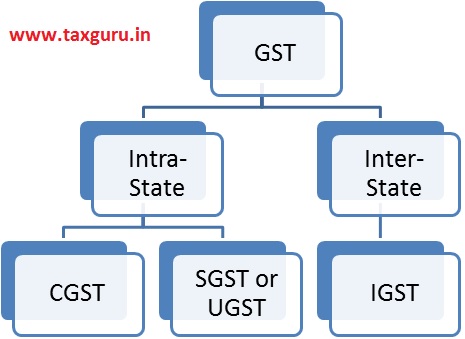

Supply of goods or Services IN GST has to determine whether the supply is

1. Inter-state Supply or

2. Intra-state Supply in GST which is

After the Above segregation one can determine the right taxes on the supply which is as follows:

1. if it is Inter- State Supply —— > Tax – IGST

2. if it is Intra-state Supply in GST which is —— > Tax —CGST and SGST or UGST

Therefore, it becomes pertinent to decide whether supplies shall be treated as intra-State supplies or inter-State supplies. Also, this is necessary to determine because it will be a decisive factor for charging correct taxes, i.e. CGST and SGST/UTGST or IGST.

The relevant provisions for determining inter-State and intra-State supplies are governed by Section 7 and Section 8 of IGST Act.

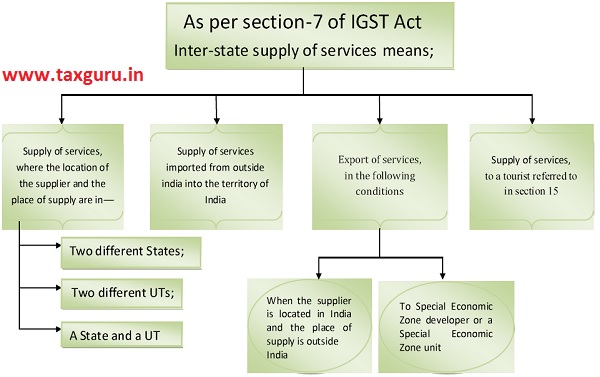

Section of 7 of IGST Act [Inter-State Supply]

1. Inter-State supply where the location of supplier and place of supply are as under and the supply shall be treated as Inter-State;

a] supply in different states

b] supply in different union territory

c] supply in state and union territory

2. supply of goods imported into the territory of India, till it crosses the custom frontier of India.

3. Supply of Goods or service or both ;

-

- Supplier is in India and recipient is outside India.

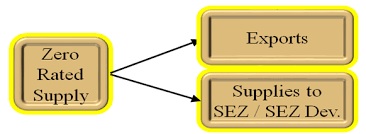

- Supply to or by SEZ unit or Developer.

- Supply in taxable territory, not being an intra-State supply elsewhere in this section.

Section 8 of IGST Act pertains to intra-State supplies.

Sub-section (1) of Section 8 of IGST Act deals with intra-State supply of goods. The said section provides that supply of goods where the location of the supplier and place of supply of goods are in the same State or same Union territory shall be treated as intra-State supply”, the proviso to above section excludes three supplies from being treated as intra-State supply even if the location of supplier and place of supply are in same State or Union territory, these are:

(i) supply to or by an SEZ developer or unit;

(ii) goods or services imported into India and;

(iii) supplies made to tourist referred in Section 15

Sub-section (2) to Section 8 deals with intra-State supply of services and it provides that supply of services where the location of the supplier and the place of supply of services are in the same State or same Union territory shall be treated as intra-state supply”.

A plain reading of the above provisions makes it clear that whereas Section 8(1) is subject to provisions of Section 10, Section 8(2) is subject to provisions of Section 12. In other words, these provisions shall not be applicable in case of export/import of goods which are covered by the provisions of Section 11 of IGST Act, as well as cases where the place of supply of services is determined as per the provisions of Section 13, i.e., in case where either the supplier or the recipient of services is located outside India

Explanation- 1 & 2 in Section -8 is very important to understand the Act in total.

Explanation -1

In the following cases establishments shall be treated as establishments of distinct person.

i. An establishment in India and establishment outside India.

ii. Establishment in State or Union territory and any establishment in other state or union territory .

iii. Establishment in State or Union territory and any establishment being business vertical in same state or union territory .

Explanation -2

A person carrying on business through branch or agency or representation office in any territory shall be treated as establishment in that territory.

4. Supplies in territorial waters

a] where the location of the supplier is in territorial water , location of the supplier or

b] where the place of supply is in territorial water, place of such supply.

Supply shall be deemed to be in the Coastal State or union territory where the nearest point of the appropriate baseline is located

Author Bio