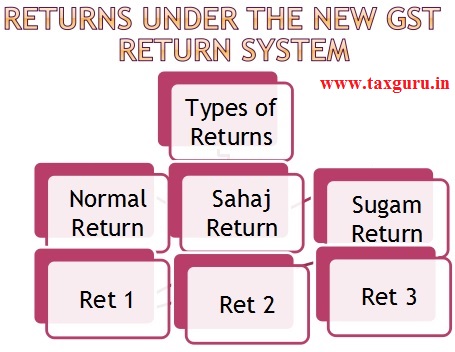

Normal return

- Normal Return is a general return which is available for all

- All the outward supplies transection, i.e. B2B, B2C, Export, SEZ etc covered under this return.

- Monthly or quarterly

- Two Annexure: GST ANX-1 & ANX-2

- Two amendment portion GST ANX-1A and GST RET 1A

Sahaj return

- For Tax Payers involved in B2C transections only.

- Only available to Small Tax Payers

- Quarterly only.

- Two Annexure: GST ANX-1 & ANX-2

- Two amendment portion GST ANX-1A and GST RET 2A

Sugam return

- Only for Small Tax Payers

- Only for tax payers involved in B2C and B2B transactions’.

- Quarterly Only

- Two Annexure: GST ANX-1 & ANX-2

- Two amendment portion GST ANX-1A and GST RET 3A

Instructions for profile updations

- Periodicity deemed to be monthly.

- Quarterly is an option to Small tax payers.

- For new registered dealer, Previous year turnover shall be considered Zero.

- Change in periodicity would be allowed once in a year at the time of filling first return.

- Small tax payers can choose Quarterly Normal, Sahaj and Sugam returns.

Instruction continued….

- Tax payer filling normal return can switch to Sahaj or Sugam only once a financial year, at the beginning of any quarter

- Tax Payer filling Sugam return can switch to Sahaj Only once a financial year at the beginning of any quarter.

- Tax payer filling Sahaj can switch to Sugam or Normal any number of time during the financial year but at the beginning of any quarter.

- Tax Payer filling Sugam can switch to Normal any number of time during F Y at the beginning of QTR

Normal return in detail

- The details can be uploaded on real time basis.

- This details can be uploaded till the due date of return of September 2019 of next financial year or till furnishing of annual return.

- Monthly return fillers will not be able to upload details from 18th to 20th of the month following tax period.

- Quarterly return fillers will not be able to upload details from 23rd to 25th of the month following tax period.

- Recipient shall get credit of documents uploaded by the supplier till 10th of the month following the tax period.

- Supplies attracting reverse charge shall only be declared by the recipient. Now no liability of the supplier to disclose the same.

- HSN mandatory only for Large tax payers. (Most welcome Change)

- Tax amount shall be auto calculated by system, up to 2 decimals.

- However Cess shall have to be inserted manually.

- Place of supply shall be mandatory to be reported.

Details of old system of return

- Document which has been mistakenly left out or are to be amended for returns pertaining to old returns shall be allowed to be amended in new returns.

- If the transaction has not been reported in 3B and also in GSTR 1, the tax is to be paid and is to be reported in ANX 1 and Ret 1/2/3.

- If the transaction is accounted in 3B and failed to be reported in GSTR 1, it is only to be reported in ANX 1 and adjustment has to be done in Colum 3C(5) of Return.

- If the transaction is reported in GSTR 1, but not accounted in 3B, the tax liability shall be adjusted in Colum 3A(8).

Edit and amendment of anx 1

- Edit and amendment to be done in ANX 1A

- Documents can be edited only up to 10th of the following tax period.

- Amendment-Edit only available if the receipient has not accepted by the recipient.

- If the recipient has accpeted the same edit and amendment only possible if the recipient has reset/unlocked the said transaction.

Amendment only to be done by supplier

- Only the supplier can edit or amend the details

- Only recipient can reset/unlock the details.

- Recipient has no option to amend or edit.

Annx 2: Details of inward supplies

- The recipient can view the transaction on real time basis. (If uploaded by the supplier on real time!!!)

- Recipient can taken action on the details showing till 10th of the month following tax period.

- Recipient has 3 main options in Annx 2:

- Accept

- Reject

- Keep pending

- The transactions that can not be corrected through financial credit or debit note has to be rejected.

- Transaction like mistake in bill no, date, HSN etc.

- Keep pending is an action which is neither a acceptance nor a rejection, but is an option to keep the decision of the particular credit pending.

- ITC of pending invoice shall not be available and the said shall be carry forward to next period.

- Pending invoice also not available to supplier for amendment. Though he would have to pay the tax on it.

- Any invoice on which no action has been take shall be deemed to be accepted.

- The status of return filling of supplier shall be made known to the recipient.

- Trade name of the supplier will also be shown along with legal name. (Rare welcome Change)

- The details of supplier returns status shall be mentioned in as M-1 and M-2. The credit of 2 return defaults by the supplier shall be blocked.

- A joke of Mulla Nasruddin….

RET 01: instruction

- Fecility to file NIL return through SMS will be provided.

- After uploading supplies in ANX 1 and taking action on ANX 2, the Ret 1 shall be furnished.

- Information declared in ANX 1 and ANX 2 shall be auto populated.

- Suggested ITC utilization shall be made available automatically, but the tax payer can adjust the same according to system permited under Law.

- The value of tax payable on reverse charge shall be declared in RET 01.

- Adjustments to liability of prior period, excess tax collection may be done in RET 01.

- Due date of RET 1 is 20th of the month following tax period.

ANX 1A: instructions

- Amendment shall be possible for invoice entered during the previous returns.

- Amendment permissible till the September of the next F Y or date of filling annual return whichever is earlier.

- Providing of original details of invoices shall be mandatory.

- Missing document of prior period can not be added in this ANX 1A but has to be reported in ANX 1 itself.

ANX 1A: continued

- The invoice which is accepted by the recipient shall not be eligible for amendment.

- For amendment in such invoice, the recipient needs to reset/unlock such invoice.

ANX RET 01A

- Entries which were not auto populated from ANX 1 & 2 and which were entered manually are to be amended in this form.

- Payment can be made if liability arises due to amendment in RET 01A.

- However if refund arises, no refund shall be paid but the same shall be carried forward to next tax period.

- Full revised value has to be reported in the amendment. If the original amount was shown as 100 but the correct amount is 120, 120 is to be shown.

PMT 08

- Tax payer opting to file return on quarterly basis shall be required to file PMT 08 for the first 2 months.

- In PMT 08 only eligible ITC shall be allowed to be claimed. (ITC available as per ANX 2)

- Payment has to be still done by PMT 05 as challan. This is a set off form.

- Last date of payment through PMT 08 is 20th of the next month.

- Even NIL PMT 08 to be filled.

- Late payment will attract interest u/s 50.

Roadmap to new returns system: Large Tax Payers

- As per the latest press release, dt: 11th June 2019, It has been decided as under:

- Large tax payers, i.e. tax payers with turnover of more then 5 Crore in the previous year, shall file their monthly GST ANX-1 from October 2019

- No GSTR 1 from October 2019.

- For October and November Liable to file GSTR 3B on monthly basis as per current system

- Large tax payers shall be liable to file Ret 01 from December 2019.

Small tax payers

- The small tax payers would stop filling GSTR 3B from the month of October 2019 and start filling GST PMT-08 from October 2019.

- They would start filling RET-01 for the quarter October-December 2019 with due date of 20th January 2020.

- The small tax payers would stop filling GSTR 3B from the month of October 2019 and start filling GST PMT-08 from October 2019.

- From January 2019 Rest in Peace 3B

Author Bio